MD: A “Real Money Process” (RMP) does not have reserves. Rather it perpetually maintains perfect supply/demand balance of the money itself (and thus system integrity) via the process. As soon as a DEFAULT is detected, it is immediately mitigated by an INTEREST collection of like amount. The operative relation is INFLATION = DEFAULT – INTEREST = zero. This always makes it interesting to annotate anything that deals with the Federal “Reserve” System. It’s confusion is represented right their in its name.

Reforms may be on the horizon for the Federal Reserve System, as a new bill aims to alter the U.S. central bank’s dual mandate.

MD: An RMP has no mandate, nor does it need one… let alone two.

House Republicans, led by House Committee on Financial Services Chairman French Hill (R-Ark.), introduced the Price Stability Act of 2025, a bill that would end the twin mandate, ensuring the Federal Reserve concentrates primarily on containing inflation.

“For too long, the Federal Reserve has been stretched between competing objectives. It’s time to return to a clear, singular focus: protecting the wallets of American families by keeping inflation in check,” Hill said in a statement.

MD: “For too long”? As in since it was imposed in 1913? The FED has one objective. To collect INTEREST and deliver it to the money changers. Everything else if theater.

In 1977, Congress formally introduced the twin mandate of ensuring maximum employment and price stability through an amendment to the Federal Reserve Act of 1913. The broader legislative initiative emerged as the U.S. economy struggled with higher unemployment, rising inflation, and volatile GDP growth rates.

MD: This I did not know. I thought that was its claim from the very beginning. I have never read the Act. Why bother? When an RMP can be described so concisely and completely you don’t need the details of its competition to know the competition is “no contest”. The RMP has no interest or sensitivity to unemployment or GDP growth rates… neither of which can be measured. It has explicit interest in INFLATION which also can’t be measured… but which the RMP can guarantee to be perpetually zero. Can you imagine brain-dead Congress trying to improve on an RMP? It’s kind of like the justice system trying to improve on the “golden rule”.

Now, a chorus of GOP lawmakers says the institution’s expanding regulatory and supervisory purview over the years is hindering the central bank’s efforts to stabilize prices and threatening the central bank’s independence.

MD: Earth to GOP Lawmakers: “All” of government’s problems with purview of any kind are caused by its perpetual counterfeiting. And BTW, what branch of the Federal Government does the FED fall under. For example, Trump is trying to fire one of the FED governors. Does that mean it’s under the Executive branch?

MD:Their website says: The Board of Governors–an agency of the federal government that reports to and is directly accountable to Congress–provides general guidance for the System and oversees the 12 Reserve Banks.Sounds like Trump has no jurisdiction. Does he appoint anybody in the FED. I guess that a rabbit hole we can leave alone for now.

“Expanding its regulatory reach through unaccountable international agreements or otherwise ill-defined third and fourth mandates, distracts the Fed from doing its congressionally mandated job well,” said Rep. Frank Lucas (R-Ok.), head of the Monetary Policy, Treasury Market Resilience, and Economic Prosperity Task Force.

“The Fed’s actions must stay squarely within congressional intent.”

It is unclear how much broad support there is in the upper chamber for reforming the dual mandate.

Rep. Thomas Massie (R-Ky.) told The Epoch Times that he would support removing all mandates and “just eliminate it … get rid of the Fed.”

MD: And what does Massie propose for the creation and destruction of money. I wonder if we could get him to look at the RMP in this regard. Getting rid of the Fed is a good idea but we sure don’t want some department that is as stupid as the Treasury Department to take up that responsibility.

“The fact that they’re trying to do something to it means that it is broken,” he said.

The legislative proposal from GOP lawmakers comes soon after the Fed completed its review of its monetary policy framework, which, in part, examined the dual mandate.

MD: If you think there is such a thing as a monetary policy framework, let alone a monetary policy, you have some studying to do.

Fed officials agreed to return to flexible inflation targeting in the policymaking blueprint and abandoned the “makeup strategy,” a key component of the 2020 framework.

MD: If your inflation target is anything but zero you’re on the wrong track. And zero is not a target… it’s a guaranteed result of an RMP.

“The document continues to explain how we interpret the mandate Congress has given us and describes the policy framework that we believe will best promote maximum employment and price stability,” Fed Chair Jerome Powell said last month in his speech at the central bank’s annual Jackson Hole retreat.

MD: Again. And RMP doesn’t care anything about policy. It cares only about one simple thing. That being perpetually guaranteeing the relation: INFLATION = DEFAULT – INTEREST = zero.

“We continue to believe that monetary policy must be forward looking and consider the lags in its effects on the economy.”

MD: There is no way to know how many lags there are; what those lags are; how they are phased; and what they have to do with the economy. And an RMP doesn’t care. With the RMP guaranteeing Free Supply of Money and perpetual zero INFLATION and zero INTEREST load on responsible traders, everything else will take care of itself.

Talking Reforms to the Federal Reserve

In recent months, several senior administration officials and economic observers have recommended a full review of Fed operations.

Earlier this month, Treasury Secretary Scott Bessent penned an essay titled “The Fed’s New ‘Gain-of-Function’ Monetary Policy.”

The piece was a sharp critique of how the Federal Reserve has evolved since the 2008 global financial crisis. Bessent, who has been a frequent critic of the century-old entity over the past year, stated that the Fed has engineered new powers, pointing to, for example, quantitative easing—an unconventional monetary policy tool that consists of creating ultra-low interest rates, buying government bonds, and injecting liquidity into the U.S. financial system.

MD: All this manipulation is at best theater… at worst corruption. And it is likely the “worst”. It creates the so-called business cycle which is the money-changers farming operation.

According to Bessent, the Fed has distorted financial markets, diminished independence, and manufactured adverse consequences for the economy.

“Overuse of nonstandard policies, mission creep, and institutional bloat are threatening the central bank’s monetary independence,” Bessent wrote.

MD: Bessent as head of the Treasury is proof positive the Treasury doesn’t know what it is doing. Nor does Trump who put her there. And how can you have a “non-standard policy” when you have no standard nor any way of complying with one. The bank’s don’t need monetary independence. The RMP dictates their actions… should they exist at all, and I don’t see why they should.

He proposed a full-scale “honest, independent, and nonpartisan review” of the entire Federal Reserve System, such as monetary and regulatory policymaking, communications, staffing, and research.

Treasury Secretary Scott Bessent testifies before the House Ways and Means Committee on Capitol Hill in Washington on June 11, 2025. Madalina Vasiliu/The Epoch Times

Others have also called for reviewing and reforming the U.S. central bank.

Most notably, former Fed Governor Kevin Warsh, who is one of the three finalists on the short list to replace Fed Chair Jerome Powell next year, suggested a “regime change” at the institution.

“The credibility deficit lies with the incumbents that are at the Fed, in my view,” Warsh said in a July 17 interview with CNBC’s “Squawk Box.”

MD: The “credibility deficit” lies in trying to use anything but an RMP. It’s as good a system as can ever exist for provisioning money.

He also suggested an alliance between the Federal Reserve and the Treasury Department, similar to the one that occurred in March 1951. Both institutions agreed to liberate the Fed from the Treasury’s control, allowing it to conduct monetary policy independently of executive intervention.

MD: Liberate the Fed from Treasury’s control? So that means it was under the Executive Branch? Need to look into what happened in March of 1951.

The Fed had been pressured during World War II to keep interest rates artificially low to help fund war efforts with cheap debt. A burst of inflation occurred after the war’s end, but it was not until after the accord that the Fed started tightening monetary policy.

MD: And here is where an RMP really shines. When the “elites” want to turn on their war factories, they have to find different funding than government counterfeiting. This should eliminate wars altogrther. Put the “elites” in a ring together and let them settle their differences by dukeing it out.

Warsh said a new arrangement should enable the Fed and the Treasury to communicate their objectives to the financial markets.

“We need a new Treasury-Fed accord, like we did in 1951, after another period where we built up our nation’s debt, and we were stuck with a central bank that was working at cross purposes with the Treasury. That’s the state of things now,” he said.

“So if we have a new accord, then the Fed chair and the Treasury secretary can describe to markets plainly and with deliberation, ‘This is our objective for the size of the Fed’s balance sheet.’”

MD: The blind leading the blind?

A March 2024 paper by the Manhattan Institute, co-authored by Fed Governor Stephen Miran, suggested a series of reforms to strengthen independence and recalibrate “the Fed’s governance to ensure that it remains insulated from day-to-day politics.”

The paper proposed reforming term limits, closing the revolving door between the executive branch and the Fed, addressing the FOMC voting structure, and bolstering the “influence and independence” of regional central banks.

“Only by providing for both accountability and a reliable measure of independence can the Fed restore its reputation in the eyes of the public,” the report stated.

A recent Economist–YouGov poll found that only 45 percent of Americans trust the Federal Reserve to handle the U.S. economy, with thirty-three percent approving of the job Powell is doing as head of the central bank.

At the Sept. 17 post-meeting press conference, when asked if he would support an independent review, Powell signaled he was open to the idea.

“We’re certainly open to always trying to do better,” Powell said.

MD: Try an RMP… and take the rest of your life off.

The Fed followed through on its first rate cut of the year at the September Federal Open Market Committee policy meeting. Officials voted 11–1 to reduce the benchmark federal funds rate by a quarter point to a target range of 4.00 percent to 4.25 percent.

The rate-setting FOMC will convene its next two-day policy meeting on Oct. 28 and 29.20,142191

MD:Money Delusions knows a “Real Money Process” (RMP) has no need for a central bank.

The Federal Reserve is the central bank of the United States and is arguably the most influential economic institution in the world. One of the chief responsibilities set out in the Fed’s charter is the management of the total outstanding supply of U.S. dollars and dollar substitutes. The Fed is responsible for creating or destroying several billion dollars every single day.

MD: Should an institution be “influential”. Is that the reason for having institutions? How can the Fed manage the supply of U.S. dollars… and why the qualifier “outstanding”? If it’s money, it’s outstanding. Money that has served its purpose (i.e. monitoring a trading promise spanning time and space) is destroyed as it completes that function. If the Fed was really the RMP, it would be responsible for “monitoring transparently” the performance on money creating promises. How does the Fed “create” money? How does it “destroy” money? How can it possibly know the “outstanding supply” of money? It can’t… and it doesn’t. The Fed is a rigged game posing as regulation and control. It’s the money-changers “farming” operation… and Thomas Jefferson, himself being a planter, warned against exactly that.

Despite being colloquially charged with running the printing press for dollar bills, the modern Federal Reserve no longer simply runs new paper bills off of a machine. Some real dollar printing does still occur (with the help of the U.S. Department of the Treasury), but the vast majority of the American money supply is digitally debited and credited to major banks. The real money creation takes place after the banks loan out those new balances to the broader economy.

MD: The Fed never did run “bills off of a machine”. The Treasury has always done that at their “mints”. They have 4 (Philadelphia, San Francisco, West Point, and New Orleans). It has 2 printing presses: Ft. Worth and Washington, DC. This may be the only thing Washington DC actually produces… yet it makes up part of 3 of the wealthiest counties in the country… and part one of the poorest. Why so much wealth? Why so much poverty?

At least the article gets one thing right. A RMP does addition and subtraction. But it doesn’t create money… and its member banks do not create money. You can’t point to a single instance where money is created that there is not a trader “requesting (demanding)” that it be created. And it obviously isn’t loaned by banks because banks don’t have it to loan. They exist by creating 10x as much money as they have capitalizing the bank. And they collect a % which they call INTEREST. If it was their own money, that 2% to 4% would seem small. Groceries, the most efficient businesses out there, only earn 3% on their sales. But with banks 10x leverage, that becomes 20% to 40%. At 20%, money doubles every 3-1/2 years. At 40% it doubles in less than 2 years.

In a RMP, INTEREST just mitigates DEFAULTs experienced. No DEFAULTs… no INTEREST. The operative relation is INFLATION = DEFAULTS – INTEREST = zero.

Determining the Money Supply

The Federal Open Market Committee (FOMC) and associated economic advisers meet regularly to assess the U.S. money supply and general economic condition. If it is determined that new money needs to be created, then the Fed targets a certain level of money injection and institutes a corresponding policy.

MD: This doesn’t sound like a “real time” operation. And an RMP cares nothing about “economic condition”. An RMP knows exactly how much money is needed. It’s the amount of in-process trading promises created by traders. An RMP has no policy… unless that’s what you call mitigating DEFAULTs experienced with immediate INTEREST collections of like amount. I call that an automatic control system delivering an automatic negative feedback loop to the process.

It’s hard to track the actual amount of money in the economy because many things can be defined as money. Obviously paper bills and metal coins are money, and savings accounts and checking accounts represent direct and liquid money balances. Money market funds, short-term notes and other reserves are also often counted. Nevertheless, the Fed can only approximate the money supply.

MD: It’s not hard to track the actual amount of money. It’s the amount created by traders promises that have not yet been delivered as promised. It’s addition and subtraction and there is no hocus pocus involved. And not only can the RMP know precisely the supply and demand for money, it maintains that perfect perpetual balance in real time. That’s how it “guarantees” zero INFLATION… all the time… everywhere.

The Fed could initiate open market operations, where it buys and sells Treasurys to inject or absorb money. It can use repurchase agreements for temporary expansions. It can use the discount window for short-term loans to banks. By far, the most common result is an increase in bank reserves.

MD: The Fed has no income with which to buy anything. To the extent it is capitalized by its member banks, that’s a reserve to combat a “run on the banks”. That cannot happen with an RMP. There are no reserves in an RMP. The RMP loans nothing. Thus, there is nothing “to run on”. To the extent that the process leaks (i.e. experiences DEFAULTs), it replaces those leaks immediately with INTEREST collections of like amount. It’s precise… and it’s real time.

We will now leave the remainder of the annotations as an exercise for the student. The principles are that simple. Have at it. And if you get stuck, revisit the real definition of money and the description of the Real Money Process (RMP).

Money Creation Mechanism

In the early days of central banking, money creation was a physical reality; new paper notes and new metallic coins would be crafted, imprinted with anti-fraud devices and subsequently released to the public (almost always through some favored government agency or politically connected business).

Central banks have since become much more technologically creative. The Fed figured out that money doesn’t have to be physically present to work in an exchange. Businesses and consumers could use checks, debit and credit cards, balance transfers and online transactions. Money creation doesn’t have to be physical, either; the central bank can simply imagine up new dollar balances and credit them to other accounts.

A modern Federal Reserve drafts new readily liquefiable accounts, such as U.S. Treasurys, and adds them to existing bank reserves. Normally, banks sell other monetary and financial assets to receive these funds.

This has the same effects as printing up new bills and transporting them to the bank vaults, only it’s cheaper. It is just as inflationary, and the newly credited money balances count just as much as physical bills in the economy.

The Credit Market Funnel

Suppose the U.S. Treasury prints up $10 billion in new bills, and the Federal Reserve credits an additional $90 billion in readily liquefiable accounts. At first, it might seem like the economy just received a monetary influx of $100 billion, but that is actually only a very small percentage of the actual money creation.

This is because of the role of banks and other lending institutions that receive new money. Nearly all of that extra $100 billion enters banking reserves. Banks don’t just sit on all of that money, even though the Fed now pays them 0.25% interest to just park the money with the Fed Bank. Most of it is loaned out to governments, businesses and private individuals.

The credit markets have become a funnel for money distribution. However, in a fractional reserve banking system, new loans actually create even more new money. With a legally required reserve ratio of 10%, the new $100 billion in bank reserves could potentially result in a nominal monetary increase of $1 trillion.

By Andrew Beattie | Updated December 29, 2015 — 1:56 PM EST

Money, in and of itself, is nothing. It can be a shell, a metal coin, or a piece of paper with a historic image on it, but the value that people place on it has nothing to do with the physical value of the money. Money derives its value by being a medium of exchange, a unit of measurement and a storehouse for wealth. Money allows people to trade goods and services indirectly, understand the price of goods (prices written in dollar and cents correspond with an amount in your wallet) and gives us a way to save for larger purchases in the future.

Money is valuable merely because everyone knows everyone else will accept it as a form of payment – so let’s take a look at where it has been, how it evolved and how it is used today. (To learn more about money itself, see What Is Money?)

A World Without Money

Money, in some form, has been part of human history for at least the last 3,000 years. Before that time, it is assumed that a system of bartering was likely used.

Bartering is a direct trade of goods and services – I’ll give you a stone axe if you help me kill a mammoth – but such arrangements take time. You have to find someone who thinks an axe is a fair trade for having to face the 12-foot tusks on a beast that doesn’t take kindly to being hunted. If that didn’t work, you would have to alter the deal until someone agreed to the terms. One of the great achievements of money was increasing the speed at which business, whether mammoth slaying or monument building, could be done.

Slowly, a type of prehistoric currency involving easily traded goods like animal skins, salt and weapons developed over the centuries. These traded goods served as the medium of exchange even though the unit values were still negotiable. This system of barter and trade spread across the world, and it still survives today on some parts of the globe.

Asian Cutlery

Sometime around 1,100 B.C., the Chinese moved from using actual tools and weapons as a medium of exchange to using miniature replicas of the same tools cast in bronze. Nobody wants to reach into their pocket and impale their hand on a sharp arrow so, over time, these tiny daggers, spades and hoes were abandoned for the less prickly shape of a circle, which became some of the first coins. Although China was the first country to use recognizable coins, the first minted coins were created not too far away in Lydia (now western Turkey).

Coins and Currency

In 600 B.C., Lydia’s King Alyattes minted the first official currency. The coins were made from electrum, a mixture of silver and gold that occurs naturally, and stamped with pictures that acted as denominations. In the streets of Sardis, circa 600 B.C., a clay jar might cost you two owls and a snake. Lydia’s currency helped the country increase both its internal and external trade, making it one of the richest empires in Asia Minor. It is interesting that when someone says, “as rich as Croesus”, they are referring to the last Lydian king who minted the first gold coin. Unfortunately, minting the first coins and developing a strong trading economy couldn’t protect Lydia from the swords of the Persian army. (To read more about gold, see What Is Wrong With Gold?)

Not Just a Piece of Paper

Just when it looked like Lydia was taking the lead in currency developments, in 600 B.C., the Chinese moved from coins to paper money. By the time Marco Polo visited in 1,200 A.D., the emperor had a good handle on both money supply and various denominations. In the place of where the American bills say, “In God We Trust,” the Chinese inscription warned, “All counterfeiters will be decapitated.”

Europeans were still using coins all the way up to 1,600, helped along by acquisitions of precious metals from colonies to keep minting more and more cash. Eventually, the banks started using bank notes for depositors and borrowers to carry around instead of coins. These notes could be taken to the bank at any time and exchanged for their face values in silver or gold coins. This paper money could be used to buy goods and operated much like currency today, but it was issued by banks and private institutions, not the government, which is now responsible for issuing currency in most countries.

The first paper currency issued by European governments was actually issued by colonial governments in North America. Because shipments between Europe and the colonies took so long, the colonists often ran out of cash as operations expanded. Instead of going back to a barter system, the colonial governments used IOUs that traded as a currency. The first instance was in Canada, then a French colony. In 1685, soldiers were issued playing cards denominated and signed by the governor to use as cash instead of coins from France.

Money Travels

The shift to paper money in Europe increased the amount of international trade that could occur. Banks and the ruling classes started buying currencies from other nations and created the first currency market. The stability of a particular monarchy or government affected the value of the country’s currency and the ability for that country to trade on an increasingly international market. The competition between countries often led to currency wars, where competing countries would try to affect the value of the competitor’s currency by driving it up and making the enemy’s goods too expensive, by driving it down and reducing the enemy’s buying power (and ability to pay for a war), or by eliminating the currency completely.

Mobile Payments

The 21st century gave rise to two disruptive forms of currency: Mobile payments and virtual currency. A mobile payment is money rendered for a product or service through a portable electronic device such as a cell phone, smartphone or PDA. Mobile payment technology can also be used to send money to friends or family members. Increasingly, services like Apple Pay and Samsung Pay are vying for retailers to accept their platforms for point-of-sale payments.

Virtual Currency

Bitcoin, invented in 2009 by the pseudonymous Satoshi Nakamoto, became the gold standard–so to speak–for virtual currencies. Virtual currencies have no physical coinage. The appeal of virtual currency is it offers the promise of lower transaction fees than traditional online payment mechanisms and is operated by a decentralized authority, unlike government issued currencies.

The Bottom Line

Despite many advances, money still has a very real and permanent effect on how we do business today. (Follow the development of money in the United States in The History Of Money: Currency Wars.)

The central bank has been described as “the lender of last resort,” which means it is responsible for providing its economy with funds when commercial banks cannot cover a supply shortage. In other words, the central bank prevents the country’s banking system from failing. However, the primary goal of central banks is to provide their countries’ currencies with price stability by controlling inflation. A central bank also acts as the regulatory authority of a country’s monetary policy and is the sole provider and printer of notes and coins in circulation. Time has proved that the central bank can best function in these capacities by remaining independent from government fiscal policy and therefore uninfluenced by the political concerns of any regime. The central bank should also be completely divested of any commercial banking interests.

The Rise of the Central Bank

Today the central bank is government owned but separate from the country’s ministry of finance. Although the central bank is frequently termed the “government’s bank” because it handles the buying and selling of government bonds and other instruments, political decisions should not influence central bank operations. Of course, the nature of the relationship between the central bank and the ruling regime varies from country to country and continues to evolve with time. To ensure the stability of a country’s currency, the central bank should be the regulator and authority in the banking and monetary systems.

Historically, the role of the central bank has been growing, some may argue, since the establishment of the Bank of England in 1694. It is, however, generally agreed upon that the concept of the modern central bank did not appear until the 20th century as problems developed in the commercial banking system. Thus, the central bank’s modern function emerged in response to an already present commercial banking structure.

Between 1870 and 1914, when world currencies were pegged to the gold standard (GS), maintaining price stability was a lot easier because the amount of gold available was limited. Consequently, monetary expansion could not occur simply from a political decision to print more money, so inflation was easier to control. The central bank at that time was primarily responsible for maintaining the convertibility of gold into currency; it issued notes based on a country’s reserves of gold. (For more insight, read The Gold Standard Revisited.)

At the outbreak of WWI, the GS was abandoned, and it came apparent that, in times of crisis, governments, facing budget deficits (because it costs money to wage war) and needing greater resources, will order the printing of more money. As governments did so, they encountered inflation. After WWI, many governments opted to go back to the GS to try to stabilize their economies. With this rose the awareness of the importance of the central bank’s independence from the political machine.

During the unsettling times of the Great Depression and the aftermath of WWII, world governments predominantly favored a return to a central bank dependent on the political decision-making process. This view emerged mostly from the need to establish control over war-shattered economies; furthermore, countries with newly-acquired independence opted to keep control over all aspects of their countries – a backlash against colonialism. The rise of managed economies in the Eastern Bloc was also responsible for increased government interference in the macro economy. Soon after the effects of WWII, however, the independence of the central bank from the government came back into fashion in Western economies and has prevailed as the optimal way to achieve a liberal and stable economic regime.

How the Bank Influences an Economy

A central bank can be said to have two main kinds of functions: (1) macroeconomic when regulating inflation and price stability and (2) microeconomic when functioning as a lender of last resort. (For background reading on macroeconomics, see Macroeconomic Analysis.)

Macroeconomic Influences

As it is responsible for price stability, the central bank must regulate the level of inflation by controlling money supplies by means of monetary policy. The central bank performs open market transactions that either inject the market with liquidity or absorb extra funds, directly affecting the level of inflation. To increase the amount of money in circulation and decrease the interest rate (cost) for borrowing, the central bank can buy government bonds, bills, or other government-issued notes. This buying can, however, also lead to higher inflation. When it needs to absorb money to reduce inflation, the central bank will sell government bonds on the open market, which increases the interest rate and discourages borrowing. Open market operations are the key means by which a central bank controls inflation, money supply, and price stability. If you’d like to learn more about this subject, read The Federal Reserve (the Fed) Tutorial.

Microeconomic Influences

The establishment of central banks as lender of last resort has pushed the need for their freedom from commercial banking. A commercial bank offers funds to clients on a first come, first serve basis. If the commercial bank does not have enough liquidity to meet its clients’ demands (commercial banks typically do not hold reserves equal to the needs of the entire market), the commercial bank can turn to the central bank to borrow additional funds. This provides the system with stability in an objective way; central banks cannot favor any particular commercial bank. As such, many central banks will hold commercial-bank reserves that are based on a ratio of each commercial bank’s deposits. Thus, a central bank may require all commercial banks to keep, for example, a 1:10 reserve/deposit ratio. Enforcing a policy of commercial bank reserves functions as another means to control the money supply in the market. Not all central banks, however, require commercial banks to deposit reserves. The United Kingdom, for example, does not have this policy while the United States does.

The rate at which commercial banks and other lending facilities can borrow short-term funds from the central bank is called the discount rate (which is set by the central bank and provides a base rate for interest rates). It has been argued that, for open market transactions to become more efficient, the discount rate should keep the banks from perpetual borrowing, which would disrupt the market’s money supply and the central bank’s monetary policy. By borrowing too much, the commercial bank will be circulating more money in the system. Use of the discount rate can be restricted by making it unattractive when used repeatedly. (To learn more, read Understanding Microeconomics.)

Transitional Economies

Today developing economies are faced with issues such as the transition from managed to free market economies. The main concern is often controlling inflation. This can lead to the creation of an independent central bank but can take some time, given that many developing nations maintain control over their economies in an effort to retain control of their power. But government intervention, whether direct or indirect through fiscal policy, can stunt central bank development. Unfortunately, many developing nations are faced with civil disorder or war, which can force a government to divert funds away from the development of the economy as a whole. Nonetheless, one factor that seems to be confirmed is that, for a market economy to develop, a stable currency (whether achieved through a fixed or floating exchange rate) is needed. However, the central banks in both industrial and emerging economies are dynamic because there is no guaranteed way to run an economy regardless of its stage of development.

The Bottom Line

Central banks are responsible for overseeing the monetary system for a nation (or group of nations), along with a wide range of other responsibilities, from overseeing monetary policy to implementing specific goals such as currency stability, low inflation, and full employment. The role of the central bank has grown in importance over time, but in U.S., its activities continue to evolve.

On page 81 of Democracy in Chains Nancy MacLean describes John C. Calhoun’s “case for minority veto power” – that is, Calhoun’s proposal that no legislation be enacted unless it receives the approval of “the concurrent majority” – as being “like that which Buchanan and Tullock were advocating” in The Calculus of Consent. She’s mistaken. Significant differences distinguish Buchanan’s and Tullock’s proposal from Calhoun’s proposal of a concurrent majority.

The most important of these distinctions is the one mentioned in my correction of Michael Chwe’s misunderstanding of Buchanan’s proposed unanimity rule – namely, for Buchanan and Tullock, the only rules which require unanimous consent are constitutional rules, including the rules that determine the procedures and requirements for enacting legislation. Buchanan and Tullock argued that, when choosing constitutional rules, individuals would recognize that a rule of unanimity for the enactment of ordinary legislation would be too costly. At the constitutional stage of decision-making, therefore, individuals unanimously agree to have some rule of less-than-unanimity – for example, majority rule – for the enactment of legislation. More precisely, Buchanan and Tullock argued that, at the constitutional stage, individuals might choose different rules for the enactment of different kinds of legislation. For example, individuals might choose to allow tax rates to be changed with the approval of a simple majority, while proposals to declare war must receive the approval of two-thirds of the citizens’ representatives. The relevant point here is that the rule of unanimity for Buchanan and Tullock – unlike for Calhoun – applies only to the making of constitutional rules and not to the enactment of legislation.

Another important difference between Buchanan’s and Tullock’s proposal and Calhoun’s is that, for Buchanan and Tullock, the unanimous approval that is required is that of individuals; for Calhoun, the unanimous approval that is required is that of groups. Calhoun thought of society as being naturally comprised of different “interests” – for example., planters, merchants, and lawyers. As explained by Alex Tabarrok and Tyler Cowen in their 1992 paper on the extent to which Calhoun anticipated public choice,

Calhoun’s thought on the question of optimal consent is clearly related to pluralist or corporatist “group theory.” In particular, Calhoun’s concurrent majority applies to interest groups and not individuals [p. 666]…. Unlike Buchanan, Calhoun does not subscribe to normative individualism of contractarianism. The social state is thought of as God-given and methodologically prior to civilized man [p. 671].

Each proposed piece of legislation must, under Calhoun’s system, win majority approval from each of the different interests – thus the term concurrent majority.

Unlike Calhoun, no public-choice scholar accepts the idea that among the elemental components of society are different “interests.” Instead, for public-choice scholars, the elemental components of society are individuals. It’s true that public-choice analysis predicts that individuals will often form themselves into interest groups, but such groups are the product of the interplay of the costs and the expected benefits to individuals of so organizing. Unlike for Calhoun’s “interests,” the interest groups identified by public choice are not elemental entities each of which deserves, by right, a say in – and much less a veto power over – the enactment of legislation. (Indeed, the normative attitude of public-choice scholars toward interest groups is decidedly negative, for such groups typically succeed in using state power to secure benefits for themselves at a greater cost to society at large.)

In short, for Calhoun, interest groups are simply assumed to exist, and to exist in such numbers that the interests of all individuals in the polity are thereby represented by this collection of groups. In stark contrast, for public choice, interest groups arise if and only to the extent that the costs to individuals of forming into a group are exceeded by the benefits that each individual expects to receive by joining the group. For Calhoun, the interplay of interests under a system of concurrent-majority rule ensures good government. For public-choice scholars, the political activity of interest groups is among the most important forces that incite government to behave badly.

….

In summary, for Buchanan (and for Buchanan and Tullock) the rule of unanimity was to govern only the enactment of constitutional rules and not the enactment of legislation. This fact alone renders false MacLean’s assertion that Buchanan’s and Tullock’s proposal is “like” that of Calhoun’s. When other aspects of Buchanan’s and Tullock’s analysis are considered – such as their belief that each individual should have an equal say in the choosing of constitutional rules – the similarity between Buchanan’s analysis and that of Calhoun shrinks even further. Here, again, are Tabarrok and Cowen:

Buchanan has chosen individual preferences as the source of justification for his proposed unanimity rule. For Buchanan, informed consent is the ultimate source of value. The purpose of a political constitution is to allow men to achieve their desired ends. There are no values higher than those given by preferences, and the state is visualized as a hypothetical social compact among autonomous, contracting individuals [p. 672].

None of the above denies that Calhoun (like several other thinkers) anticipated some aspects of public choice. But the normative, methodological, and practical differences between Calhoun, on one hand, and Buchanan, Tullock, and other public-choice scholars, on the other, is so huge that for MacLean to describe Buchanan’s and Tullock’s project as being “like” that of Calhoun’s – and for her to conclude that Calhoun is the “intellectual lodestar” of public-choice scholars – is absurd. If MacLean sincerely believes her charge, then she either has not read carefully Calhoun or public choice (or both), or she is unable to grasp not just the (many) subtleties in these works but also their main thrusts. (Indeed, MacLean admits to having read the Tabarrok-Cowen article quoted above; but, obviously, she did not read it carefully enough to grasp its full message.) Either way, MacLean had no business writing a book about these matters.

Here’s a letter that I sent several days ago to the Washington Post:

In “The beliefs of economist James Buchanan conflict with basic democratic norms. Here’s why” (July 25) Michael Chwe is completely mistaken when he writes that Buchanan wanted to “make the passing of new laws as difficult as possible, requiring unanimous consent.” Buchanan argued for unanimous consent only to constitutional rules; he emphatically did not argue for unanimous consent to legislation enacted under any existing constitution. Indeed, the very point of the most famous chapter (#6) of his most famous book, The Calculus of Consent (co-authored with Gordon Tullock), is to explain why unanimous consent to ordinary legislation is an unworkable and, hence, unacceptable idea.

Central to Jim Buchanan’s life’s work was the distinction between choosing constitutional rules and choosing legislation and regulation within constitutional rules. It’s unfortunate that Prof. Chwe misses this key distinction and, in the process, portrays Buchanan in an exceedingly misleading light.

Sincerely,

Donald J. Boudreaux

Professor of Economics

and

Martha and Nelson Getchell Chair for the Study of Free Market Capitalism at the Mercatus Center

George Mason University

Fairfax, VA 22030

… is from this speech, which I believe was delivered sometime in the late 1970s or early 1980s, by the late, great Milton Friedman (who was born 105 years ago today):

You must separate out being pro free-enterprise from being pro-business. The two greatest enemies of the free enterprise system, in my opinion, have been on the one hand my fellow intellectuals, and on the other hand, the big businessmen – for opposite reasons.

Ethereum Co-Founder Responds To Sweden’s Cashless-Society Rethink

MD: We never know what we’re going to get into with these “cyber money” articles. Looks like someone’s having reservations about how well it works. And is it correct to refer to it as “cashless”?

If I have a $100 bill and I take it to a gas station and trade it for a tank of gas and $50 in change that’s a “cash” transaction. The gas station now has a $100 bill in their cash register. And they have one less $50 bill there. Further, they have $50 less gas in their buried tank. And I have $50 worth of gas in my truck. And I have a $50 bill in my wallet where I once had a $100 bill.

Now, does anything change if I give the gas station a debit card… or a credit card… or the gas station’s own branded credit card? It’s all just accounting. It’s all just moving “cash” around. Or is it? There’s an important distinction between a “debit” card and a “credit” card.

With a “debit” card, you have something keeping track of “cash you have”. With a “credit” card you have something keeping track of “cash you create”… cash you “don’t” have… cash you must return to complete your promise. Cash you have is an “in process promise to complete a trade spanning time and space” You don’t know who made that promise. You do know it wasn’t you. You are using it as the most common object in simple barter exchange.

But what about the “credit” card. It’s about “cash you create”. And when you “create” cash, “you” are making the “promise to complete a trade spanning time and space.” And it is “you” who must deliver on that promise. But it’s still cash. It’s still money. But it’s not money “you” have. It’s money the creator of the credit card has. These are terms referring to the same thing. At the end of the month you “pay” off your credit card… usually by making a deposit in an account. And what do you deposit in the account? Probably a check from your employer.

And that check from your employer… what is that? It’s a token that will eventually take cash out of his account and transfers it into your account. That is now a principal function of a bank. It’s a banking function that they charge you for.

In the beginning, it was no function of a bank at all. The function of a bank was to keep people from stealing your valuables… whether in a safe deposit box, or in their vault holding gold and silver… things people “believe” to have value. And you paid the bank for that safe keeping. And in the end, the bank occasionally lost your gold and silver… and said “sorry… it’s gone!”

So, are we clear what “cash” is? Are we clear that the term “cashless” is meaningless?

As Sweden reconsiders its push toward a cashless society, Ethereum co-founder Vitalik Buterin highlighted the fragility of centralized digital payments and the opportunity presented by decentralized payment alternatives.

MD: “Fragility of centralized digital payments”. I think this is the “thesis statement” of this article. Let’s keep it in mind as we proceed.

In recent years, Sweden has led the charge toward a cashless future, with digital payment platforms becoming widespread. However, as concerns over cyber-threats, civil defense and instability have emerged, Swedish authorities are now actively encouraging citizens to keep some cash.

MD: What he’s really saying is “keep your cash as stuff rather than as numbers in a ledger”. And is a token representing numbers in a ledger stuff? Well, we’re seeing how confused these geniuses are, aren’t we.

Buterin noted the reversal illustrates that while centralized solutions may be efficient, they may not be reliable during times of crisis.

MD: If tokens (i.e. stuff) representing numbers in a ledger is not a “centralized solution”, then what is it? Would it be better to call it a “universal” solution? I think so.

“Nordics are walking back the cashless society initiative because their centralized implementation of the concept is too fragile,” Buterin wrote, citing a March 16 article by The Guardian. “Cash turns out necessary as a backup.”

MD: Ethereum claims to be money. It falsely assumes that by keeping track of “pure waste” of electricity, money is created. And Ethereum is the ledger that keeps track of that. It’s obviously silly… but that’s the concept. They call it “proof of work”. And now they’re suggesting that that number in the ledger is actually worthless… even though it stands for actual waste. And as a backup, you should keep some “cash”. Now tell me, where did the cash come from?

A former central bank official predicted in 2018 that Sweden would be cashless after seven years. In 2025, the prediction mostly held, with only one in 10 transactions in the country being done in cash, according to The Guardian.

MD: This “one in 10” is probably a made up statistic. Do you really think it’s somebody’s job to keep track of so-called “cash” transactions as distinct from “non-cash” transactions?

Still, while the Nordic country was an early adopter of digital payments, its government published a brochure encouraging citizens to keep a week’s worth of cash in case of war or crisis. Sweden’s reconsideration has revealed the issue of centralized digital payment infrastructure remaining reliable in times of instability, Buterin suggested.

MD: “… in case of war or crisis…” This suggests that this ethereum stuff disappears or is otherwise inaccessible in some situations. And this isn’t true of what they’re calling cash… which is presumably “currency” and “coin”… tokens that don’t disappear for some reason. That suggests, if we are to have a truly cashless society, we need an indelible record. Could an SD card be made to act like an indelible record? It could if it could be encrypted with a password that only the owner knows. An invention is needed here.

Buterin said Ethereum can be a decentralized financial fallback in times of crisis. “Ethereum needs to be resilient enough, and private enough, to be able to credibly play this kind of role,” Buterin said.

MD: Seems to me what we need is a process that moves numbers from one ledger to another ledger with no central authority. That’s what needs to be invented.

When asked if fully offline zero-knowledge technology-secured private transfers were close to practical implementation, Buterin said the tech know-how is already there, but there are still limitations:

“We basically know how to do it, but with the limitation that any solution depends on trusted hardware and/or post hoc enforcement against double-spenders.”

MD: So basically what is it he thinks he knows how to do then?

Crypto payments exec thinks crypto won’t replace fiat

MD: Oh please! What’s with this “fiat”? See how their improper use of terms just throws a wrench in the works?

While crypto payment solutions are becoming more common, Mercuryo co-founder and CEO Petr Kozyakov has said that crypto will not replace fiat.

MD: And did his say that, somehow knowing everybody knew what he was talking about? Does everybody know what this “fiat” term means?

Kozyakov told Cointelegraph in an interview that crypto payments are seeing an increase in demand and adoption.

However, the executive said that instead of cryptocurrencies fully replacing fiat money as a payment method, the two payment options will coexist.

MD: Is that different than saying “cash” and “currency” and “checks” and “credit cards” and “debit cards” and ATM machines should coexist?

Kozyakov told Cointelegraph that people will use crypto when it’s easier and more practical.1,1375

MD: What makes it “hard” and “less practical”? Are these people of value? Are they paid (i.e. do other people give money to them for putting out this nonsense). How advanced must a society become to be so confused about value?

MD: Here at Money Delusions we’re well aware that they don’t teach you anything about money. And those of you who think you know… well, let’s see. We annotate this article.

The Original Matrix – What They Don’t Teach You About Money

“You take the blue pill – the story ends, you wake up in your bed and believe whatever you want to believe. You take the red pill – you stay in Wonderland and I show you how deep the rabbit hole goes.”

– Morpheus, The Matrix

What is Money?

MD (MoneyDelusions): Watch how long he goes on before he tells you what money is. We’ll flag it when we see it. If you want to cut to the chase, read the right sidebar. You’ll know in less than 300 words

Some things in life are so deeply ingrained in our daily existence that we rarely stop to question them.

They are simply there, operating in the background, so fundamental to our existence that they feel as natural as the air we breathe.

We use them, rely on them, and move through the world assuming they are exactly as they should be.

For example, everyone is familiar with the phrase “Money makes the world go ‘round.”

This is rarely questioned and is rather accepted as self-evident.

Every day, you wake up, pay your bills, go to work, and check your bank account,—believing that you understand the system you operate within.

But have you ever stopped to ask yourself: What is money, really?

Not the textbook definition.

Not the economic theory you learned in school.

But the truth.

Money is everywhere. It dictates who eats and who starves, who rises and who falls. It builds empires and crushes civilizations.

It has fueled revolutions, financed wars, and controlled the fate of entire nations.

It is arguably the most powerful force on Earth, yet most people never stop to question its origins, its purpose, or its true nature.

You use money every single day. You earn it, you spend it, you save it. You trade your time and energy for it. It determines where you live, what you own, and the opportunities available to you.

It is so deeply embedded in your life that questioning it feels absurd—like questioning gravity or the air you breathe.

But have you ever wondered who decided what money is? Who, or what, gave it value? Or who controls it?

MD: Now that’s kind of provocative don’t you think? We’ll show that money stems directly from trade. Nobody “decided” it. It’s just obvious. Consider trade. There are 3 steps: (1) Negotiation; (2) Promise to Deliver; (3) Delivery. After the trade is agreed upon in step (1), if this is a Simple Barter Exchange (SBE), steps (2) and (3) happen simultaneously on the spot. One “object” is traded directly for another “object”. The most common object in every SBE is money in one of its forms. For trades spanning time and space, money facilitates steps (2) and (3). It may already exist and held by one of the traders or either trader may “create” it specifically for this trade. A good example is buying a car with 48 equal monthly payments. One trader makes the promise and creates the money. The other trader takes the money and his deal is done. But the trader creating the money has 48 more steps before he is done. Each month he brings (to the process) his 1-month’s payment; it is destroyed; and the remainder of his promise is reduced by that amount. It’s just that simple.

And more importantly—what if you have been playing a game where the rules were rigged before you were even born?

MD: And you know what? That’s exactly what you have been doing. And you know what else. You can stop it just as soon as you and your trading partners choose to stop it. The “real money process” (RMP) is in control. And it works because the money creation/destruction activity is never anonymous and is always totally transparent.

For those who are willing to look beyond the surface, the answers may be surprising.

But be warned: once you start asking the right questions, there is no turning back.

MD: Getting pretty exciting isn’t it!

Traditional Definitions of Money

Money is one of the most universally recognized yet least examined aspects of human civilization.

It influences every facet of our lives, dictating our economic opportunities, shaping global trade, and acting as a central force in ways few ever consider.

Yet, despite its ubiquity, money remains a concept that is deeply misunderstood.

MD: Including by the writer of this article. This is always such fun.

While we all use money, few of us ever stop to truly evaluate what it is, how it functions, and whether it works the way we assume it does.

The goal here is not to convince anyone of a specific perspective but to think critically about money—what it really represents and whether the reality matches what we have been taught.

MD: Your best clue is seeing where it is created and by whom. And your clue is seeing where it is destroyed and by whom.

If you were to stop someone on the street and ask them whether they knew what money was, they would almost certainly respond with a confident yes.

MD: Just as this guy might do… probably after he’s made you read all the way to the bottom… holding you in suspense. But we’ve tricked him. You already know the punch line. I think he’s paid by the word so let’s just try to sit back and relax..

However, if you pressed them further and asked them to give a proper definition, the response might not come quite as quickly. The initial certainty would likely give way to hesitation as they search for an answer.

Were you to push a little harder or direct the question toward someone well-versed in finance or economic theory, the answers would likely become more structured.

At this level, people might begin describing the attributes associated with a strong form of money—qualities that make it function effectively as a medium of exchange, store of value, and unit of account.

If the conversation were to then go even further, those thinking critically about the question might move past the attributes of money and instead focus on what money actually does.

They might start discussing its role in facilitating trade, its function in settling debts, or its importance in economic transactions.

Yet, even if all of these points are accepted as true, the core of the question still remains: What “IS” it?

At its most fundamental level, a medium of exchange must be some “thing.” And what are tangible things made of?

MD: Ok. He still hasn’t told us what money is. Here’s a hint. Let’s see how long he goes before he tells you this: Money is provably “an in-process promise to complete a trade spanning time and space”. We’ll discuss its attributes as he moves along. No commodities are money. Commodities change value as their supply/demand balance changes. “Real” money doesn’t do that. “Real” money is a “process”. So right out of the box he’s getting it wrong… but maybe he’ll teach you some chemistry.

Commodities.

By this reasoning, money—when stripped to its most basic form—is a commodity.

And commodities are made up of elements found on the Periodic Table. However, not just any commodity (or any element) can serve as money.

MD: I guess he wasn’t aware that at the time USA became USA, tobacco leaves were used as money. Look below. Is it in the periodic table?

If a particular commodity is widely demanded and possesses some (or all) of the attributes that define strong money, then it ceases to be just a commodity and instead also transcends to become money itself.

At this point, it often becomes clear that money is the most marketable commodity, a good that serves as the final extinguisher of debt and that has been selected by free market forces over time.

MD: Tilt! Since money is a “promise”, the final extinguisher of debt is “delivery as promised”. It’s not selected by free market forces over time. It’s obvious from seeing it actually created by a trader like you and me. And it’s proven by that same trader as he completes his “delivery as promised”, and the money for the trade has been totally destroyed in the process.

This definition resonates with many who have studied the history of money and how different forms have evolved over time.

MD: You know what? We know of no instance of all time that a “real money process” has ever existed. We’ve had lots of stand-ins like precious metals, sea shells, big rocks with holes in them, and even IOU’s. Surprisingly, the IOU is the only thing that comes close to being money. But IOU’s only work between those two traders. Money is IOU between the creator and the RMP (Real Money Process). As he continues to distort we’ll slowly reinforce the truth and you’ll see clearly how it works.

Taking this concept a step further, and recognizing that money is a commodity, and commodities are made up of elements from the Periodic Table, one might even evaluate the various elements to see which of them has the most attributes which would allow it to “ascend” to become money.

MD: Wrong… money is not a commodity. And wrong… even all stand-ins are not in the Periodic Table. In fact, today only one is… Gold. That had a fight towards the end of the 19th century too as William Jennings Bryant claimed Silver was money (they’d just found a bunch in Nevada)… but the powers to be said it was not… and it thus was not.

And, as always happens, we want to stop him right here. He’s got it wrong. We can prove he’s got it wrong. We know with this false premise everything to follow will be wrong. Normally I’d advise you to quit reading and move on to the next article. But, though “time is money”, sometimes it’s worth the grind to follow along.

In doing so, one would realize that there in one commodity that has long been regarded as one of the strongest forms of money due to its unique set of attributes, which make it highly effective as a medium of exchange and store of value.

One of its most defining qualities is durability—unlike paper currency or other perishable goods, it does not corrode, tarnish, or degrade over time, ensuring that it retains its value across generations.

MD: Earth to whoever this is. Accounting records do not corrode, tarnish or degrade. And in a “real money process” where money perpetually maintains perfect supply/demand balance, it’s value never changes. No other exchange media cans claim that.

This durability allows it to function as a reliable form of wealth preservation, as it does not succumb to the forces of time or environmental conditions.

MD: But that’s not an issue. A promise has a fixed time and place it agrees to be delivered. Time is contracted. Environmental conditions are of no import whatever. We’re in a blizzard of false premises.

Another critical characteristic of this commodity is its divisibility.

MD: If you know how to divide or multiply or add or subtract, you know everything you need to know about “real” money. With every other money you need exponentiation. With real money you don’t.

Unlike other commodities, it can be melted down and divided into smaller units without losing its intrinsic value, allowing for transactions of varying sizes.

MD: Maybe so… but money isn’t a commodity. Is this guy one of those Mises Monks?

This makes it more practical as a medium of exchange compared to goods that cannot be easily broken down.

MD: Alright. This is a good time to introduce the obvious proper unit for money. It is the “Hour Of Unskilled Labor” (HUL). It trades for the same size hole in the ground over all time and space. We’ve all traded our time for a HUL early in our lives. We baby sat. We mowed the lawn. We worked at McDonalds. They call it the minimum wage. People who recognize the “real money process”, can recognize a HUL. A HUL traded for the same size hole in the ground 3,000 years ago as it trades for now. And you can talk in 1/2 HULs if you want. Time can be more easily divided than any commodity can. And like HULs it trades for any fraction you want. It never changes over all time.

Additionally, it is fungible, meaning that each unit is identical to another unit of the same weight and purity. This interchangeability ensures that it can be exchanged without discrepancies in value, making it a highly efficient means of trade.

MD: This is obviously a Mises Monk. What attributes do we have now: (1) Durable; (2) Divisible; (3) Fungible;

It is also prized for its portability.

Despite being a physical commodity, it possesses a high value-to-weight ratio, allowing individuals and institutions to transport significant amounts of wealth in a compact and convenient form.

MD: “Real” money is just about record keeping. It’s value to weight ratio is perpetually “infinite”. The cost to transport it is perpetually “zero”. Can whatever this wonderful this guy is peddling… can it meet those metrics?

This portability, combined with its recognizability, reinforces its status as a widely accepted and trusted form of money.

MD: So is he claiming two more attributes: (4) value to weight ratio; and (5) recognizability. You know, I’m 80 years old. The only money I’ve ever experienced is the dollar, and its fractions and multiples. And when I was a kid, the paper version said “Silver Certificate” on it and you could demand silver for it… which nobody did. And in 1964, the coins had 90% silver in them. But in 1965 they quit putting silver in them… but they still traded for the same amount of gas. That proved beyond all doubt that people just viewed them as tokens of no intrinsic value at all. It’s obvious for all to see. She still hasn’t mentioned gold yet had she. Let me check. Nope. Still hasn’t mentioned it. But I know where this nonsense is going. It’s going where is always goes… and has never been in my lifetime or my dad’s lifetime.

Across cultures and throughout history, it has been universally acknowledged as a store of value, and its distinct appearance and unique properties make it difficult to counterfeit.

MD: Difficult to counterfeit? They can plate tungsten and unless you hit it with a tuning fork, you can’t tell the difference. Do these Mises Monks have just one essay to copy?

Beyond these qualities, it also holds scarcity, a fundamental attribute that has preserved its value over time.

MD: (6) Scarcity. Now why in the world would you want money to be scarce? You want it to be in free supply over all time and space. It is used for trade. You never want to inhibit trade. We’re up to 6 attributes and he still hasn’t mentioned his magic commodity… but we know it meets none of these 6 attributes.

Its supply is naturally limited by the physical constraints of extraction and production.

MD: You don’t want to limit supply. You want to maintain perfect supply/demand balance for money. Otherwise it doesn’t hold its value. It either becomes more valuable, which hurts one trader. Or it becomes less valuable, which hurts the other trader. The only time it works at all is for SBE… if anybody takes it these days. I guarantee you, WalMart doesn’t.

This inherent scarcity prevents artificial inflation and ensures that it maintains its purchasing power over extended periods.

MD: Prevents artificial inflation? When was Ft. Knox last audited. What was its value in 1973 when Nixon changed its value. It doesn’t work folks! And we still don’t even know what “it” is. Is anyone still reading this nonsense?

Lastly, its malleability adds to its utility, as it can be shaped into coins, bars, or intricate jewelry without losing its essential properties.

MD: (7) Malleability. Now really. How many shapes can a promise take on? You either keep it or you don’t. And the “real money process” (RMP) knows at all times. The instant you DEFAULT on your promise, the RMP is collecting INTEREST of like amount to make up for irresponsibility. Who pays the INTEREST. Well responsible traders don’t. They enjoy zero INTEREST load. So that leaves irresponsible traders.

This adaptability makes it highly versatile, further cementing its place as one of the most effective and enduring forms of money.

We are, of course, talking about gold.

MD: Finally the cat’s out of the bag. Why doesn’t silver qualify? Why doesn’t platinum? Why doesn’t gold plated tungsten? And if you have to wait for gold to become money, what do you trade with in the mean time? How do you get dirt turned into gold so you can pay the people that are digging it and turning it into gold?

And indeed, throughout history, gold has embodied all the qualities of strong money—it is scarce, durable, divisible, portable, and widely recognized.

MD: And in my lifetime, which is now 80 years, it has never been used as money… not once. In fact, I traded some of my dollars for gold with GoldMoney.com 20 years ago. To test their concept, I asked for my gold… and I got it in gold grams… less 10% import duty. How’s that for money? How’s that for holding value? And now they’re asking for all kinds of information they never asked me for when I made the trade of dollars for gold grams. And if I don’t give them the information, they won’t even let me see my records. And they’re right now in the process of making it more expensive to have my dollars (or what is in their vault) turned into the units of gold grams. Look them up. GoldMoney.com. See if you want to do business with them. Or go to your local pawn shop and see what you have to pay over spot price to get some. And it’s been that way my whole life, which is longer than the Mises Monk writing this article has been around, I guarantee that!

Its long-standing role in economic systems has led many to assert that it remains the ultimate form of money.

MD: The only ones I know asserting that are the Mises Monks… and they’re provably dead wrong.

At this point, a show of hands might reveal broad agreement with this perspective.

MD: No hands go up. Maybe some fists!

But before reaching a final conclusion, it is worth pausing and asking: Has history always functioned under a free-market system?

MD: When I bought my last Timex watch it did. It even said on the box… fair market price… and it was the same wherever you bought it. In fact, virtually everything I have bought was for the published priced. You don’t barter in the USA like you do in Mexico.

More importantly, has money always been determined by the free market, or has another force been at play?

MD: Ask Russia. USA isn’t a nice trading partner. They sanction their trading partners and take over their accounts. Right Russia?

Money as a State-Controlled Construct

A common assumption that must be accepted when using the definition of money found above, is that markets operate freely, driven by voluntary exchange and competition.

But does this match with historical reality?

Has history always been characterized by a Free Market? Or, more importantly, has the world ever been truly governed by Free Market principles?

MD: But that’s not because of the money.

These questions are essential, but they require us to look at the world as it is, not as we wish it to be. Which leads to a broader discussion about the nature of money itself.

If we assume that money is simply a commodity chosen by free market forces, then we must reconcile this assumption with historical evidence.

MD: Bad assumption. Money is “simply a promise to deliver spanning time and space”. It’s provable. Historical evidence won’t help us because governments have conned us over all time. The money-changers institute governments to do just that. I really intended to go through this whole thing… but I just can’t. How about you? I’m outa here!

And the simple fact is, there exists another perspective—one that challenges the traditional definition of money and forces us to reconsider whether money has ever been purely a market-driven phenomenon.

If history tells us anything, it is that the state has played a significant role in the shaping of history as a whole. The state has also played a significant role in the development of monetary systems.

So, if we are dealing with the world as it actually is, rather than how we want it to be, this simple fact cannot be ignored.

Throughout history, governments have issued various forms of fiat currency, not as a response to free market demand, but as a mechanism to facilitate trade, assert control, and support economic systems.

Ancient empires often minted coins made of base metals, stamping them with the images of rulers or state symbols, ensuring that their value was determined by decree rather than intrinsic worth.

These early monetary systems established a precedent where the state, rather than market forces, dictated what functioned as money.

During the Renaissance and beyond, paper banknotes emerged as a widespread monetary tool. Initially, these notes were backed by precious metals, reinforcing their legitimacy and trust.

However, over time, they gradually evolved into pure fiat money, entirely detached from any physical commodity.

This transformation allowed governments and central banks to exert greater control over monetary systems, as they were no longer constrained by finite reserves of gold or silver.

Colonial governments also played a significant role in monetary history, issuing promissory notes as a means of managing trade and economic activity.

These notes functioned as early forms of government-backed currency, representing an obligation rather than a tangible store of value.

As time progressed, fiat currencies became the dominant form of money, with modern states embracing national currencies such as the dollar, euro, and yen.

Today, fiat money exists in both physical and digital forms, serving as a testament to the continued evolution of state-sponsored monetary systems.

If we accept this historical reality, then we must ask: Is money truly a product of free markets, or has it always been shaped and defined by those in power?

Or put another way: Is money really the most marketable commodity that is chosen by the free-thinking individuals, or is it a powerful tool that is dictated by the King?

To answer these questions, it is first necessary to develop the skills needed to best understand one’s environment.

Situational Awareness

Situational Awareness is a fundamental skill that allows individuals to perceive, comprehend, and anticipate events in their surroundings, enabling them to make informed decisions and take effective action.

It consists of three essential components: first, the ability to perceive critical elements in the environment, such as people, objects, and unfolding events; second, the capacity to comprehend their meaning and potential impact; and third, the foresight to project future developments based on available information.

This skill is indispensable in high-stakes environments such as aviation, military operations, healthcare, and business, where the ability to recognize subtle cues and react accordingly can mean the difference between success and failure.

The same principle applies to portfolio allocation, where financial markets constantly shift, and a lack of awareness can lead to devastating losses.

Beyond professional fields, situational awareness plays a critical role in everyday life, enhancing personal safety, improving decision-making, and allowing individuals to navigate an ever-changing world effectively.

Without this skill, people risk being caught off guard, making poor choices, and suffering avoidable consequences.

Whether applied to personal security, financial decisions, or strategic thinking, situational awareness is a vital tool for optimizing outcomes in a world filled with uncertainty.

An example of applying situational awareness to our current topic at hand can be found in the below scenario.

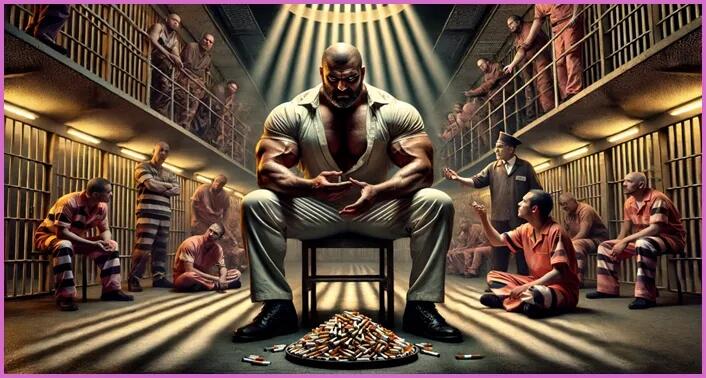

The Prison Economy

As noted above; to optimize one’s circumstances, it is necessary to fully understand the environment in which one operates.

This principle is starkly illustrated in the closed ecosystem of prison economies, where traditional monetary systems do not exist.

In such environments, inmates rely on alternative forms of currency, selecting goods that are durable, widely accepted, and easily exchangeable.

For example, cigarettes have historically functioned as an effective currency behind bars.

They are in high demand, easily divisible for small transactions, and widely recognized as a unit of exchange.

Cigarettes can be traded for food, services, or other necessities, creating a barter economy that mirrors traditional financial systems.

Similarly, cans of sardines have emerged as a valuable commodity in some prison settings.

Their non-perishable nature, combined with their nutritional value, makes them a reliable store of wealth that retains its usefulness over time.

In the absence of officially sanctioned money, these items take on the characteristics of a medium of exchange, a store of value, and a unit of account—the very principles that define money itself.

This informal economy within prisons serves as a microcosm of broader monetary systems, demonstrating that money is not defined by government decree alone, but by what people collectively recognize as having value.

The lessons from these controlled environments underscore the importance of adaptability, resourcefulness, and understanding economic forces, no matter where one operates.

Its also important to understand that while both cigarettes and sardines have become popular forms of money found in controlled environments, they have not become so solely due to the marketability of their intrinsic qualities.

Consider a scenario within a prison economy, where sardines are widely accepted as currency. In this system, they serve as a medium of exchange, a store of value, and a unit of account—fulfilling all the necessary functions of money.

However, what happens when an inmate is transferred to a different facility, where the power dynamics have changed?

In this new prison, the dominant figure—the one who holds the most influence—hates sardines but loves cigarettes.

He has declared, by fiat, that cigarettes are now the required form of payment.

In such an environment, it no longer matters that sardines once held monetary value. The rules have changed, and the new authority figure has dictated a new system.

In this situation, would it make sense to insist that sardines are still money?

Or would the prisoner be forced to adapt to the new standard, recognizing that money is not determined by intrinsic qualities alone, but rather by the power structures that enforce its use?

Would you take it upon yourself to try and convince the dominant figure that he is wrong to demand cigarettes and that he should rely on free market principles rather than his own wants and desires?

This example raises a critical question: If given the choice, would we prefer a market-based form of money, determined organically by free exchange, or a system where money is dictated by a central authority that holds power over the participants?

Most people would instinctively lean toward the former, believing that free markets should determine the best form of money.

And because they believe that free markets would be better, they then believe that that is how markets developed throughout history.

However, there is a problem with this perspective—one that is rarely acknowledged.

Despite its widespread acceptance in economic textbooks and theoretical models, there is little historical evidence that large-scale barter and free exchange ever formed the foundation of monetary systems.

The assumption that markets naturally produce money without some form of imposed structure does not align with much of the historical record.

This challenges the idea that money evolved as a product of free markets and forces us to reconsider whether its origins are more closely tied to power, authority, and enforced rules rather than voluntary exchange.

Most people assume money has always been determined by free market forces. But history tells a different story—one where power, control, and coercion have shaped financial systems in ways few ever stop to consider.

So if money isn’t what we think it is, what does that mean for everything else?

Debt, Power, and the Evolution of Money Systems