Mises Monks are a term we associate with those who worship Ludwig Von Mises … and his disciples. They think gold is money … and “sound money” to boot. They are clueless about money … but well funded and noisy … and dangerous.

On page 81 of Democracy in Chains Nancy MacLean describes John C. Calhoun’s “case for minority veto power” – that is, Calhoun’s proposal that no legislation be enacted unless it receives the approval of “the concurrent majority” – as being “like that which Buchanan and Tullock were advocating” in The Calculus of Consent. She’s mistaken. Significant differences distinguish Buchanan’s and Tullock’s proposal from Calhoun’s proposal of a concurrent majority.

The most important of these distinctions is the one mentioned in my correction of Michael Chwe’s misunderstanding of Buchanan’s proposed unanimity rule – namely, for Buchanan and Tullock, the only rules which require unanimous consent are constitutional rules, including the rules that determine the procedures and requirements for enacting legislation. Buchanan and Tullock argued that, when choosing constitutional rules, individuals would recognize that a rule of unanimity for the enactment of ordinary legislation would be too costly. At the constitutional stage of decision-making, therefore, individuals unanimously agree to have some rule of less-than-unanimity – for example, majority rule – for the enactment of legislation. More precisely, Buchanan and Tullock argued that, at the constitutional stage, individuals might choose different rules for the enactment of different kinds of legislation. For example, individuals might choose to allow tax rates to be changed with the approval of a simple majority, while proposals to declare war must receive the approval of two-thirds of the citizens’ representatives. The relevant point here is that the rule of unanimity for Buchanan and Tullock – unlike for Calhoun – applies only to the making of constitutional rules and not to the enactment of legislation.

Another important difference between Buchanan’s and Tullock’s proposal and Calhoun’s is that, for Buchanan and Tullock, the unanimous approval that is required is that of individuals; for Calhoun, the unanimous approval that is required is that of groups. Calhoun thought of society as being naturally comprised of different “interests” – for example., planters, merchants, and lawyers. As explained by Alex Tabarrok and Tyler Cowen in their 1992 paper on the extent to which Calhoun anticipated public choice,

Calhoun’s thought on the question of optimal consent is clearly related to pluralist or corporatist “group theory.” In particular, Calhoun’s concurrent majority applies to interest groups and not individuals [p. 666]…. Unlike Buchanan, Calhoun does not subscribe to normative individualism of contractarianism. The social state is thought of as God-given and methodologically prior to civilized man [p. 671].

Each proposed piece of legislation must, under Calhoun’s system, win majority approval from each of the different interests – thus the term concurrent majority.

Unlike Calhoun, no public-choice scholar accepts the idea that among the elemental components of society are different “interests.” Instead, for public-choice scholars, the elemental components of society are individuals. It’s true that public-choice analysis predicts that individuals will often form themselves into interest groups, but such groups are the product of the interplay of the costs and the expected benefits to individuals of so organizing. Unlike for Calhoun’s “interests,” the interest groups identified by public choice are not elemental entities each of which deserves, by right, a say in – and much less a veto power over – the enactment of legislation. (Indeed, the normative attitude of public-choice scholars toward interest groups is decidedly negative, for such groups typically succeed in using state power to secure benefits for themselves at a greater cost to society at large.)

In short, for Calhoun, interest groups are simply assumed to exist, and to exist in such numbers that the interests of all individuals in the polity are thereby represented by this collection of groups. In stark contrast, for public choice, interest groups arise if and only to the extent that the costs to individuals of forming into a group are exceeded by the benefits that each individual expects to receive by joining the group. For Calhoun, the interplay of interests under a system of concurrent-majority rule ensures good government. For public-choice scholars, the political activity of interest groups is among the most important forces that incite government to behave badly.

….

In summary, for Buchanan (and for Buchanan and Tullock) the rule of unanimity was to govern only the enactment of constitutional rules and not the enactment of legislation. This fact alone renders false MacLean’s assertion that Buchanan’s and Tullock’s proposal is “like” that of Calhoun’s. When other aspects of Buchanan’s and Tullock’s analysis are considered – such as their belief that each individual should have an equal say in the choosing of constitutional rules – the similarity between Buchanan’s analysis and that of Calhoun shrinks even further. Here, again, are Tabarrok and Cowen:

Buchanan has chosen individual preferences as the source of justification for his proposed unanimity rule. For Buchanan, informed consent is the ultimate source of value. The purpose of a political constitution is to allow men to achieve their desired ends. There are no values higher than those given by preferences, and the state is visualized as a hypothetical social compact among autonomous, contracting individuals [p. 672].

None of the above denies that Calhoun (like several other thinkers) anticipated some aspects of public choice. But the normative, methodological, and practical differences between Calhoun, on one hand, and Buchanan, Tullock, and other public-choice scholars, on the other, is so huge that for MacLean to describe Buchanan’s and Tullock’s project as being “like” that of Calhoun’s – and for her to conclude that Calhoun is the “intellectual lodestar” of public-choice scholars – is absurd. If MacLean sincerely believes her charge, then she either has not read carefully Calhoun or public choice (or both), or she is unable to grasp not just the (many) subtleties in these works but also their main thrusts. (Indeed, MacLean admits to having read the Tabarrok-Cowen article quoted above; but, obviously, she did not read it carefully enough to grasp its full message.) Either way, MacLean had no business writing a book about these matters.

Here’s a letter that I sent several days ago to the Washington Post:

In “The beliefs of economist James Buchanan conflict with basic democratic norms. Here’s why” (July 25) Michael Chwe is completely mistaken when he writes that Buchanan wanted to “make the passing of new laws as difficult as possible, requiring unanimous consent.” Buchanan argued for unanimous consent only to constitutional rules; he emphatically did not argue for unanimous consent to legislation enacted under any existing constitution. Indeed, the very point of the most famous chapter (#6) of his most famous book, The Calculus of Consent (co-authored with Gordon Tullock), is to explain why unanimous consent to ordinary legislation is an unworkable and, hence, unacceptable idea.

Central to Jim Buchanan’s life’s work was the distinction between choosing constitutional rules and choosing legislation and regulation within constitutional rules. It’s unfortunate that Prof. Chwe misses this key distinction and, in the process, portrays Buchanan in an exceedingly misleading light.

Sincerely,

Donald J. Boudreaux

Professor of Economics

and

Martha and Nelson Getchell Chair for the Study of Free Market Capitalism at the Mercatus Center

George Mason University

Fairfax, VA 22030

… is from this speech, which I believe was delivered sometime in the late 1970s or early 1980s, by the late, great Milton Friedman (who was born 105 years ago today):

You must separate out being pro free-enterprise from being pro-business. The two greatest enemies of the free enterprise system, in my opinion, have been on the one hand my fellow intellectuals, and on the other hand, the big businessmen – for opposite reasons.

Ethereum Co-Founder Responds To Sweden’s Cashless-Society Rethink

MD: We never know what we’re going to get into with these “cyber money” articles. Looks like someone’s having reservations about how well it works. And is it correct to refer to it as “cashless”?

If I have a $100 bill and I take it to a gas station and trade it for a tank of gas and $50 in change that’s a “cash” transaction. The gas station now has a $100 bill in their cash register. And they have one less $50 bill there. Further, they have $50 less gas in their buried tank. And I have $50 worth of gas in my truck. And I have a $50 bill in my wallet where I once had a $100 bill.

Now, does anything change if I give the gas station a debit card… or a credit card… or the gas station’s own branded credit card? It’s all just accounting. It’s all just moving “cash” around. Or is it? There’s an important distinction between a “debit” card and a “credit” card.

With a “debit” card, you have something keeping track of “cash you have”. With a “credit” card you have something keeping track of “cash you create”… cash you “don’t” have… cash you must return to complete your promise. Cash you have is an “in process promise to complete a trade spanning time and space” You don’t know who made that promise. You do know it wasn’t you. You are using it as the most common object in simple barter exchange.

But what about the “credit” card. It’s about “cash you create”. And when you “create” cash, “you” are making the “promise to complete a trade spanning time and space.” And it is “you” who must deliver on that promise. But it’s still cash. It’s still money. But it’s not money “you” have. It’s money the creator of the credit card has. These are terms referring to the same thing. At the end of the month you “pay” off your credit card… usually by making a deposit in an account. And what do you deposit in the account? Probably a check from your employer.

And that check from your employer… what is that? It’s a token that will eventually take cash out of his account and transfers it into your account. That is now a principal function of a bank. It’s a banking function that they charge you for.

In the beginning, it was no function of a bank at all. The function of a bank was to keep people from stealing your valuables… whether in a safe deposit box, or in their vault holding gold and silver… things people “believe” to have value. And you paid the bank for that safe keeping. And in the end, the bank occasionally lost your gold and silver… and said “sorry… it’s gone!”

So, are we clear what “cash” is? Are we clear that the term “cashless” is meaningless?

As Sweden reconsiders its push toward a cashless society, Ethereum co-founder Vitalik Buterin highlighted the fragility of centralized digital payments and the opportunity presented by decentralized payment alternatives.

MD: “Fragility of centralized digital payments”. I think this is the “thesis statement” of this article. Let’s keep it in mind as we proceed.

In recent years, Sweden has led the charge toward a cashless future, with digital payment platforms becoming widespread. However, as concerns over cyber-threats, civil defense and instability have emerged, Swedish authorities are now actively encouraging citizens to keep some cash.

MD: What he’s really saying is “keep your cash as stuff rather than as numbers in a ledger”. And is a token representing numbers in a ledger stuff? Well, we’re seeing how confused these geniuses are, aren’t we.

Buterin noted the reversal illustrates that while centralized solutions may be efficient, they may not be reliable during times of crisis.

MD: If tokens (i.e. stuff) representing numbers in a ledger is not a “centralized solution”, then what is it? Would it be better to call it a “universal” solution? I think so.

“Nordics are walking back the cashless society initiative because their centralized implementation of the concept is too fragile,” Buterin wrote, citing a March 16 article by The Guardian. “Cash turns out necessary as a backup.”

MD: Ethereum claims to be money. It falsely assumes that by keeping track of “pure waste” of electricity, money is created. And Ethereum is the ledger that keeps track of that. It’s obviously silly… but that’s the concept. They call it “proof of work”. And now they’re suggesting that that number in the ledger is actually worthless… even though it stands for actual waste. And as a backup, you should keep some “cash”. Now tell me, where did the cash come from?

A former central bank official predicted in 2018 that Sweden would be cashless after seven years. In 2025, the prediction mostly held, with only one in 10 transactions in the country being done in cash, according to The Guardian.

MD: This “one in 10” is probably a made up statistic. Do you really think it’s somebody’s job to keep track of so-called “cash” transactions as distinct from “non-cash” transactions?

Still, while the Nordic country was an early adopter of digital payments, its government published a brochure encouraging citizens to keep a week’s worth of cash in case of war or crisis. Sweden’s reconsideration has revealed the issue of centralized digital payment infrastructure remaining reliable in times of instability, Buterin suggested.

MD: “… in case of war or crisis…” This suggests that this ethereum stuff disappears or is otherwise inaccessible in some situations. And this isn’t true of what they’re calling cash… which is presumably “currency” and “coin”… tokens that don’t disappear for some reason. That suggests, if we are to have a truly cashless society, we need an indelible record. Could an SD card be made to act like an indelible record? It could if it could be encrypted with a password that only the owner knows. An invention is needed here.

Buterin said Ethereum can be a decentralized financial fallback in times of crisis. “Ethereum needs to be resilient enough, and private enough, to be able to credibly play this kind of role,” Buterin said.

MD: Seems to me what we need is a process that moves numbers from one ledger to another ledger with no central authority. That’s what needs to be invented.

When asked if fully offline zero-knowledge technology-secured private transfers were close to practical implementation, Buterin said the tech know-how is already there, but there are still limitations:

“We basically know how to do it, but with the limitation that any solution depends on trusted hardware and/or post hoc enforcement against double-spenders.”

MD: So basically what is it he thinks he knows how to do then?

Crypto payments exec thinks crypto won’t replace fiat

MD: Oh please! What’s with this “fiat”? See how their improper use of terms just throws a wrench in the works?

While crypto payment solutions are becoming more common, Mercuryo co-founder and CEO Petr Kozyakov has said that crypto will not replace fiat.

MD: And did his say that, somehow knowing everybody knew what he was talking about? Does everybody know what this “fiat” term means?

Kozyakov told Cointelegraph in an interview that crypto payments are seeing an increase in demand and adoption.

However, the executive said that instead of cryptocurrencies fully replacing fiat money as a payment method, the two payment options will coexist.

MD: Is that different than saying “cash” and “currency” and “checks” and “credit cards” and “debit cards” and ATM machines should coexist?

Kozyakov told Cointelegraph that people will use crypto when it’s easier and more practical.1,1375

MD: What makes it “hard” and “less practical”? Are these people of value? Are they paid (i.e. do other people give money to them for putting out this nonsense). How advanced must a society become to be so confused about value?

MD: The Mises Monks are always great fodder for illustrating the spread of confusion and delusions as to what money “really” is. Let’s dissect this one.

One of history’s greatest ironies is that gold detractors refer to the metal as the barbarous relic. In fact, the abandonment of gold has put civilization as we know it at risk of extinction.

MD: How’s that for an opening line? The Monks never disappoint. “Greatest Ironies”; “gold detractors”;” barbarous relic”: Yet they never seem to be able to tell us what money really is. But this may be going too far. Removing “gold” will “risk extinctions”?

Gold’s main use is in jewelry and plating electrical contacts. Once used to fill teeth, it’s been a very long time since gold was used for that (except for Negros who use it to decorate their faces.) And in no lifetime of anyone living today has gold served as money. And silver ceased serving as money in 1965…almost 10 years before Nixon declared the obvious…that the so-called gold backing of the dollar was a giant fiction…a fraud on which the French called them out.

The only risk to extinction was use of mercury amalgamating silver to fill teeth. It was shown to be poison…like lead in paint and gasoline. Precious metals have never been money. They are just clumsy expensive stand-ins for what money really is…”a promise”. And what do these Monks call real money? They call it “fiat money”…and make it a derogatory slur. Since when is a “promise” derogatory. Let’s continue.

The gold coin standard that had served Western economies so brilliantly throughout most of the nineteenth century hit a brick wall in 1914 and was never able to recover, or so the story goes. As the Great War began, Europe turned from prosperity to destruction, or more precisely, toward prosperity for some and destruction for the rest. The gold coin standard had to be ditched for such a prodigious undertaking.

MD: Served economies “brilliantly”? Economic panics were as regular then as pandemics are becoming today. And in 1913 (a year before this so-called brick wall), the Federal Reserve Act began to plague us with the money we have today…a money that States freely counterfeit…and that money-changers collect interest on…and that both manipulate to deliver the so-called “business cycle”. “Prodigious undertaking”? Oh please!

If gold was money, and wars cost money, how was this even possible?

MD: A Mises Monk might be close to getting something right here. You can’t support a war if you can’t pay for it. And if gold is money…with only about one ounce per person on Earth (less than $2,000)…you’re not going to support war with gold. But you can by counterfeiting. They claim Lincoln did this to finance the USA Civil War in the 1860’s…and that’s correct. But when that counterfeit money (Greenbacks) was paid back, it ceased to be counterfeit. It “proved” to be “real” money. That hasn’t happened with any war since. The State just rolls its counterfeit money over by taking out new loans to pay off the old.

First, people were already in the habit of using money substitutes instead of money itself—banknotes instead of the gold coins they represented. People found it more convenient to carry paper around in their pockets than gold coins. Over time the paper itself came to be regarded as money, while gold became a clunky inconvenience from the old days.

MD: Well, the Monks being right didn’t last long did it? Here at Money Delusions we know money is an “in-process promise to complete a trade spanning time and space”. It is only created by traders like you and me. It begins as a ledger entry…open to all to see. And it ends with delivery on the promise and reversal of that ledger entry documenting the promise…again for all to see. In the interim it may remain a ledger entry; it may become a “demand deposit” (i.e. check); it may become a paper chit (currency); it may become a token (a coin). As such, it becomes the most common object of every simple barter exchange. But in the end it becomes a reversing entry in a ledger and is extinguished forever…for that trading promise. And if the promise is broken (defaulted) an “interest collection” of like amount is immediately made to recover the “orphaned” money. This guarantees perpetual perfect balance of supply and demand for the money itself…and thus zero “inflation”.

Second, banks had been in the habit of issuing more bank-notes and deposits than the value of the gold in their vaults. On occasion, this practice would arouse public suspicion that the notes were promises the banks could not keep. The courts sided with the banks and allowed them to suspend note redemption while staying in business, thus strengthening the government-bank alliance. Since the courts ruled that deposits belonged to the banks, bankers could not be accused of embezzlement. The occasional bank runs that erupted were interpreted as a self-fulfilling prophecy. If people lined up to withdraw their money because they believed their bank was insolvent, the bank soon would be. People had no idea their banks were loaning out most of their deposits. They did not know fractional reserve banking, a form of counterfeiting, was the norm.

MD: That’s not a “habit”…it’s by design. Money-changers instituted the State. The State chartered the Banks (owned by the Money-changers)…and gave them a 10x leverage advantage over traders like you and me. And when those scoundrels abused even that enormous privilege, the State they created defended them…as designed. It’s not a government-bank alliance. The State is a “creation and tool” of the Money-changers. And the State fiction of Laws sealed the deal. They pass one law that dilutes the golden rule and bammo…everything else that isn’t against the law (but violates the golden rule) is suddenly legal. And that obvious problem created here brings us 40,000 new laws each year…trying to put the Genie back in the bottle…trying to make us comply with that one simple golden rule.

And why didn’t the people know this was going on? Because there was “secrecy” in banking. Money requires “authentication” of the trader creating it and “transparency” of the promise to all lookers. And “defaults” are evident to all lookers “immediately”…and immediately mitigated by “interest collections” of like amount.

Here again, the Monks get close to saying what’s going down. Money “is” fiat…and that’s good. It’s what makes it so efficient in trade. But a “real” money process gives “no” trader an advantage…not even the Money-changers; their States; or their Banks. In this context, the “fraction” is not 10x…but rather infinite to the trader. And there is no reserve. Unlike a water well, you don’t have to prime the pump. But if you don’t replace the water you pump, you don’t get to pump again…until you replace that water. Lots of metaphors going on here.

Gold coin redemption requirements put limits on fractional reserve banking. Such limits were not welcomed by banks. Since banks could loan to the government, limitations also capped government spending, so the government did not like the limitations of gold coin redemption either.

MD: What “coin redemption requirements”? They were always a fiction. Gold coins were never used in my lifetime. And silver coins quit being used in 1964…and changed nothing in the behavior of traders… proving that precious metal was not money. Rather, it was the “token” that was money. At the same time, the paper money which said “Silver Certificate” changed to saying “Federal Reserve Note”…and as far as traders like you and me were concerned, nothing changed.

We never asked for the silver promised by those certificates. We had no use for it. It weighed too much and was too bulky. But for non-traders, the change was large. These non-traders are called “investors”. They’re really just gamblers. And they immediately gobbled up all the silver. You can now buy it on eBay (google “Silver Roosevelt Dimes 90% Junk Constitutional Circulated *Guaranteed Cheapest!”). It sells for (i.e. trades for) $4.50 for 10 dimes…dimes that used to trade for two candy bars…before State counterfeiting withered the dollar to its current condition.

And “government limitations”? Does anyone really believe there is such a thing as a government limitation? All governments are by their very definition “unlimited”!

Which brings us to the wall gold allegedly hit.

Preparing for War Means Preparing for Inflation

In his 1949 book, Economics and the Public Welfare, economist Benjamin Anderson tells us, “the war [in 1914] came as a great shock, not only to the masses of the American people, but also to most well-informed Americans—and, for that matter, to most Europeans.” And yet, Germany, Russia, and France began accumulating gold prior to the war (with Germany starting first in 1912). Gold was taken “out of the hands of the people” and carried to the reserves of the Reichsbank, the German central bank. People were given paper notes “to take the place of gold in circulation.”

MD: It goes all the way back to the Battle of Waterloo! … and for all time before that! All wars are “bankers” wars (i.e. money-changer wars). And if they had a “real money process” back then, they could have taken up all the gold they wanted. Traders had no use for it. There are no “reserves” in a real money process. It’s promises with which we deal. The only thing that can destroy a promise is to destroy the record of the promise…or destroy the person who made the promise. And a “real money process” mitigates such contingencies with “interest collections of like amount.” It’s simple arithmetic. Who pays the interest? Only traders who have a propensity to default pay it. And those traders have to work that much harder if they want to continue to trade at all, because once the defaults get too large, the marketplace ostracizes them.

When war broke out in August 1914, Gary North explains that the pre–World War I policy of gold coin redemption was

independently but almost simultaneously revoked by European governments. . . . They all then resorted to monetary inflation. This was a way to conceal from the public the true costs of the war. They imposed an inflation tax, and could then blame any price hikes on unpatriotic price gouging. This rested on widespread ignorance regarding economic cause and effects regarding monetary inflation and price inflation. They could not have done this if citizens had possessed the pre-war right to demand payment in gold coins at a fixed rate. They would have made a run on the banks. Governments could not have inflated without reneging on their promises to redeem their currencies for gold coins. So, they reneged while they still had the gold. Better early contract-breaking than late, they concluded.

MD: Earth to Monks. You just made our case. You’ve shown that precious metals are no cure to State deviance and malfeasance. A “real money process” has no State sponsorship. It has no Money-changer sponsorship. It has only trader and their marketplace sponsorship. And it depends on “authenticating” the trader and “accounting” for the trader’s promises. By the classical triple “A”s of trade: (1) Authentication; (2) Authority; (3) Accounting; all “responsible” traders (i.e. those with no propensity to default) have equal “authority” to create money. Those with non-zero propensity to default pay insurance “premiums” which are called “interest collections”. And they’re not arbitrarily set in the smokey rooms of LIBOR . They always equal “defaults incurred”. I’ve always wondered why banks always tell us the “prevailing interest”…but never show us the “prevailing defaults”. Now I no longer wonder. It enables their “business cycle”. It enables the “front running”of economic perturbations they themselves cause by “throttling” the money supply …supposedly in the interest of controlling inflation (which they cause) and maintaining full employment (which they can’t control at all).

If governments had not broken their promise to redeem paper notes for gold coins, they would have had to negotiate their differences rather than engage in one of the deadliest wars in history. Abandoning the gold coin standard, which had always been under government control, was the deciding factor in going to war.

MD: Duh! How about we do an “iterative secession”. How about we do without government altogether.

Though the US did not formally abandon gold during its late participation in the war, it discouraged redemption while roughly doubling the money supply. Blanchard Economic Research discusses the situation in “War and Inflation”:

MD: If gold is money, how did they “double” the money supply? These Monks are beyond stupid. In a “real money process”, you can only double money supply by doubling trader promises. And traders don’t make promises they can’t see clear to delivering. But get rid of government and the money-changers that create it and bammo…a doubling of trade would be minuscule.

War also causes the type of inflation that results from a rapid expansion of money and credit. “In World War I, the American people were characteristically unwilling to finance the total war effort out of increased taxes. This had been true in the Civil War and would also be so in World War II and the Vietnam War. Much of the expenditures in World War I, were financed out of the inflationary increases in the money supply.”

MD: When it comes to money, there’s only one type of inflation. That is when supply exceeds demand for the money itself. And this is impossible in a “real money process”. And as we pointed out earlier, the Civil War was different from all following wars. The Greenbacks were “all” recovered (“Greenbacks then became freely convertible into gold“)

Governments had a choice to make: fight a long, bloody war for specious reasons, or retain the gold coin standard. They chose war. US leaders found their decision irresistible. It was not J.P. Morgan, Woodrow Wilson, Edward Mandell House, or Benjamin Strong who would be fighting in the trenches.

When we hear that “going off gold” was the prerequisite for global peace and harmony, we should remember places such as the Meuse-Argonne American Cemetery in France, where grave markers seemingly extend to infinity. These are mostly the graves of young men who died for nothing but the lies of politicians and the profits of the politically connected. Gold wanted no part in the slaughter. But politicians and bankers knew a paper fiat standard was the monetary prerequisite to achieving their goals.

MD: Every time I ask one of the Mises Monks how you can use gold as money when there’s only one ounce per person on Earth? …i.e. less than $2,000…1/2 what someone at Home Depot makes in a month! The line goes dead.

Conclusion

John Maynard Keynes, who coined the term “barbarous relic” in reference to the gold standard, wrote about the world that was lost when gold was abandoned:

What an extraordinary episode in the economic progress of man that age was which came to an end in August, 1914! . . . The inhabitant of London could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery upon his doorstep. . . . He could secure forthwith, if he wished it, cheap and comfortable means of transit to any country or climate without passport or other formality, could despatch his servant to the neighboring office of a bank for such supply of the precious metals as might seem convenient, and could then proceed abroad to foreign quarters, without knowledge of their religion, language, or customs, bearing coined wealth upon his person, and would consider himself greatly aggrieved and much surprised at the least interference. But, most important of all, he regarded this state of affairs as normal, certain, and permanent, except in the direction of further improvement, and any deviation from it as aberrant, scandalous, and avoidable.

If Keynes had read what he wrote, he might have been a better economist. And we might be living in a better world today.

MD: This is shades of the Red vs. Blue; The Donkeys vs. the Elephants; the Harlem Globe Trotters vs. the Washington Generals; the Keynesians vs the Mises Monks. You’re never going to solve a problem when you’re given two choices, both bad, and both controlled by a single non-choice. Such is democracy. Long live democracy.

George Ford Smith is a former mainframe and PC programmer and technology instructor, the author of eight books including a novel about a renegade Fed chairman (Flight of the Barbarous Relic), a filmmaker (Do Not Consent), and an advocate of stateless market government. He welcomes speaking engagements and can be reached at gfs543@icloud.com.

Let’s start with this fact; fiat (paper) currencies die – often spectacularly. That is why precious metals may someday be needed for barter and trade. Anyone who thinks it is silly to worry about such a thing is putting blind faith in Federal Reserve Notes.

MD: Fiat is a derogatory term, usually used by gold bugs who think precious metals are “sound” money. It is a slur against “real” money created by traders and used in a Medium of Exchange (MOE) process. The slur is valid for “improper” MOE processes (the only ones which currently exist in the wild … or anywhere for that matter) but it is totally invalid when referring to a “proper” MOE process as described here at Money Delusions. This opening comment is an overt admission that precious metals are not money …. but rather are something that must be resorted to when money fails.

The U.S. dollar is having a great run, no question. It will soon be 50 years since Nixon closed the gold window, thereby converting the dollar to a purely fiat currency. Five decades is longer than most purely fiat currencies survive.

MD: This is so silly. It implies that the dollar was not a fiat currency before it was proven to be (i.e. the myth that was there all along that it was backed by precious metals was exposed). The dollar has been fiat currency since its inception … and there’s nothing wrong with that. It is improper MOE processes that don’t survive. Try a proper one and it “will” survive.

Humans carry a normalcy bias. That helps explain why so many assume the unbacked Federal Reserve Note, which has served so long as our currency, will continue to serve in the future.

MD: Humans are traders. They know money for what it is … i.e. an in-process promise to complete a trade over time and space. Some create it themselves (e.g. when you buy a car with 60 monthly payments). Most just use money created by others. It is the most common object in every simple barter exchange.

If you test that assumption, it quickly gets hard to defend.

MD: Nonsense. The so-called “backed” coins were removed from circulation at the beginning of 1965. Before that they contained 90% silver. After that they were just worthless tokens. If the “backing” had anything to do with their use as money, the new worthless tokens would not have traded for anything. The same is true when they took the myth “Silver Certificate” off the paper currency and replaced it with the true “Federal Reserve Note”. Nothing changed as far as traders were concerned.

Point to the exponential growth in U.S. debt, the unrestrained government spending throughout both Republican and Democratic administrations, and the extraordinary monetary policies of the Fed (particularly in the past decade) and reasonable people should acknowledge that the reign of “king dollar” is unlikely to last forever.

MD: The US debt has been exponentially increasing from the very beginning. It is the nature of any exponential curve, that in its early existence it looks flat. That’s because its early rate of increase is swamped by the scaling needed to accommodate the later rates driven by the exponent. Our money has exhibited about a 4% inflation rate for all time. It is what has funded our government. All taxes have been absorbed in paying tribute to the money changers who instituted that government. They call it interest on the debt.

Most people don’t know the first thing about the dark history of fiat currencies around the world. Governments use them to borrow and print without limits. Suffer no delusions – fiat currencies were invented for precisely that purpose. The gold in the treasury has never been sufficient for the wars, social programs, and graft which are the hallmarks of a growing government.

MD: Most people don’t care. People using money are traders. With a proper MOE process, so-called investors (and also savers) would use money to hold their wealth until they were ready to dispose of it. With a government objective of a 2% annual leak, and a realized 4% annual leak, this doesn’t work. But for most trades (which are hand to mouth) it’s undetectable. You just institute an increase in “minimum wage” every now and then to make people think they are keeping up.

America is no exception. Nixon slammed the gold window shut because nations – France in particular – saw the U.S. spending beyond its means and devaluing the dollar. So, our trading partners began swapping dollars for bullion. In order to stop the hemorrhaging of U.S. gold reserves, Nixon reneged on the commitment to redeem Federal Reserve Notes in gold.

MD: Actually, France called the USA bluff. When Nixon “slammed the gold window” he removed the myth that the dollar was worth 1/35th an ounce of gold. In the real world it was trading for about 1/70th an ounce of gold. The French decided they would rather have their debts repaid at the rate they were incurred rather than the fraudulent rate the USA government was claiming. If a proper MOE process had been in place, and the money was in units of HULs (Hours of Unskilled Labor), this would not have happened. It is prima-facie evidence that gold is not money and can’t be used to back money. There’s only one ounce of it per human on earth … now about $2,000 … chump change.

Honest money in the form of gold, or currency redeemable in gold, imposes restraints that no expansionist government can abide – ours included.

The chart showing the growth of our national debt since Nixon broke the last remaining tie between the dollar and gold is hard to refute.

MD: These charts never show inflation from 1913 to 1970 … or from 1787 to 1913. The same rate of inflation is there, but just as this curve looks flat on the left, it would look flat if plotted all the way back to 1787. If the plot was honest it would have a log scale on the vertical and would appear as a straight line. Nothing happened in 1970.

Whether or not the federal government can be trusted to make good on its commitments over time is a serious question.

MD: There is no question at all. It will continue to inflate at 4%. That’s how it is funded. That’s how it will always be funded. Institute a “proper” MOE process and that funding becomes impossible. This is because a proper process “guarantees” zero inflation. Governments everywhere would have to resort to taxes for their funding and existence … and that means the banks would no longer get “tribute” (i.e. interest) from them. The governments and banks as we know them would cease to exist … and that would be a good thing.

It would be silly not to prepare for a collapse in confidence, and, by extension, a collapse in the dollar. And nobody should wait. Currency crises through history catch most people by surprise, then it is too late to prepare.

MD: No preparation is feasible. Look at Weimar Germany, Zimbabwe, and now Venezuela for what happens … whether you prepare or not. It would be better to institute a proper and competitive MOE process and let it be the governments’ and banks’ problem, and not the traders’ problem.

Governments are like the Ernest Hemingway character:

“How did you go bankrupt?”

“Two ways. Gradually, then suddenly.”

History is full of nations and currencies rolling slowly downhill for a while, then plummeting over the cliff.

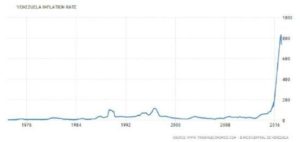

You can show naysayers a picture of the recent hyperinflation in Venezuela:

MD: And it looks real dramatic. It’s like plotting an explosion after a pile of rags has been smoldering from spontaneous combustion for a long time.

Venezuelans who entered 2016 with all of their savings in bolivars probably didn’t know it, but they were in serious trouble. Within weeks they would be searching for scarce food with nothing to exchange but devalued banknotes – slips of paper which merchants suddenly loathed.

The above chart is based on “official” data from the Venezuelan central bank. The reality is even worse.

MD: Read “When Money Dies” by Adam Ferguson. Ponzi schemes have existed forever … even before Ponzi. You don’t have to tolerate them. For darn sure you don’t have to “constitutionalize” them as we have done in the USA. And you won’t improve things at all by strangling traders with the nonsense that precious metals are money.

Grocers can’t keep enough food on the shelves because suppliers don’t want bolivars. Instead, much of the food is bought and sold in black and grey markets where people offer something more compelling in exchange.

Once lost, it is extraordinarily hard to restore confidence.

MD: Read the history. Weimar Germany was well on its way to forgetting about how it had been screwed by its elite within a year of the collapse. And it started all over again. Stupidity is pretty hard to eradicate. Replacing stupid with stupid (in this case declaring precious metal to be money by edict) just moves the problem around.

The Venezuelan government, and their bolivar, are struggling to maintain any sort of legitimacy. Total collapse is all but assured.

Granted, the USA is not Venezuela. Our dollar is the world’s reserve currency and the U.S. is much larger and wealthier than that South American nation. But much of the difference boils down to scale and timing. Venezuela is simply ahead of the U.S. on the same road to national bankruptcy.

MD: The USA “is” Venezuela. The USA covertly caused this collapse of Venezuela. It was precipitated by Venezuela taking over the oil companies. The ultimate result was predictable. What they should have done is just charged them higher rates for their leases.

Absent a course correction, there is little reason to think we won’t arrive at the same destination – hyperinflation and disorder.

It is possible America can make reforms before it is too late. But even those who are optimistic about President Trump enacting change for the better, must admit it is very unlikely that he will ever get Congress to cooperate. And it is that august body which is responsible for spending and debt.

MD: The proper reform is found in instituting a “proper” MOE process to compete with the government process (i.e. dollar) we now use. It will drive the dollar out of existence. The government isn’t going to take the removal of their cash cow lightly. The solution is in education. The people need to be taught about a proper MOE process and its attributes: Zero inflation; zero interest to responsible traders; unrestrained media supply; removal of all monetary controls (and manipulation). The real problem is getting this knowledge into general circulation. This will neuter government and bank efforts to make it illegal. Nonsense from articles like this one is not helpful.

Federal debt and entitlement obligations have kept growing, regardless of which party is in control.

If the U.S. returns to honest money and limited government BEFORE a crisis, it may be the first nation in history to do so. Anybody who doesn’t like those odds would be wise to hold some gold and silver for a handful of good reasons. Having something to barter with is certainly one of them.

MD: “Returns to honest money”? When did it ever have anything different than the money we have now. Answer: Never. It’s just time to institute a “proper” MOE process. It has nothing to do with honesty. It has to do with transparency and plain old common sense.

Clint Siegner is a Director at Money Metals Exchange, the national precious metals company named 2015 “Dealer of the Year” in the United States by an independent global ratings group. A graduate of Linfield College in Oregon, Siegner puts his experience in business management along with his passion for personal liberty, limited government, and honest money into the development of Money Metals’ brand and reach. This includes writing extensively on the bullion markets and their intersection with policy and world affairs.

MD: This article is so typical of what we see coming out of ZeroHedge.com. These people actually believe what they write. As usual, we’ll dissect the article in place and expose the delusions. We’ve done it repeatedly before. The trouble is, they either will never get it…or the are an active part of the scam.

It’s no secret that China and Russia have been stashing away as much gold as possible for many years.

MD: And if they had a clue they wouldn’t be doing that. At the point where gold can have meaning in economics, the game is already over. There is only enough gold on the planet for each person to have less than 2 ounces…less than $4,000. If gold were actually the media of exchange, it would have to trade for a few orders of magnitude greater than that. And if it did, people would be digging up their own back yards looking for the stuff. It’s beyond stupid. Miners who actually know how to find and refine gold would become enormously wealthy, but could never create enough for the rest of us to use it in trade…i.e. as money.

China is the world’s largest producer and buyer of gold. Russia is number two. Most of that gold finds its way into the Russian and Chinese governments’ treasuries.

MD: Where it does absolutely nothing for the benefit of anyone.

Russia has over 2,300 tonnes—or nearly 74 million troy ounces—of gold, one of the largest stashes in the world. Nobody knows the exact amount of gold China has, but most observers believe it is even larger than Russia’s stash.

MD: Ok. Take that number. 74,000,000 ounces. Divide that by the 7 billion people on the planet. That comes to about 0.01 ounces per person on the planet. Times $4,000 per ounce you have $40. That’s 4 trips to McDonalds. Now what?

Russia and China’s gold gives them access to an apolitical neutral form of money with no counterparty risk.

MD: Counterparty risk? What does that have to do with anything. Money is an “in-process promise to complete a trade over time and space.” It is always, and only, created by traders like you and me. And it is always properly destroyed when we deliver as promised. In the mean time it circulates as the most common object of every simple barter exchange. It’s a record keeping problem…and a discipline problem if the trader fails to deliver as promised.

Remember, gold has been mankind’s most enduring form of money for over 2,500 years because of unique characteristics that make it suitable to store and exchange value.

MD: This stupid argument won’t even play in Peoria… let alone throughout the world.

Gold is durable, divisible, consistent, convenient, scarce, and most importantly, the “hardest” of all physical commodities.

MD: And here we have an open admission of ignorance about money. Durable isn’t an issue. An open record keeping system (e.g. ledger) is durable. Divisible? You can divide a number to any number of pieces you choose. If you buy a car by creating $70,000 in new money, that money can circulate as any denomination the marketplace requires. In the USA the smallest denomination is one cent…and most people won’t bend over to pick one up. Consistent? What does that mean? A promise is a promise. Delivery is delivery. What’s to be inconsistent? Convenient? What in the world is more convenient than a record keeping system? Create checks, currency, coins, … they’re just convenient place holders for what is recorded in the ledger. Scarce? This is the one that gets me most. The media of exchange should never be scarce. Quite the contrary, it should be in perpetual free supply. It should resist trade not at all. Hardest? As in harder than a Hershey bar? How ridiculous! And the one they left out…which is historically the biggest problem with any substitute for “real” money…it must be non-counterfeitable! And who is the biggest counterfeiter in “all” cases? Government!

In other words, gold is the one physical commodity that is the “hardest to produce” (relative to existing stockpiles) and, therefore, the most resistant to inflation. That’s what gives gold its superior monetary properties.

MD: Another open admission to stupidity. The money relation is: INFLATION = DEFAULT – INTEREST. Counterfeiting, the biggest cause of default not mitigated by interest collection, is the biggest source of inflation. It’s a very small fraction of traders who don’t deliver as promised. And when that happens, a “real money process” makes an immediate and equal interest collection of like amount. This guarantees that inflation will be perpetually zero.

Russia and China can use their gold to engage in international trade and perhaps back the currencies.

MD: Only as long as ignorance regarding real money prevails.

That’s why gold represents a genuine monetary alternative to the US dollar, and Russia and China have a lot of it.

MD: And of course there is no shortage of “stupid” people who think that matters. Real traders will “create” a “real money process” every time if not conflicted by the money-changers and the governments they institute. I’m now going to let him spew on as long he purveys the same ridiculous fiction. If he comes up with some new nonsense I’ll break back in.

Today it’s clear why China and Russia have had an insatiable demand for gold.

They’ve been waiting for the right moment to pull the rug from beneath the US dollar. And now is that moment…

This is a big problem for the US government, which reaps an unfathomable amount of power because the US dollar is the world’s premier reserve currency. It allows the US to print fake money out of thin air and export it to the rest of the world for real goods and services—a privileged racket no other country has.

Russia and China’s gold could form the foundation of a new monetary system outside of the control of the US. Such moves would be the final nail in the coffin of dollar dominance.

Five recent developments are a giant flashing red sign that something big could be imminent.

Warning Sign #1: Russia Sanctions Prove Dollar Reserves “Aren’t Really Money”

In the wake of Russia’s invasion of Ukraine, the US government has launched its most aggressive sanctions campaign ever.

Exceeding even Iran and North Korea, Russia is now the most sanctioned nation in the world.

As part of this, the US government seized the US dollar reserves of the Russian central bank—the accumulated savings of the nation.

MD: Oh I would so like to have Putin’s ear here. The best thing he could do is institute a “real money process” and use his gold to allay his doubters…he’d never have to touch any of it. In fact, I would like to see Elon Musk do it, rather than buy Twitter (that will bury him in criminal lawsuits should he succeed there).

It was a stunning illustration of the dollar’s political risk. The US government can seize another sovereign country’s dollar reserves at the flip of a switch.

MD: …until its counterfeiting is so obvious and egregious it deals itself out of the game all together.

The Wall Street Journal, in an article titled “If Russian Currency Reserves Aren’t Really Money, the World Is in for a Shock,” noted:

“Sanctions have shown that currency reserves accumulated by central banks can be taken away. With China taking note, this may reshape geopolitics, economic management and even the international role of the U.S. dollar.”

MD: Is anyone getting the dozen or so calls a day that I’m getting…from so-called investors who want to trade dollars for my real property? Why do that unless you know the dollars you hold are about to be worthless.

Russian President Putin said the US had defaulted on its obligations and that the dollar is no longer a reliable currency.

The incident has eroded trust in the US dollar as the global reserve currency and catalyzed significant countries to use alternatives in trade and their reserves.

China, India, Iran, and Turkey, among other countries, announced, or already are, doing business with Russia in their local currencies instead of the US dollar. These countries represent a market of over three billion people that no longer need to use the US dollar to trade with one another.

The US government has incentivized almost half of mankind to find alternatives to the dollar by attempting to isolate Russia.

MD: I vote for a competitive HUL (Hour of Unskilled Labor) based “real money process”. The HUL is valued today (i.e. trades for the same size hole in the ground) as it has for all time…recorded or otherwise.

Warning Sign #2: Rubles, Gold, and Bitcoin for Gas, Oil, and Other Commodities

Russia is the world’s largest exporter of natural gas, lumber, wheat, fertilizer, and palladium (a crucial component in cars).

It is the second-largest exporter of oil and aluminum and the third-largest exporter of nickel and coal.

Russia is a major producer and processor of uranium for nuclear power plants. Enriched uranium from Russia and its allies provides electricity to 20% of the homes in the US.

Aside from China, Russia produces more gold than any other country, accounting for more than 10% of global production.

These are just a handful of examples. There are many strategic commodities that Russia dominates.

In short, Russia is not just an oil and gas powerhouse but a commodity superpower.

After the US government seized Russia’s US dollar reserves, Moscow has little use for the US dollar. Moscow does not want to exchange its scarce and valuable commodities for politicized money that its rivals can take away on a whim. Would the US government ever tolerate a situation where the US Treasury held its reserves in rubles in Russia?

The head of the Russian Parliament recently called the US dollar a “candy wrapper” but not the candy itself. In other words, the dollar has the outward appearance of money but is not real money.

That’s why Russia is no longer accepting US dollars (or euros) in exchange for its energy. They are of no use to Russia. So instead, Moscow is demanding payment in rubles.

MD: Bingo. Game over for the Earth’s, and History’s, most egregious counterfeiter.

That’s an urgent problem for Europe, which cannot survive without Russian commodities. The Europeans have no alternative to Russian energy and have no choice but to comply.

European buyers must now first buy rubles with their euros and use them to pay for Russian gas, oil, and other exports.

This is a big reason why the ruble has recovered all of the value it lost in the initial days of the Ukraine invasion and then made further gains.

In addition to rubles, the top Russian energy official said Moscow would also accept gold or Bitcoin in return for its commodities.

“If they want to buy, let them pay either in hard currency—and this is gold for us… you can also trade Bitcoins.”

Here’s the bottom line. US dollars are no longer needed (or wanted) to buy Russian commodities.

Warning Sign #3: The Petrodollar System Flirts With Collapse

MD: I’m really skimming now. This guy is so far off the tracks there’s no hope of bringing him back. I think I’ll quit here.

Oil is by far the largest and most strategic commodity market.

For the last 50 years, virtually anyone who wanted to import oil needed US dollars to pay for it.

That’s because, in the early ’70s, the US made an agreement to protect Saudi Arabia in exchange for ensuring, among other things, all OPEC producers only accept US dollars for their oil.

Every country needs oil. And if foreign countries need US dollars to buy oil, they have a compelling reason to hold large dollar reserves.

This creates a huge artificial market for US dollars and forces foreigners to soak up many of the new currency units the Fed creates. Naturally, this gives a tremendous boost to the value of the dollar.

The system has helped create a deeper, more liquid market for the dollar and US Treasuries. It also allows the US government to keep interest rates artificially low, thereby financing enormous deficits it otherwise would be unable to.

In short, the petrodollar system has been the bedrock of the US financial system for the past 50 years.

But that’s all about to change… and soon.

After it invaded Ukraine, the US government kicked Russia out of the dollar system and seized hundreds of billions in dollar reserves of the Russian central bank.

Washington has threatened to do the same to China for years. These threats helped ensure that China cracked down on North Korea, didn’t invade Taiwan, and did other things the US wanted.

These threats against China may be a bluff, but if the US government carried them out—as it recently did against Russia—it would be like dropping a financial nuclear bomb on Beijing. Without access to dollars, China would struggle to import oil and engage in international trade. As a result, its economy would come to a grinding halt, an intolerable threat to the Chinese government.

China would rather not depend on an adversary like this. This is one of the main reasons it created an alternative to the petrodollar system.

After years of preparation, the Shanghai International Energy Exchange (INE) launched a crude oil futures contract denominated in Chinese yuan in 2017. Since then, any oil producer can sell its oil for something besides US dollars… in this case, the Chinese yuan.

There’s one big issue, though. Most oil producers don’t want to accumulate a large yuan reserve, and China knows this.

That’s why China has explicitly linked the crude futures contract with the ability to convert yuan into physical gold—without touching China’s official reserves—through gold exchanges in Shanghai (the world’s largest physical gold market) and Hong Kong.

PetroChina and Sinopec, two Chinese oil companies, provide liquidity to the yuan crude futures by being big buyers. So, if any oil producer wants to sell their oil in yuan (and gold indirectly), there will always be a bid.

After years of growth and working out the kinks, the INE yuan oil future contract is now ready for prime time.

And now that the US has banned Russia from the dollar system, there is an urgent need for a credible system capable of handling hundreds of billions worth of oil sales outside of the US dollar and financial system.

The Shanghai International Energy Exchange is that system.

Back to Saudi Arabia…

For nearly 50 years, the Saudis had always insisted anyone wanting their oil would need to pay with US dollars, upholding their end of the petrodollar system.

But that could all change soon…

Remember, China is already the world’s largest oil importer. Moreover, the amount of oil it imports continues to grow as it fuels an economy of over 1.4 billion people (more than 4x larger than the US).

China is Saudi Arabia’s top customer. Beijing buys over 25% of Saudi oil exports and wants to buy more.

The Chinese would rather not have to use the US dollar, the currency of their adversary, to buy an essential commodity.

In this context, The Wall Street Journal recently reported that the Chinese and the Saudis had entered into serious discussions to accept yuan as payment for Saudi oil exports instead of dollars.

The WSJ article claims the Saudis are angry at the US for not supporting it enough in its war against Yemen. They were further dismayed by the US withdrawal from Afghanistan and the nuclear negotiations with Iran.

In short, the Saudis don’t think the US is holding up its end of the deal. So they don’t feel like they need to hold up their part.

Even the WSJ admits such a move would be disastrous for the US dollar.

“The Saudi move could chip away at the supremacy of the US dollar in the international financial system, which Washington has relied on for decades to print Treasury bills it uses to finance its budget deficit.”

Here’s the bottom line.

Saudi Arabia—the linchpin of the petrodollar system—is flirting in the open with China about selling its oil in yuan. One way or another—and probably soon—the Chinese will find a way to compel the Saudis to accept the yuan.

The sheer size of the Chinese market makes it impossible for Saudi Arabia—and other oil exporters—to ignore China’s demands to pay in yuan indefinitely. Moreover, using the INE to exchange oil for gold further sweetens the deal for oil exporters.

Sometime soon, there will be a lot of extra dollars floating around suddenly looking for a home now that they are not needed to purchase oil.

It signals an imminent and enormous change for anyone holding US dollars. It would be incredibly foolish to ignore this giant red warning sign.

Warning Sign #4: Out of Control Money Printing and Record Price Increases

In March of 2020, the chair of the Federal Reserve, Jerome Powell, exercised unfathomable power…

At the time, it was the height of the stock market crash amid the COVID hysteria. People were panicking as they watched the market plummet, and they turned to the Fed to do something.

In a matter of days, the Fed created more dollars out of thin air than it had for the US’s nearly 250-year existence. It was an unprecedented amount of money printing that amounted to more than $4 trillion and nearly doubled the US money supply in less than a year.

One trillion dollars is almost an unfathomable amount of money. The human mind has trouble wrapping itself around such figures. Let me try to put it into perspective.

One million seconds ago was about 11 days ago.

One billion seconds ago was 1988.

One trillion seconds ago was 30,000 BC.

For further perspective, the daily economic output of all 331 million people in the US is about $58 billion.

At the push of a button, the Fed was creating more dollars out of thin air than the economic output of the entire country.

The Fed’s actions during the Covid hysteria—which are ongoing—amounted to the biggest monetary explosion that has ever occurred in the US.

When the Fed initiated this program, it assured the American people its actions wouldn’t cause severe price increases. But unfortunately, it didn’t take long to prove that absurd assertion false.

As soon as rising prices became apparent, the mainstream media and Fed claimed that the inflation was only “transitory” and that there was nothing to be worried about.

Of course, they were dead wrong, and they knew it—they were gaslighting.

The truth is that inflation is out of control, and nothing can stop it.

Even according to the government’s own crooked CPI statistics, which understates reality, inflation is rising. That means the actual situation is much worse.

Recently the CPI hit a 40-year high and shows little sign of slowing down.

I wouldn’t be surprised to see the CPI exceed its previous highs in the early 1980s as the situation gets out of control.

After all, the money printing going on right now is orders of magnitude greater than it was then.

Warning Sign #5: Fed Chair Admits Dollar Supremacy Is Dead

“It’s possible to have more than one reserve currency.”

These are the recent words of Jerome Powell, the Chairman of the Federal Reserve.

It’s a stunning admission from the one person who has the most control over the US dollar, the current world reserve currency.

It would be as ridiculous as Mike Tyson saying that it’s possible to have more than one heavyweight champion.

In other words, the jig is up.

Not even the Chairman of the Federal Reserve can go along with the farce of maintaining the dollar’s supremacy anymore… and neither should you.

Conclusion

It’s clear the US dollar’s days of unchallenged dominance are quickly ending—something even the Fed Chairman openly admits.

To recap, here are the five imminent, flashing red warning signs the end of dollar hegemony is near.

Warning Sign #1: Russia Sanctions Prove Dollar Reserves “Aren’t Really Money”

Warning Sign #2: Rubles, Gold, and Bitcoin for Gas, Oil, and Other Commodities

Warning Sign #3: The Petrodollar System Flirts With Collapse

Warning Sign #4: Out of Control Money Printing and Record Price Increases

Warning Sign #5: Fed Chair Admits Dollar Supremacy Is Dead

We are likely on the cusp of a historic shift… and what’s coming next could change everything.

* * *

The economic trajectory is troubling. Unfortunately, there’s little any individual can practically do to change the course of these trends in motion. The best you can and should do is to stay informed so that you can protect yourself in the best way possible, and even profit from the situation. That’s precisely why bestselling author Doug Casey and his colleagues just released an urgent new PDF report that explains what could come next and what you can do about it. Click here to download it now.511

David Lawant this is my bio More posts by David Lawant.

MD: This blog named MoneyDelusion.com (note singular, not plural like this one) I tripped over. It was created in 2020. MoneyDelusions.com (note plural…was created three years earlier in 2017). This David Lawant is likely a Mises Monk. He’s posted three articles to his blog…one each day for three days…and then nothing. I wonder what he thinks he’s up to. Let’s see if he knows anything about money. If he does he’ll be the first Mises Monk I’ve found who does…and wouldn’t that be exciting!

A Medium of exchange (MoE) is an economic good that is used in exchange for other goods. Money is nothing more than a special case of media of exchange that happens to be universally accepted through a process that has already been well described elsewhere. Under this definition Bitcoin is not money because it’s not commonly accepted (yet), but it certainly is a MoE. For this text you can read these two concepts as synonyms, as everything here about money can be generalized to media of exchange without any loss in meaning.

MD: Right off the bat it looks like he doesn’t get it. A “medium” is the environment (control) within which “media” exists. It’s a minor point…unless his confusion goes deeper. Nope: Second sentence his thinks “money” is a special case of “media”. This is wrong. Money “is” the media. Different “cases” would be like ledger entries, demand deposits, coins, currency, etc. And what is this “universally accepted process described elsewhere”? Now he swerves into correctness…Bitcoin “is” not money…but it looks like it’s “acceptance” that is not mature enough…and thus will eventually be money. He’s wrong. It’s not created correctly. That’s what keeps it from ever being money. That’s what makes it just being stuff of simple barter exchange like gold and silver. And read that last sentence again. He is “money deluded”…that’s for sure.

Media of exchange are not a payment system, as Pierre Rochard correctly and insistently emphasizes. Although a payment system might be a nice-to-have feature to transfer a MoE form one hand to another, it is important to understand that these are completely orthogonal concepts. The channel through which a good is exchanged is not important for the economic analysis of a MoE. What matters is that the good is primarily used to be exchanged for other goods. Ludwig von Mises traced this confusion to a juridical view of money:

…the principal, although not exclusive, motive of the law for concerning itself with money is the problem of payment. When it seeks to answer the question ‘What is money?’ it is in order to determine how monetary liabilities can be discharged. For the jurist, money is a medium of payment. The economist, to whom the problem of money presents a different aspect, may not adopt this point of view if he does not wish at the very outset to prejudice his prospects of contributing to the advancement of economic theory.

MD: See…I told you he was a Mises Monk…and his brain is thoroughly contaminated. We here know that money is “an in-process promise to complete a trade over time and space.” It is always, and only, created by traders like you and me. It may never circulate as an object of simple barter exchange…but virtually always does. And when it does, it trades like any other object that two traders are willing to exchange. But its process is what makes it special. Real money has zero intrinsic value. But when properly protected from counterfeiting, it is the most efficient and most trusted of any object of simple barter exchange. This is because its value never changes over time and space. This is because there is no interest load associated with using it. And it is because the “process (e.g. medium) guarantees this to be so. It cannot operate any other way.

Some Bitcoiners question whether it makes sense to stress so much the MoE aspect of money if it is only a stage in the evolutionary process brilliantly depicted by Nick Szabo (collectible, store of value, medium of exchange, and unit of account). The point, as Szabo points out, is that something special happens when an economic good becomes a medium of exchange.

MD: Here you see a very common attribute of the Mises Monks…that is worship of other Mises Monks. They’re truly a mutual admiration society. It is a religion…and misguided like all religions. But the key thing to note here: An economic good does not “become” a medium of exchange (or even properly a “media” of exchange). Money is not an economic good…it is a “promise”. And “real” money is a promise that is guaranteed to be kept. It’s designed into the process. The sidebar explains it in very simple terms.

Categorization of Economic Goods

One of the most basic distinctions in economics is the one between consumption and production goods, usually called by Austrian economists as first-order and higher-order (second-order, third-order, etc…) goods. We can get away for now with the following simplified definition: first-order (consumption) goods satisfy direct human needs and higher-order (production) goods are used to produce lower-order goods.

MD: Money has no interest in what it is being traded for or how it will be used…or why it is being traded. Why should it? Why do they make this complicated? If I trade money for a hammer, do I care if it’s used to pound nails or to blacksmith wrought iron…or just to hang on the wall? If this article tells us why “he” cares we’ll correct him at that instant.

There’s nothing intrinsic about whether a good is first or higher order. For example: I can consume a certain amount of water to satisfy my thirst (i.e., water as a first-order good) or alternatively I can provide this same amount of water to cattle which I will ultimately consume as food (i.e., water as a second-order good and cattle as a first-order good).

First- and higher-order economic goods, albeit ultimately connected to a fundamental theory of value, are different enough to be treated separately in many instances. As Jesus Huerta de Soto puts it: “this classification and terminology were conceived by Carl Menger, whose theory on economic goods of different order is one of the most important logical consequences of his subjectivist conception of economics”.

Peter Paul Rubens’ representation of an altcoiner trying to spin up a monetary system (c. 1614–1616)

MD: More praise for fellow Mises Monks. Look how far we are into this article and he still has said nothing that has to do with money. He’s just tried to act like an intellectual. We know that as “double talk”. And watch out for creation of a new “..ist”…in this instance “subjectivist”. Does the world really need any more “ists”?

We have thus defined that media of exchange are goods that have no real “utility” aside from being exchanged for other goods, which in turn have real “utility” of their own. So how do we classify media of exchange? Are they first-order (consumption) or higher-order (production) economic goods? Is there anything especial about media of exchange that warrants a special analysis of them?

MD: When you realize that it’s the entire trading universe that is the “medium” of exchange, you don’t have to classify anything. In trading, those who prefer to trade for gold know its value. If they trade in silver, they know its value. What is different about “real” money is “its value never changes.” This can’t be said for any other object of simple barter exchange.

MD: The preferred unit for money is the HUL (Hour of Unskilled Labor). For all time in the past it has traded for the same size hole in the ground. And in a “real” money process, it will trade for the same size hole in the future. It is the traders who decide in their personal trades how many HULs is being traded.

MD: And this is a great simplification over the complicated process he alludes to. In his process you have to know the changing value of every good and service …in your mind. But when it comes to “real money” as one of the exchanged objects, you always know its value. When you were in high school (i.e. unskilled labor) you knew exactly what people were willing to pay for it. With the improperly managed dollar, people were willing to pay me $1.50 for a HUL. Today they are willing to pay $8.00. Why? Because the improper “dollar process” has allowed counterfeiting. They have allowed the supply/demand balance to change over time…and it is with supply continually outstripping demand through government counterfeiting (i.e. making promises they never keep)…counterfeiting “inflates” the supply. It’s just that simple.

Media of Exchange Are a Sui Generis Type of Economic Good

The number of economists who don’t have good answers to these questions is astounding. Most simply classify media of exchange as a higher-order good by exclusion. They don’t have direct “utility”, so they cannot be first-order economic goods.

MD: Here we see the pot calling the kettle black. I’m going to just let him spew on here. To put what he writes in context, he thinks gold is money. He thinks money “always” has intrinsic value. Gold thus gets its value by digging dirt and refining it. But dirt in your back yard isn’t going to give you any gold…no matter how much you refine it. And you can argue until you’re blue in the face that you put as much work into your backyard dirt as the gold professional put into his. He got gold…you didn’t. He got something to trade for his HULs…you didn’t. But when you know money is a promise, and you know “real” money comes from a process that “guarantees promises”, you don’t need to screw around with things like gold. I’ll let you read on yourself for a while. These guys make me tired..

Austrian economists think this approach is simplistic and inconsistent. They defend a three-fold categorization of economic goods: first-order (consumption) goods, higher-order (production) goods and media of exchange. This is a key proposition in Ludwig von Mises’ indispensable Theory of Money and Credit. He even criticizes his master Eugen von Böhm-Bawerk and defends the position of Karl Knies, economist of the rival German historical school, in this respect:

Production goods derive their value from that of their products. Not so money; for no increase in the welfare of the members of a society can result from the availability of an additional quantity of money. The laws which govern the value of money are different from those which govern the value of production goods and from those which govern the value of consumption goods.

The peculiarity of media of exchange, and by extent of money, as economic goods is clearly exposed by a simple conundrum. We know intuitively that every economic good can command a price because it has “utility”. If the “utility” of a MoE is to have purchasing power (i.e., a price), how to we get out of this circular reference to understand how money has value? Mises derived his famous regression theorem to solve this apparent circularity by introducing the time element, but this is outside the scope of this text. What matters for us is that media of exchange are unique because their “utility” and purchasing power coincide. As Murray Rothbard puts it:

Without a price, or an objective exchange-value, any other good would be snapped up as a welcome free gift; but money, without a price, would not be used at all, since its entire use consists in its command of other goods on the market. The sole use of money is to be exchanged for goods, and if it had no price and therefore no exchange-value, it could not be exchanged and would no longer be used.

MD: Here is a good time to comment on this thing they call “price”. It’s how much of the stuff you have and are willing to trade for how much of the stuff your trading partner has and is willing to trade. If the “stuff” is real money, you both know exactly what is being traded…one hour of unskilled labor…and it’s guaranteed. You can convert that to dollars, marks, franks, ounces of gold, or pork bellies. It’s up to you to decide on that conversion. But one thing you don’t have to do with “real” money. You don’t have to decide what a HUL is worth. You always know, because at one point in your life your were one…an hour of unskilled labor. So if you’re using “real” money, your trade just got less risky by a factor of two (i.e. one of the objects being traded is “guaranteed” not to change over time and space). Let’s let him blab on further for a while..

This special relationship between “utility” and price for media of exchange makes its analysis unique and leads to conclusions that might seem counter-intuitive compared to the analysis of typical commodities. As Mises points out: the real problem of the value of money only begins where it leaves off in the case of commodity-values. Rothbard agrees with Mises on this point: