If The Fed Starts A Digital Currency, It Had Better Guarantee Privacy Tyler Durden’s Photo by Tyler Durden Tuesday, Apr 05, 2022 – 08:00 PM

MD: As always, Money Delusions will use the true definition of “real” money to annotate this article. The article appear in ZeroHedge.com as “If the Fed Starts A Digital Currency, It Had Better Guarantee Privacy”. And the title itself reveals confusion about what money is…and what its characteristics are. This begins by knowing what money is (i.e “an in-process promise to complete a trade over time and space”); how money is created (i.e. transparently in plain view by traders like you and me); how money is destroyed (i.e. also transparently by the trader delivering as promised); what happens if the trader “defaults” (i.e. “interest” of like amount is immediately collected); and how money trades in the interim (i.e. anonymously as any other object of simple-barter-exchange). Let’s get started:

Authored by By Andrew M. Bailey & William J. Luther via RealClearPolicy.com,

President Biden’s latest executive order calls for extensive research on digital assets and may usher in a U.S. central bank digital currency (CBDC), eventually allowing individuals to maintain accounts with the Federal Reserve. Other central banks are already on the job. The People’s Bank of China began piloting a digital renminbi in April 2021. India’s Reserve Bank intends to launch a digital rupee as early as this year.

MD: They immediately exhibit that they don’t know what money is. “Banks” have nothing to do with “real” money at all. It is the most obvious corruption of real money. And “digital” is just one of many forms of money.

Most commonly, money is just an entry in a ledger. In some cases it is in the form of coins and currency…both carefully designed to resist counterfeiting. In some cases it is in the form of a check (i.e. against a demand deposit). And we already have a fairly digital form of money in “debit cards”…a link to your ledger records that you carry in your purse. “Credit cards” are not an example of money. Rather, they are an example of “money creation”.

When you charge something on a credit card, “you” are creating money…a promise to complete a trade over time and space. When you use a “debit card” you are merely submitting proof that you hold some previously created money.

A CBDC may upgrade the physical cash the Federal Reserve already issues – but only if its designers appreciate the value of financial privacy.

Cash is a 7th century technology, with obvious drawbacks today. It pays no interest, is less secure than a bank deposit, and is difficult to insure against loss or theft. It is unwieldy for large transactions, and also requires those transacting to be at the same place at the same time — a big problem in an increasingly digital world.

MD: And before cash we had the tally stick…which claims to be the best implementation of money. And tally sticks were “real” money. They represented a promise to complete a trade over time and space. They worked better than gold. In fact, they could claim any kind of “backing” the trader’s agreed to (e.g. pork bellies). But nobody “traded” tally sticks. Thus, in that respect they weren’t money at all. They really were close to “crypto” in that respect…but much cheaper to create. You could create a tally stick with a twig and a knife. Today’s crypto requires insane amounts of electricity waste to create. They call it “proof of work”…which of course is nonsense.

Nonetheless, cash remains popular. Circulating U.S. currency exceeded $2.2 trillion in January 2022, more than doubling over the last decade. The inflation-adjusted value of circulating notes grew more than 5.5 percent per year over the period. And U.S. consumers used cash in 19 percent of transactions in 2020.

MD: Actually, the money changers are revealing the imminent collapse of cash. They hold lots of cash (counterfeited by government) and are doing everything they can to exchange it for real “property”. I get a dozen calls a day from “so-called investors” who want to “buy” my property. It’s a game of musical chairs. They don’t want to holding it when the “reset” comes as they know it will be instantly worthless. And also note, with “real” money, inflation is perpetually zero. No adjusted valuation is ever necessary.

Why is cash so popular, despite its drawbacks? Cash is easy to use. There are no bank or merchant terminal fees associated with cash. And, most importantly, it offers more financial privacy than the available alternatives.

MD: In actuality, cash is “not” easy to use. You almost never see it being used…even in restaurants and bars. I use it in bars just to keep score. I take a certain amount of cash, which when I’ve used it up I know I’m about to have had too much to drink. I spend lots of time explaining to other patrons why I can’t let them buy me a beer.

When you use cash, no one other than the recipient needs to know. Unlike a check or debit card transaction, there’s no bank recording how you spend your money. You can donate to a political or religious cause, buy controversial books or magazines, or secure medicine or medical treatment without much concern that governments, corporations, or snoopy neighbors will ever find out.

MD: With a “real” money implementation, there is no need for banks to be involved. All that is necessary is a “block chain” like implementation that resists the “three general problem” and counterfeiting. And when properly implemented, the “block chain” implementation is cost free. It has no use for “proof of work”. It “knows” it’s keeping track of performance on promises.

Privacy means you get to decide whether to disclose the intimate details of your life. Some will happily share. That is their choice. But others will prefer to keep those details private.

MD: But keep in mind, while “real” money used in trade is “always anonymous”, it’s creation is always “open and transparent”. Awareness of this distinction is crucial.

In a digital world, personal information can spread far and wide. And it can be used to exclude or exploit people on the margins. The choice about what information to share is important. For some, flourishing depends on carefully choosing how much others know about their politics, religion, relationships, or medical conditions.

Financial privacy matters just as much as privacy in other areas. What we do reveals much more about who we are than what we say. And what we do often requires spending money. In many cases, meaningful privacy requires financial privacy.

MD: Again, keep in mind that money is only concerned with the problem of “counterfeiting”. It cares not at all who is using it and for what. But people using it must know and expect it is genuine…i.e. not counterfeited. And of course we all know the principal counterfeiters of money are governments. For a “real” money process to exist, it’s operation must be transparent and impervious to any attempts to control or to counterfeit it. It is simply about record keeping.

Privacy also operationalizes the presumption of innocence and promotes due process. You are not obliged to testify against yourself. If law enforcement believes you have done something unlawful, they must convince a judge to issue a warrant before rifling through your things. Likewise, financial privacy prevents authorities from monitoring your transactions without authorization.

MD: Law doesn’t apply to a “real” money process. But open communication and mitigation is crucial. Again, it’s about making counterfeiting impossible. And when detected it must reveal who did the counterfeiting; see that the counterfeiting doesn’t happen again; and treat the counterfeiting for what it is… a “default”. And thus it immediately mitigates it with “interest” collection of like amount. This must be totally transparent…so the marketplace can ostracize the perps. Who pays the interest? Other irresponsible traders.

The recent executive order, to the administration’s credit, notes that a CBDC should “maintain privacy; and shield against arbitrary or unlawful surveillance, which can contribute to human rights abuses.” But a reasonable person might worry that the government is paying lip service to privacy concerns.

MD: A principle “axiom” must be observed at all times. If you are considering a government solution to any problem, you are still looking for a solution. Government is “never” the solution to any problem. It is just a magnifier of the problem.

A recent paper from the Fed, offered as “the first step in a public discussion” about CBDCs, suggests the central bank has no interest in guaranteeing privacy at the design stage. Instead, it maintains that a “CBDC would need to strike an appropriate balance […] between safeguarding the privacy rights of consumers and affording the transparency necessary to deter criminal activity.” The Fed then solicits comments on how a CBDC might “provide privacy to consumers without providing complete anonymity,” which it seems to equate with “facilitating illicit financial activity.” A U.S. CBDC, in other words, will likely offer much less privacy than cash.

MD: No central entity (especially a central bank) is ever involved in a “real” money process. Rather, it is the “process” that is the entity. As such, the process is universally used and totally transparent to all traders at all times.

We do not deny that financial privacy benefits criminals and tax cheats. Such claims tend to be exaggerated, though. In reality, it is a small price to pay for civil liberty. That due process applies to everyone — criminals included — is no reason to scrap the Fourth or Fifth Amendments.

MD: Taxes implies government…so it is a non-starter. If government participation was ever a valid option, it would be the “only” viable option. You would pay taxes (and only taxes) for everything. Your gasoline, your groceries, your clothing…all would be free. You would just pay tax and it would be covered out of that. Some people call this communism. Some call it insurance. It’s all nonsense.

Policymakers may be tempted to compromise on financial privacy when implementing a CBDC. Instead, they should attempt to replicate the privacy afforded by cash. Like non-alcoholic beer, the Fed’s “digital form of paper money” would superficially resemble the real McCoy while lacking its defining feature.

MD: Policy is the the marker here. No process is every properly governed by policy. The closest we should ever come to adopting policy is the “golden rule”. Policy is different from process. Money is a “process”. It cares nothing about policies like full employment and setting inflation at 2% (while continuously failing by a factor of 2).

MD: Note: There are charts

embedded in this article

which link back to the original. In time they will likely get

broken.

MD: A proper MOE (Medium of Exchange or Money) Process

treats all “traders” equally. But this instance does bring on to

the stage an important case. What limits should be placed on the

size of “promises” it will embrace…and why?

The case is fairly simple for individuals. It easily embraces

the case for viable shelter (buying a house). It easily embraces the

case for viable transportation (buying a car). It easily embraces

the case for unanticipated medical needs (supplementing insurance).

But how does it deal with the case for highly leveraged promises?

I will answer this question as I read the article and

intersperse my comments. Hopefully it will address these issues. The

most important issues are regarding “leverage” and detection of

“rollovers”.

The only way to get really wealthy in any society is through

unusual leverage.

Banks grant themselves 10x the leverage you and I have. As

individuals we have no leverage. We work an hour…we make some

number of HULS (note: HULs…Hours of Unskilled Labor… are the

ideal MOE measure). We must be really really good at what we do

(e.g. neurosurgery) to be worth 10x what we were in high school).

The mom and pop shop has almost no leverage. They “are”

the business. But as they grow they hire help. And that is the

beginning of their leverage growth. They take a piece of their

workers’ labor as if they performed it themselves. As they grow they

retain earnings but may also take on debt (i.e. they make money

creating promises) or they take on partners (sell shares in their

company). The money creating case is problematic. You can’t just say

I want to create a car company and create $100B (or 10B HULS).

Then we have the financial wizards. They claim to be able to

deploy surplus HULs better those who earn those HULs. And they take

a piece of the action if they succeed. They don’t suffer if they

fail; their clients do the suffering. They use options, derivatives,

high speed trading, and myriad other tricks to multiply the natural

leverage this game brings them.

Selling shares is not problematic. Each shareholder has to

decide how he’s going to come up with the money to pay for his

share. And the business itself decides how it will reward his

participation. There are many games being played in this space to

help mom and pop keep control as they grow. For example, they can

give themselves options to buy shares as payment. They can mix debt

and equity instruments as warrants. The options have proven to be

inexhaustible…their consequences unknowable and unsupportable.

Such tactics are of no concern to the MOE process. Its only

interest is in the “reasonableness” of the money creation and

tracking its return and destruction. That means assessing the

trader’s propensity to default and monitoring his performance in

real time. And we know how to address such issues. We call them

actuaries. They have great experience in the mutual casualty

insurance business.

So now lets see how we address this very unusual but real

instance of a threat to the MOE process. More importantly, we see

how the MOE process places the responsibility exactly where it

belongs…with the promise maker and with the process behavior. This

characteristic gives some assurance of self discipline.

If the trader screws up, the trader must back his failed

promise or he must pay the consequences (i.e. be banned from

creating money…as we know all governments will be banned if they

don’t change their behavior).

If the process screws up (i.e. supports an irresponsible

trader), it must penalize oncoming traders (responsible or

irresponsible) immediately. They pay INTEREST (which is returned if

they prove to be responsible).

Now to the article. My interspersed comments appear formatted

as this pretext is formatted. And please bear with me…I’m thinking

through this as I write and it’s worth at least what you’re paying

for it.

==================

Well, with everyone and everything else getting a bailout, may as

well go all the way.

MD: What a remarkable opening. Is that like “if rape

is inevitable, relax and enjoy it”?

Two months after we

reported that the state of California is trying to turn

centuries of finance on its head by allowing businesses to walk away

from commercial leases – in other words to make commercial debt

non-recourse – a move the California Business Properties Association

said “could cause a financial collapse”, attempts to bail

out commercial lenders have reached the Federal level, with the WSJ

reporting that lawmakers have introduced a bill to provide

cash to struggling hotels and shopping centers that weren’t able

to pause mortgage payments after the coronavirus shut down the U.S.

Economy.

MD: Well, the concept of “throwing good money after bad” is well known. And this likely falls into that category. Shopping malls have become a thing of the past. They had their 50years in the sun and have now been made obsolete by a better idea (.e.g. Amazon). The handwriting was on the wall way before the COVID-19 hoax and government lock-down suspended trade. COVID-19 is a neutron bomb attack. It kills people but doesn’t destroy things. For those still alive, a restart should be a simple process. Suspend the delivery on existing money creating promises until the external restrictions have been lifted. Continue to support new money creating promises using regular actuarial principles. Such principles will detect “rollover” attempts and reject them.

I think the obvious solution is to recognize the situation and do an “automatic extension” of promise time terms (the “time” part of the time and space spanning trade) of all affected promises, and move painlessly on down the road. Nobody gets hurt.

The bill would set up a government-backed funding vehicle which

companies could tap to stay current on their mortgages. It is meant

in particular to help those who borrowed in the $550 billion CMBS

market in which mortgages are re-packaged into bonds and sold to

Wall Street. What it really represents, is a bailout of the only

group of borrowers that had so far not found access to the Fed’s

various generous rescue facilities: and that’s where Congress comes

in.

MD: The problem as expressed here does not exist with a

proper MOE process. Money is not “backed” by anything but the

process. So there is no such thing as a CMBS market or

mortgage-backed securities and bonds. If we had a proper MOE

process, such techniques could still exist for those who want the

risk of non-responsible traders. But that is no concern or

responsibility of the money process. And the phrase

“government-backed funding vehicle” is a marker. This is not a

viable proposal with the word “government” in it.

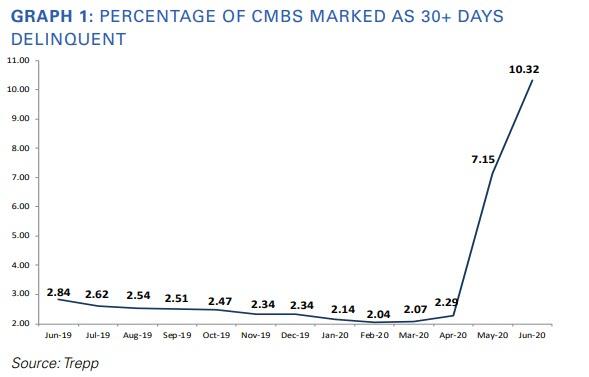

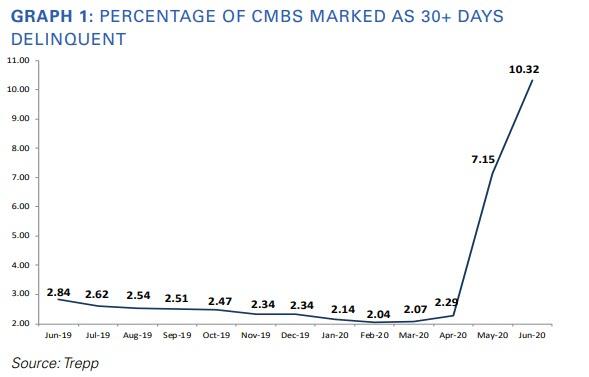

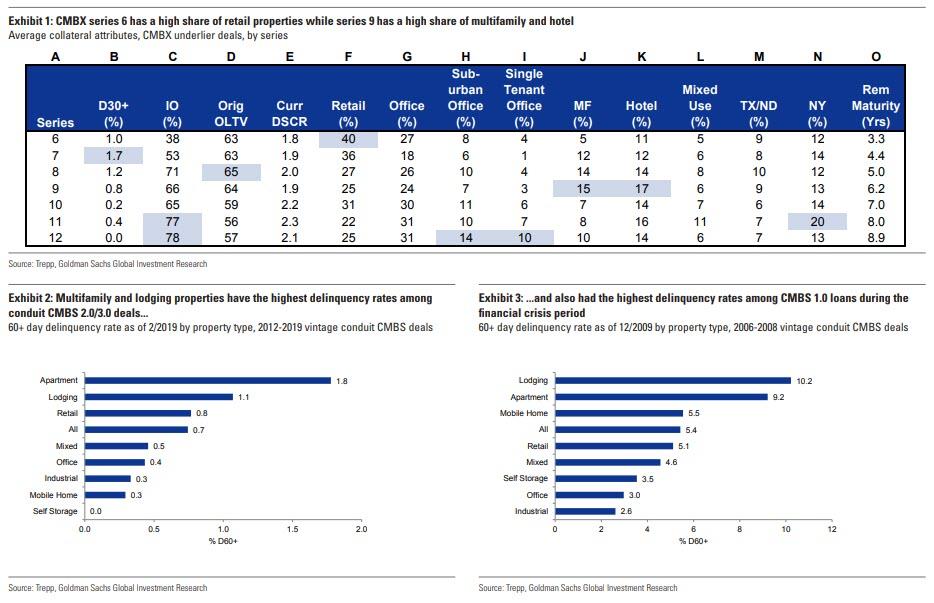

To be sure, the commercial real estate market is imploding, and

as we reported at the start of the month, some 10% of loans in

commercial mortgage-backed securities were 30 or more days

delinquent at the end of June, including nearly a quarter of loans

tied to the hard-hit hotel industry, according to Trepp LLC.

MD: And if those leases were taken on by trader created

money, then an automatic 30 day extension would have already been

applied to their promise. Such extensions could go on indefinitely.

There are no so-called investors involved at all. Mom and pop

created the money (they created money for the full lease as if it

was a purchase…but is paid out to the seller monthly) and this is

one of those unavoidable occurrences that the money process

naturally accommodates. Loan sharks anticipate this too. They take

the property. Moving these leases into the MOE process space stops

the domino effect such instances create.

MD: The above curve illustrates the superiority of the

MOE process solution. In April, the COVID-19 hoax lock down

occurred. Up until then the market was healthy and getting more

healthy. Then wammo!. With the MOE process, the above curve would go

flat…or maybe even continue to go down. And a new curve would

start up. That curve would be the automatic extensions of the time

component of the money creating promises. There is no pain to anyone

anywhere…and everyone is still responsible for their promise.

Note, this concept also applies to floor plans purchased in

anticipation of normal business sales performance…now interrupted

by the lock down. Such provisions are now provided by banks through

lines of credit or compensating balance loans…and they profit

exorbitantly.

“The numbers are getting more dire and the projections are

getting more stern,” said Rep. Van Taylor (R., Texas), who is

sponsoring the bill alongside Rep. Al Lawson (D., Fla.).

MD: In our system “sponsoring a bill” means “bowing

to a lobbyist”. That’s how our corrupt system works. That’s what

gives the wealthy so much leverage over the mom and pops. A proper

MOE process levels the playing field…at no cost or risk to anyone.

Under the proposal, banks would extend money to help these

borrowers and the facility would provide a Treasury Department

guarantee that banks are repaid. The funding would come from

a $454 billion pot set aside for distressed businesses in the

earlier stimulus bill.

MD: You’ve got to love that phrase “banks would extend money”. Folks. The banks don’t have money. They have a 10x leverage privilege. A proper MOE process makes that privilege unnecessary. Let the banks continue to exist if they want to. But the 10x privilege is an anachronism.

Richard Pietrafesa owns three hotels on the East Coast

that were financed with CMBS loans. They have recently had occupancy

of around 50% or less, which doesn’t bring in enough revenue to

make mortgage payments, he said.

MD: And here is a case where we have to ask: where does the money come from? When you buy a house over time you can securely make that money creating promise. You know what you expect to make and purchase a house accordingly. But if the income is interrupted its your problem to find a replacement for it.

But Pietrafesa has no way of replacing his interruption. Such deals are heavily leveraged (OPM…other people’s money). He couldn’t get the MOE process to allow this money creating trade in the first place. He would have to rely on forming a collective to get his hotel deal done. And if the collective fails, well, as individuals in the collective, they have an incentive to keep it from failing or they lose their share. The MOE process may allow their trading promise to Pietrafesa…but would not allow Pietrafesa’s promise to the owner of the hotel he purchased. For example, just like buying a house with time payments, they could actuarially show they could buy a piece of a hotel with time payments…and be responsible if it fails.

He said he is now two months behind on payments for one

of his properties, a Fairfield Inn & Suites in Charleston, S.C.

He has money set aside in a separate reserve, he said, but his

special servicer hasn’t allowed him to access it to make debt

payments.

MD: Here we have the domino effect. He’s paying a “special servicer” to cover this risk. He’s buying insurance. It’s an actuarial problem. And insurance companies are the ultimate leveragor. In insurance CLAIMs = PREMIUMS. The money is made on the investment income. But with a real MOE process which guarantees zero INFLATION, investment income can’t benefit from the leverage INFLATION gives. The insurance business becomes a risk mitigation business with a proper MOE process…as it should be.

“It’s like a debtor’s prison,” Mr. Pietrafesa

said.

MD: An MOE process does not have a provision for penalizing. It only has a provision for naturally ostracizing. Pietrafesa would have to pay INTEREST if he DEFAULTs and tries to create money again. And he has to make up that DEFAULT to become a responsible money creating trader again. It’s the natural negative feedback stabilizing loop of the process.

Those magic words, it would appear, is all one needs to say these

days to get a government and/or Fed-sanctioned bailout. Because in a

world taken over by zombies, failure is no longer an option.

MD: These days are no different than other days. In the

olden days the zombies were taken over by the Rothschilds…through

their J.P.Morgan agency. It was and is a protection racket…just

like the mafia runs. A proper MOE process removes the leverage and

drives them out of business…kind of like legalizing drugs drives

those dealers them out of that business. Ultimately, people need to

be responsible for their own stupidity…but not for the stupidity

of others.

While any struggling commercial borrower that was previously in

good financial standing would be eligible to apply for funds to

cover mortgage payments, the facility is designed specifically for

CMBS borrowers.

MD: Thus, the leverage is in the ability to lobby. Such

advantage needs to be eliminated…in a very natural, not

legislative, manner. A proper MOE process goes far in enabling that.

It gets better, because not only are taxpayers ultimately on the

hook via the various Fed-Treasury JVs that will fund these programs,

but the new money will by default be junior to existing insolvent

debt. As the Journal explains, “many of these borrowers have

provisions in their initial loan documents that forbid them from

taking on more debt without additional approval from their

servicers. The proposed facility would instead structure the

cash infusions as preferred equity, which isn’t subject to the

debt restrictions.“

MD: The taxpayers are not on the hook. Our current

process with no stabilizing negative feedback will just keep

escalating until it blows itself up. Then most people (not in the

inner circle with advance warning) lose; it resets; and starts all

over again…with the insiders picking up the pieces for pennies on

the dollar. We now pay over 3/4ths of what we earn to governments.

Where does communism begin? Where does slavery begin?. It’s not a

good system folks. We’ve been duped. And praising the constitution

and wrapping ourselves in the flag is not going to fix it. It was

broken when it was installed…the anti-federalists got it right but

lost the argument.

Yes, it’s also means that the new capital is JUNIOR

to the debt, which means that if there is another economic downturn,

the taxpayer funds get wiped out first while the pre-existing debt –

the debt which was unreapayble to begin with – will remain on the

books!

MD: When a building collapses, it’s kind of immaterial

whether the lower floors or the upper floors collapse first. When

this calamity happens, the dirt this house of cards stands on is the

only thing of value.

Perhaps sensing the shitstorm that this proposal would create,

the WSJ admits that “the preferred equity would be considered

junior to other debt but must be repaid with interest before the

property owner can pull money out of the business.”

MD: And this is how we get 40,000 new laws every year.

They start with a bad process (i.e. principles diluted by laws) and

are stuck with a huge maintenance problem.

What was left completely unsaid is that the existing impaired

CMBS debt will instantly become money good thanks to the

junior capital infusion from – drumroll – idiot taxpayers who won’t

even understand what is going on.

MD: “will instantly become money”: Let’s examine

this. We know what money is. So somehow he’s saying that some trader

instantly makes a promise spanning time and space here. Who’s the

trader, the taxpayer? Well that’s no different than what we have now

with government doing perpetual rollovers of their trading promises.

That’s not money creation. That’s counterfeiting. We already know

that.

How did this ridiculously audacious proposal come to being? Well,

Taylor led a bipartisan group of more than 100 lawmakers who last

month signed a letter asking the Federal Reserve and Treasury to

come up with a solution for the CMBS issues. Treasury Secretary

Steven Mnuchin and Fed Chairman Jerome Powell have indicated that

this may be an issue best addressed by Congress.

MD: “asking the Federal Reserve and Treasury to come

up with a solution”? They’re the problem. Institute a proper MOE

process and we drive out the problem. That allows us to address

issues in a “proper” context rather than an “opportunist”

context.

In other words, while the Fed will be providing the special

purpose bailout vehicle, it is ultimately a decision for Congress

whether to bail out thousands of insolvent hotels and malls.

MD: The malls have no future. They are the buggy whip

of a previous era. They need to be plowed under and reseeded. But

the hotels are viable. They are just suspended in time. If they’re

collectively owned they are the responsibility of the members of the

collective. They are suspended in time. They are not failing. And

suspension carries no cost in this instance except maintenance.

Remember, with a propper MOE process, money has zero time value.

Failure? That’s something else again. It all get’s back to the

individual traders’ responsibility and recourse. A proper MOE

process should allow small traders to create money to tide

themselves over the temporary situation. It should not support large

highly leveraged traders to do so. It’s an actuarial problem.

And if some in the industry have warned that an attempt to rescue

the CMBS market would disproportionately benefit a handful of large

real-estate owners, rather than small-business owners, it is because

they are precisely right: roughly 80% of CMBS debt is held by a

handful of funds who will be the ultimate beneficiaries of this

unprecedented bailout; funds which have spent a lot of money

lobbying Messrs Taylor and Lawson.

MD: Handful of “funds”. What is a fund but a

collective… where the manager gets the gains and the participants

get the losses. People who buy into a fund roll their own dice. When

the fund is a pension fund, only the pensioner should have control.

With perpetual zero inflation, placing their pension under a rock is

a viable solution.

Of course, none of this will

be revealed and instead the talking points will focus on reaching the

dumbest common denominator. Taylor said the legislation is focused on

– what else – saving jobs. What he didn’t say is that each job that

is saved will end up getting lost just months later, and meanwhile it

will cost millions of dollars “per job” just to make sure

that the billionaires who hold the CMBS debt – such as Tom Barrack

who recently

urged a margin call moratorium in the CMBS market – come out

whole.

MD: Saving jobs “is” the issue. These workers are

suspended in time. It’s their responsibility to provide for

themselves. They can do this by creating money to tide themselves

over (say for a year or two if necessary). A proper MOE process could

actuarially support this money creation.

Say we have the maitre-d of the hotel restaurant. It’s

pragmatic for him to span this interruption and go back to work as if

nothing happened. So he creates a time and space spanning money

creating promise. He creates two years of normal income to be paid

back 1/100th monthly. The payback begins two years hence and proceeds

100 months. When he goes back to work he begins paying back,

essentially cutting his own salary a manageable amount. And while

suspended, he can put up dry-wall and make some pin money.

For the bar-back it’s a little different. He may make a money

creating promise covering 3 months income to be paid back monthly

beginning in three months over a two year span. And he immediately

goes looking for a replacement job…maybe putting up dry-wall. His

job is not his “career”.

“This started with employees in my district calling and saying

‘I lost my job’,” Taylor said, clearly hoping that he is dealing

with absolute idiots.

MD: An idiot institutes processes that have built in

domino effect.

And while it is unclear if this bill will pass – at this point

there is literally money flying out of helicopters and the US deficit

is exploding by hundreds of billions every month so who really gives

a shit if a few more billionaires are bailed out by taxpayers –

should this happen, well readers may want to close out the trade we

called the “The

Next Big Short“, namely CMBX 9, whose outlier exposure to

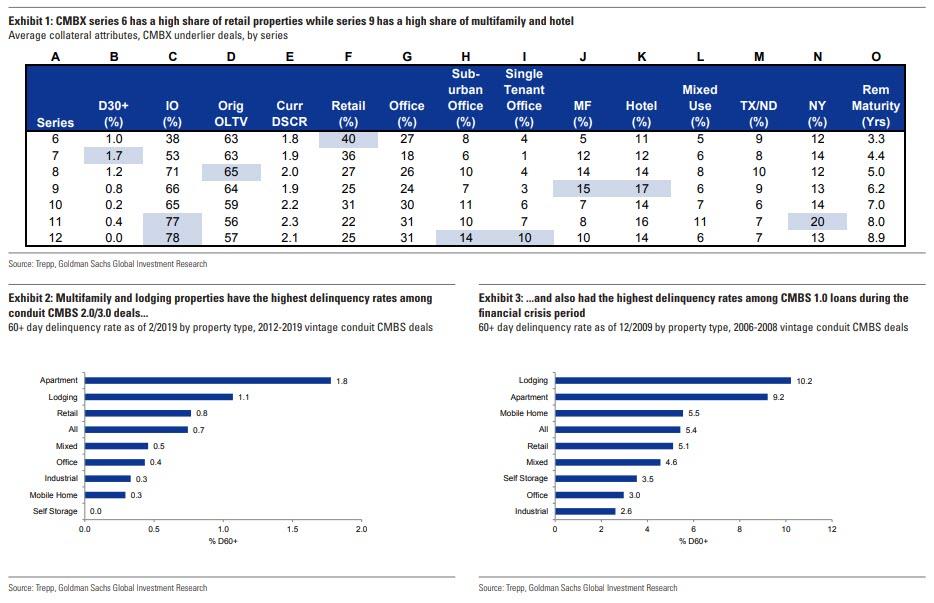

hotels which had emerged as the most impacted sector from the

pandemic.

MD: The money flying out of the helicopters is

counterfeit. It will go directly to producing INFLATION. It will only

create taxes to the extent the money-changers demand their tribute

payments…that’s where “all” taxes go.

With a proper MOE process the domino effect is mitigated; a

natural stabilizing negative feedback mechanism prevails; and a

pragmatic self controlled recovery is instituted. Remember. When you

have a government solution to a problem, you just have the same

problem multiplied and are still looking for a solution.

Alternatively, those who wish to piggyback on this latest

egregious abuse of taxpayer funds, this crucifxion of capitalism and

latest glorification of moral hazard, and make some cash in the

process should do the opposite of the “Next Big Short”

and buy up the BBB- (or any other deeply impaired) tranche of the

CMBX Series 9, which will quickly soar to par if this bailout is ever

voted through.

MD: And the real character of so-called “investors”

is revealed and amplified. Without a proper MOE process, money is the

chips in an opportunist, privileged casino called capitalism.

Traderism is where real money lives.

MD: So here we have another good example where a proper MOE process doesn’t “treat” a problem; rather it anticipates it and prevents its effect.

[MD] The provocative (and ill-informed) title of this article begs some annotation. At Money Delusions, it is obvious and provable to us that not only is money debt, it always has been and it always will be. Money is a promise to complete a trade over time and space … and a promise is obviously a debt.

So let’s see what this moron Shorty Dawkins has to say on the subject.

When the Federal Reserve System was established in 1913, it transferred the power of the US Treasury vis-a-vis the creation of money, into the hands of the Federal Reserve. The Fed creates money out of thin air and loans it to the US Treasury in the form of interest bearing debt instruments. Thus, the money of the US is based on debt. With over $20 trillion in Federal debt, the interest paid on that debt in fiscal year 2018 is estimated to be $310 billion. That’s no small amount!

[MD] What was actually transferred was the propensity to counterfeit. Neither the Treasury nor the Fed create money. Only traders create money. You can’t give a single example where money is created that a trader is not involved and did not initiate it … that is, unless it is created by counterfeiting. And regarding the interest paid: If the process is a “real” process, the interest paid is exactly equal to the defaults experienced. Why don’t we ever see these people quoting defaults experienced?

What if money were not created out of debt? Is that possible? Sure. If the powers of the Federal Reserve were taken back by the US Treasury, it would be possible to spend money into existence, rather than into existence as debt.

[MD] Can he say anything more stupid? “Spend money into existence?” And if not into debt, into “existence” as what? Kind of left something out didn’t you Shorty?

The Federal budget for 2018 is: Total expenditures: $4.094 trillion. The total estimated revenue: $3.654 trillion. This leaves a projected deficit of $440 billion. Since the deficit must, under the current Federal Reserve System, be borrowed from them, at interest. Thus the deficit grows and next year’s interest payment will increase.

[MD] If a “real” money process were in existence, the government creating this debt would only do it once … and then be excluded from the marketplace as a trader. Deadbeat traders are automatically excluded when their interest load (due to their propensity to default) comes to equal the trading promises they seek to have certified.

However, if the US Treasury were to create the money, it could simply spend it into existence to cover the deficit. No interest need be paid! As the previous debt interests of the Federal Reserve came due, they could be paid off by money created by the US Treasury in the same manner. Eventually, the entire debt could be paid off in this manner.

[MD] “No interest need be paid” is true only for responsible traders. Governments are not responsible traders. In fact they never deliver. They just roll over their trading promises … and that is default … and purposeful default is counterfeiting! I’ll bet Shorty has a perpetual motion machine he would like to show us as well.

Beware! This is not free money!

[MD] In a “real” money process, money is “always in free supply”. That’s not to say it is “free money”. Rather, it says money “never” restricts the trading intentions of responsible traders who create it. They “always” deliver on their promises.

It may sound like free money, but it isn’t. As more money is spent into creation, inflation takes its toll. The true definition of inflation is the increase of the money supply above the value of goods and services produced. When the money supply increases faster than the value of production, there is more money chasing fewer goods and prices rise, as the value of the money decreases. If too many dollars are created, the value of the dollar decreases. Under the Federal Reserve System the value of the dollar has decreased by 98%, meaning that something bought in 1913 for $1 would now cost $98, disregarding any increases in productivity of a particular product.

[MD] In a “real” money process, inflation takes no toll … it is guaranteed to be perpetually zero. The true definition of inflation is the amount that supply of the money itself exceeds the demand for the money … and we know in a “real” money process, supply and demand for the money itself is perpetually in perfect balance.

The fraud of the Federal Reserve System is that it was sold as a means of preserving the value of the dollar and that it would prevent crashes in the economy. Both of these selling points have not proven accurate. There have been multiple crashes of the economy since the Fed was established, including the Great Depression.

Ideally, the US dollar should be backed by gold and silver, or some tangible item, but that discussion is for later. First things first. We must End the Fed.

[MD] Gold and silver and any other commodity cannot maintain perpetual perfect balance of supply and demand for themselves. So obviously they are useless as money. Thus, your later discussion can be suspended. You don’t know what your talking about Shorty … and that is easy to prove.

The Federal Reserve has never been good for the public. It has only been good for the big banks. They love it, because it makes them money. Who pays? We do. We are slaves to debt. Isn’t it time to eliminate the Fed and turn its powers over to the US Treasury, where it belongs?

[MD] Even the blind squirrel occasionally finds an acorn. Congratulations Shorty. Governments are created by the money changers … always have been, always will be … unless we can effect iterative secession and have it our way in our own space.

Have you enjoyed the post ?

[MD] It brought some amusement. It was easy fodder for illustrating how stupid the gold bugs are.

I am a writer of novels, currently living in the woods of Montana. My 5 novels can be seen here: https://oathkeepers.org/my-5-books-shorty-dawkins/

[MD] Frightening. Hopefully that doesn’t lead to the natural conclusion that there are people reading your novels. Stupidity is already widespread enough don’t you think Shorty?

Authored by Frank Shostak via The Mises Institute,

[MD] The Mises Institute is professionally and universally clueless about money. But within that community, Frank Shostak holds the record for irrational thought. In the olden days his clarion call was “money pumping” … as if money could be pumped. Let’s see what he’s up to now.

According to the Austrian Business Cycle Theory (ABCT) the artificial lowering of interest rates by the central bank leads to a misallocation of resources because businesses undertake various capital projects that prior to the lowering of interest rates weren’t considered as viable. This misallocation of resources is commonly described as an economic boom.

[MD] According to the theory of park swings, if you push on a swing, it will oscillate. What in the world does Shostak think the business cycle is but the money changers farming operation? We here at MD know that a “real” money process does not allow any such perturbations … thus this is a non-sequitur. Now let’s watch him sequitur.

As a rule businessmen discover their error once the central bank – that was instrumental in the artificial lowering of interest rates – reverses its stance, which in turn brings to a halt capital expansion and an ensuing economic bust. From the ABCT one can infer that the artificial lowering of interest rates sets a trap for businessmen by luring them into unsustainable business activities that are only exposed once the central bank tightens its interest rate stance.

[MD] As we love to do here, we point out the nonsense that happens or is imagined to happen without a real money process in operation. What Frank writes about here “can not happen” with a real money process. INTEREST collections are in a bear hug with DEFAULTs experienced. Neither INTEREST nor DEFAULTs are a knob anyone can turn.

Critics of the ABCT maintain that there is no reason why businessmen should fall prey again and again to an artificial lowering of interest rates. Businessmen are likely to learn from experience, the critics argue, and not fall into the trap produced by an artificial lowering of interest rates. Correct expectations will undo or neutralize the whole process of the boom-bust cycle that is set in motion by the artificial lowering of interest rates. Hence, it is held, the ABCT is not a serious contender in the explanation of modern business cycle phenomena.

[MD] What Frank writes here would be true … if we had a real money process. But we don’t. We have a manipulated money process. What could be more obvious when we see them repeatedly use the term “monetary policy”. A real money process has no such capability … and never will. But the so-called “business cycle” which requires no theoretical examination … is a real tool of manipulation. And it does what it is intended to do … to put traders off balance in a “predictable way” … predictable to those turning the knobs … not to the traders suffering the manipulations.

According to a prominent critic of the ABCT, Gordon Tullock,

One would think that business people might be misled in the first couple of runs of the Rothbard cycle and not anticipate that the low interest rate will later be raised. That they would continue to be unable to figure this out, however, seems unlikely. Normally, Rothbard and other Austrians argue that entrepreneurs are well informed and make correct judgments. At the very least, one would assume that a well-informed businessperson interested in important matters concerned with the business would read Mises and Rothbard and, hence, anticipate the government action.1

[MD] Consider an inventory control analogy. If you know exactly what demand will be and have total control of supply, you can have a part arrive at the exact moment a customer comes in to buy it. But if either of those expectations cannot be expected, you must lay in “safety stock” (i.e. surplus for eventualities) to keep service percentage high. Now if someone is artificially manipulating demand or supply for their own benefit, you have two things: (1) A cheater benefiting from his behavior; and (2) A non-optimal process that must pay the cost of defending against the cheater. There’s enough of that going on in business without having it being done covertly and overtly to the money itself … especially in the name of “price stability” and “full employment”.

Even Mises himself had conceded that it is possible that some time in the future businessmen will stop responding to loose monetary policy thereby preventing the setting in motion of the boom-bust cycle.

[MD] No they won’t. In the inventory control example, the businessman statistically observed the supply and demand patterns. When they are noisy and unpredictably cyclical, he must lay in more safety stock. When they’re highly predictable, he can trim his safety stock dramatically. Let’s see what the “Mises” genius himself has to say on the subject.

In his reply to Lachmann he wrote,

It may be that businessmen will in the future react to credit expansion in another manner than they did in the past. It may be that they will avoid using for an expansion of their operations the easy money available, because they will keep in mind the inevitable end of the boom. Some signs forebode such a change. But it is too early to make a positive statement.2

[MD] Idiot! The businessman has no choice. He must serve his customers in the face of any eventuality. Picture him going to his bank and saying he’s not going to pay his mortgage this month because of “tightening” but fear not, next month there will be “loosening” and I will make both payments then.

Do Expectations Matter?

Now, a businessman has to cater for consumers future requirements if he wants to succeed in his business.

So whenever he observes a lowering in interest rates he knows that this most likely will provide a boost to the demand for various goods and services in the months ahead. Hence, if he wants to make a profit he would have to make the necessary arrangements to meet the future demand.

[MD] What is Shostak arguing for? He hasn’t made a demand to institute a “real” money process to make this manipulation impossible.

For instance, if a builder refuses to act on the likely increase in the demand for houses because he believes that this is on account of the loose monetary policy of the central bank and cannot be sustainable, then he will be out of business very quickly. To be in the building business means that he must be in tune with the demand for housing.

[MD] Actually, he’s better to be in tune with the money changer’s farming operation. That’s the tune that is being played.

Likewise, any other businessman in a given field will have to respond to the likely changes in demand in the area of his involvement if he wants to stay in business.

If a businessman has decided to be in a given business this means that the businessman is likely to cater for changes in the demand in this particular business irrespective of the underlying causes behind changes in demand. Failing to do so will put him out of business very quickly.

[MD] But do you see these businessmen or Shostak demanding the institution of a real money process? I wonder if Shostak will demand anything to deal with this manipulation problem.

Hence, regardless of expectations once the central bank tightens its stance most businessmen will “get caught”. A tighter stance will undermine demand for goods and services and this will put pressure on various business activities that sprang up whilst the interest rate stance was loose. An economic bust emerges.

Furthermore, even if businessmen have correctly anticipated the interest rate stance of the central bank and the subsequent changes in the growth rate of money supply, because of the variable time lag from money changes to its effect on economic activity it will be impossible to establish the accurate timing of the boom-bust cycle.

[MD] Frank. Read some history! Thomas Jefferson wrote in 1802 “If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children wake up homeless on the continent their Fathers conquered…. I believe that banking institutions are more dangerous to our liberties than standing armies…. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.” And even if he didn’t write it, it’s absolutely true and obvious.

Due to the time lag, prior changes in money supply could continue to dominate the economic scene for an extended period. (Given that the time lag is variable, it is not possible to ascertain when a given change in the money supply growth rate is going to start to dominate the economic scene and when the effect of past changes in money supply is going to vanish).

We can conclude that correct expectations cannot prevent boom-bust cycles once the central bank has eased its interest rate stance.

The only way to stop the menace of boom-bust cycles is for the central bank to stop the tampering with financial markets.

[MD] And the only way to get them to do that … since they’re doing it “on purpose for their farming operation” … is to INSTITUTE A REAL MONEY PROCESS TO COMPETE WITH THEM. Asking them kindly “please don’t do that” isn’t going to work.

To understand the difference between a blockchain and a traditional database, it is worth considering how each of these is designed and maintained.

Distributed nodes on a blockchain.

Traditional Databases

Traditional databases use client-server network architecture.

MD: There is no such thing as a traditional database. Databases existed way before there was a client-server orientation. But we’ll assume your client-server model for purposes of this critique.

HN: Here, a user (known as a client) can modify data, which is stored on a centralized server. Control of the database remains with a designated authority, which authenticates a client’s credentials before providing access to the database.

MD: Do you think the DNS (Domain Name Service) databases fit this model?

HN: Since this authority is responsible for administration of the database, if the security of the authority is compromised, the data can be altered, or even deleted.

MD: Can we replace “authority” with “protocol” or “process” and still assume we are talking about the same thing?

HN: Traditional Databases.

Blockchain Databases

Blockchain databases consist of several decentralized nodes. Each node participates in administration: all nodes verify new additions to the blockchain, and are capable of entering new data into the database. For an addition to be made to the blockchain, the majority of nodes must reach consensus. This consensus mechanism guarantees the security of the network, making it difficult to tamper with.

MD: Don’t “shared” and “distributed” databases have this trait? If not, how can they possibly work? How about “journaled” databases?

HN: In Bitcoin, consensus is reached by mining (solving complex hashing puzzles), while Ethereum seeks to use proof of stake as its consensus mechanism. To learn more about the difference between these two consensus mechanisms, read my earlier post.

A key property of blockchain technology, which distinguishes it from traditional database technology, is public verifiability, which is enabled by integrity and transparency.

MD: Actually “public” is a relative term. Corporations have databases that do this without blockchain technology for their own “public” that can be very large and use very distributed database technologies. And airline reservations do this through federation with franchised travel agents … all without blockchain.

HN: Integrity: every user can be sure that the data they are retrieving is uncorrupted and unaltered since the moment it was recorded

MD: Only if they are believers. The only users with anything close to such an assurance are the “developers” who supposedly know “all” the complicated mechanism involved. A distributed public transparent data organization, where “anyone” can see everything gives better assurance. This is the mechanism favored by a “proper” MOE process.

HN: Transparency: every user can verify how the blockchain has been appended over time

MD: By using “trusted” API’s. There’s no way they can know the API’s they’re using should be trusted. They’re too complicated … and they’re not open.

HN: A map of Dashcoin masternodes distributed across the world.

CRUD vs Read & Write Operations

In a traditional database, a client can perform four functions on data: Create, Read, Update, and Delete (collectively known as the CRUD commands).

MD: And if the database is distributed and journaled they can do this without the “delete” and “update” … a necessary requirement for “true” transparency.

HN: The blockchain is designed to be an append only structure. A user can only add more data, in the form of additional blocks.

MD: And this causes unnecessary and undesirable latency (which is killing Bitcoin right now). Ideally, every transaction journaled into the database is “related” by hash to every other “related” transaction. What is needed is a hash linking the journal entries … and that is very easy to provide by including an input and output hash into the hashing process itself. Most transactions in a so-called blockchain block have no relevance to each other. It makes more sense to keep “related” transaction chains together rather than “all” transaction chains. This reduces latency and synchronization problems enormously.

HN: All previous data is permanently stored and cannot be altered. Therefore, the only operations associated with blockchains are:

Read Operations: these query and retrieve data from the blockchain

Write Operations: these add more data onto the blockchain

MD: Which I have described above is not “novel” at all. We have had it with journaled distributed databases for a very long time now. We have many of the mechanisms in the various forms of RAID (Random Array of Inexpensive Drives).

HN: Validating and Writing

The blockchain allows for two functions: validation of a transaction, and writing of a new transaction. A transaction is an operation that changes the state of data that lives on the blockchain. While past entries on the blockchain must always remain the same, a new entry can change the state of the data in the past entries.

MD: This is deceptive. The data in past entries never changes. The state of the current data changes by adding transactions to previous states. And you can mitigate corruption of this process with an input and output hash linking them and included in the hash of the new transactions. No block is required. Just a journal entry with two hashes … an input hash and an output hash which includes the input hash. The input hash can be verified back in time as far as the user chooses to do so … and all users my choose to do so any time they want to prove the process integrity.

HN: For example, if the blockchain has recorded that my Bitcoin wallet has 1 million BTC, that figure is permanently stored in the blockchain.

MD: A “real” money process has no such thing as a “bitcoin” wallet. It only has to prove that something claiming to be a bitcoin is not a counterfeit. A huge flaw in the bitcoin process is the fractioning of bitcoins. This is not different in end result than the fractioning of Indian (native American) lands … where they have been fractioned so many times the parcels are too small to be of use and they cannot be practically re-aggregated.

HN: When I spend 200,000 BTC, that transaction is recorded onto the blockchain, bringing my balance to 800,000 BTC.

MD: A “real” and “proper” process cares nothing about the money once it is created by traders. It only cares that it cannot be counterfeited and that the promise creating it is delivered as promised (i.e. money is returned and destroyed). No money is in circulation without a relation (albeit not direct) to a trader’s “in-process” promise. For any given creation, money does not exist before the promise, nor after the promise is fulfilled. In the mean time it is the most common object in every simple barter exchange … because it works. And it works because it never changes value over time an space. The “process” or “protocol” guarantees it and cannot be manipulated.

HN: However, since the blockchain can only be appended, my pre-transaction balance of 1 million BTC also remains on the blockchain permanently, for those who care to look. This is why the blockchain is often referred to as an immutable and distributed ledger.

MD: With a “real” process, the money “used” by traders is totally anonymous and unaudited. It is usually just a ledger entry in a “trusted” account … trusted by the traders using it. It may temporarily be in use as a coin or currency and returned to a ledger entry. The coin and currency are just uncounterfeitable tokens that when converted to a ledger entry are placed in storage and have no value at all. “Creation” and “destruction” and “default” and “interest” collection are a different matter (than “usage”) entirely. The traders are known and singular. They are not anonymous. They aren’t aliases. They aren’t groups. Their locations are known and they can be visited. That’s what keeps the process honest and leads other traders to “use” the money. As an example, we all “create” money when we buy a house on time. The documents recording our “promise” are recorded by the county clerk and available for all to see. We know how to do this. We also know how to streamline it (by using things like credit bureaus and title companies). As we pay back our “mortgage” we return money and it is destroyed. We don’t return the same money we created … that’s just not necessary nor can it work in practice.

HN: Centralized vs. peer to peer.

In short, the difference is Decentralized Control

Decentralized control eliminates the risks of centralized control. Anybody with sufficient access to a centralized database can destroy or corrupt the data within it. Users are therefore reliant on the security infrastructure of the database administrator.

MD: And as I have illustrated, that is not the difference, because a distributed journaled database of any kind “must” have decentralized control. What is central and known is the “process” or “protocol”.

HN: Blockchain technology uses decentralized data storage to sidestep this issue, thereby building security into its very structure.

MD: The blockchain has nothing to do with centralization or decentralization. It has everything to do with mitigating “forging” and “counterfeiting” and it does it unnecessarily inefficiently, expensively, slowly, and in an unnecessarily complicated fashion.

HN: Though blockchain technology is well-suited to record certain kinds of information, traditional databases are better suited for other kinds of information. It is crucial for every organization to understand what it wants from a database, and gauge this against the strengths and vulnerabilities of each kind of database, before selecting one.

MD: A journaled database can just manage documents or links … or links to links … or links to links to links. That is irrelevant. What is relevant is transparency of what it is managing and who is interacting with it. That’s what journaling does.

The proof of stake system is attracting a lot of attention these days, with Ethereum switching over to this system from the proof of work system.

MD:

The Bitcoin (i.e. blockchain) people claim it’s main asset is that there is no central authority. But there is certainly a central process or “switching over” wouldn’t be possible. The RFC process of the entire internet has shown us it is possible to have a universally accepted process … without cryptography and without block chains and without a central authority. The DNS (Domain Name System) is a distributed database protocol that has many attributes useful for a distributed database system with no central authority. And of course it has some serious issues.

HN: Proof of stake is an alternative process for transaction verification on a blockchain. It is increasing in popularity and being adopted by several cryptocurrencies. To understand proof of stake, it is important to have a basic idea of proof of work. As of this writing, the proof of work method is used by Bitcoin, Ethereum and most other major cryptocurrencies.

MD: At MD we know for “real” money you don’t need “proof” of anything. What you need is universal transparency to things. Those things are the “creation and delivery on time and space spanning promises made by traders.”

HN: Proof of work

Proof of work is a mining process in which a user installs a powerful computer or mining rig to solve complex mathematical puzzles (known as proof of work problems). Once several calculations are successfully performed for various transactions, the verified transactions are bundled together and stored on a new ‘block’ on a distributed ledger or public blockchain. Mining verifies the legitimacy of a transaction and creates new currency units

.

MD: Digging a hole and filling it right back in is work … totally useless work. A money system that relies on useless work is an open admission that the “money” itself has zero value. Rather it “represents” something of “perceived” value … and that perception must be universal. Thus, here we have open admission of a failure of the “proof of work” scheme.

HN: The work must be moderately difficult for the miner to perform, but easy for the network to check. Multiple miners on the network attempt to be the first to find a solution for the mathematical problem concerning the candidate block. The first miner to solve the problem announces their solution simultaneously to the entire network, in turn receiving the newly created cryptocurrency unit provided by the protocol as a reward.

MD: This is admission that this scheme is even more stupid than using precious metals as money (being proof of work). At least with precious metals all miners are creating something of “real” value. And when someone else gets there first, they don’t lose their work.

HN: As more computing power is added to the network and more coins are mined, the average number of calculations required to create a new block increases, thereby increasing the difficulty level for the miner to win a reward. In proof of work currencies, miners need to recover hardware and electricity costs. This creates downward pressure on the price of the cryptocurrency from newly generated coins, thus encouraging miners to keep improving the efficiency of their mining rigs and find cheaper sources of electricity.

MD: Another open admission of the absurdity of this process. We see the predictable today. So-called “miners” use exotic bots to “steal” computer cycles from internet users. They sneak onto government owned super computers. They also create faster machines that quickly obsolete existing machines thus wasting more “real” resources. It’s not unusual for brand new state of the art ASIC and FPGA based machines to pay themselves off in one to three months … and be totally obsolete in three to six months. In the meantime, they make so much noise they drive their owners out. But they do have an advantage. They use so much electricity, they can mask a hidden marijuana operation.

HN: Bitcoin is an example of a cryptocurrency that uses the proof of work system.

MD: There is no need for the “currency” to be encrypted. In fact, in a “real” money process, the traders, the process, and the terms must be in universal plain view … and unchangeable. This is easily accomplished with simple universal hashing protocols.

HN: Mining rigs in a bitcoin mining facility.

Proof of Stake

Unlike the proof of work system, in which the user validates transactions and creates new blocks by performing a certain amount of computational work, a proof of stake system requires the user to show ownership of a certain number of cryptocurrency units.

MD: In a “real” money system, new traders creating money don’t have to be existing large money changers. Here is open admission that the “proof of stake” system copies a myth from our existing flawed (rigged actually) Medium of Exchange (MOE) process.

HN: The creator of a new block is chosen in a pseudo-random way, depending on the user’s wealth, also defined as ‘stake’. In the proof of stake system, blocks are said to be ‘forged’ or ‘minted’, not mined. Users who validate transactions and create new blocks in this system are referred to as forgers.

MD: In any MOE system, counterfeiters are often “forgers”. Interesting choice of terms isn’t it. Presumably they’re using the “forge” metaphor where existing metal is hammered into different shapes. But there is also the “faking” form where signatures and whole documents are forged. Any MOE process must prevent this. In a “real” MOE process, it is the only leak possible and is mitigated by total transparency of the money creation and destruction activity.

HN: In most proof of stake cases, digital currency units are created at the launch of the currency and their number is fixed.

MD: Bad idea. This fixing of the number “guarantees” the process will be deflationary. In a “real” process, inflation (deflation) is perpetually zero.

HN: Therefore, rather than using cryptocurrency units as reward, the forgers receive transaction fees as rewards. In a few cases, new currency units can be created by inflating the coin supply, and forgers can be rewarded with new currency units created as rewards, rather than transaction fees.

MD: What are these cases? If this can be done, how can they say the number is fixed? Also notice that their process seems to “require” that the creators of the money be “rewarded”. This is also taken from our flawed (corrupt) existing system. They implement a process of elites with power and privilege and ability to demand tribute … just like our current flawed system.

HN: In order to validate transactions and create blocks, a forger must first put their own coins at ‘stake’. Think of this as their holdings being held in an escrow account: if they validate a fraudulent transaction, they lose their holdings, as well as their rights to participate as a forger in the future.

MD: So they take their fake wealth and risk it … like putting it up as collateral. This is also from our existing flawed system. The capitalists take just two years to reclaim their stake (they collect 40%/year interest which doubles in two years). After that, they are forever playing with OPM (Other People’s Money) and risk nothing themselves at all. A “proper” MOE process uses perfect “transparency” and “interest collection according to propensity to default” to keep the players honest and provide negative feedback for stability. In a proper process, these deadbeats can pay back their defaults and return to good standing.

HN: Once the forger puts their stake up, they can partake in the forging process, and because they have staked their own money, they are in theory now incentivized to validate the right transactions.

MD: Myth in the open. Putting up a stake does not mean putting up their own money. They’ve gotten back their own money through deflation very quickly.

HN: This system does not provide a way to handle the initial distribution of coins at the founding phase of the cryptocurrency, so cryptocurrencies which use this system either begin with an ICO and sell their pre-mined coins, or begin with the proof of work system, and switch over to the proof of stake system later.

MD: Now they’re borrowing from the corporate model where a group can create a vision, sell a little less than half to suckers (in the form of stocks), hype the vision, pull out their stake but leave themselves in control, and bingo … you have another form of elite gaming of the system. And again, how do they switch systems later.?This sounds like they’re destroying the money and then using it to buy gold. Our current MOE manipulators call this the “business cycle”. It’s their “farming operation”.

HN: Cyptocurrencies that currently run the proof of stake system are BlackCoin, Lisk, Nxt and Peercoin, among others.

Proof of work mining versus proof of stake forging.

Block Selection Methods

For a proof of stake method to work effectively, there needs to be a way to select which user gets to forge the next valid block in the blockchain.

MD: There must be privileged users. In our present corrupt system we call them bankers (and sometimes governments) and they get 10x leverage over the rest of us.

HN: Selecting the forger by the size of their account balance alone would result in a permanent advantage for the richer forgers who decide to stake more of their cryptocurrency units. To counter this problem, several unique methods of selection have been created. The most popular of these methods are the ‘Randomized Block Selection’ and the ‘Coin Age Based Selection’ methods.

MD: This is characteristic of processes invented by very smart people with very good memories. Rather than seeing the rudimentary flaws in what they are doing, scrapping it, and starting over with a better concept, they run into obvious flaws we less smart people see immediately, and come up with more and more complicated workarounds … and the process soon stops because no one understands it.

HN: Randomized block selection

In the randomized block selection method of selection, a formula which looks for the user with the combination of the lowest hash value and the size of their stake, is used to select the next forger. Since the size of the stakes are public, each node is usually able to predict which user will be selected to forge the next block. Nxt and BlackCoin are two proof of work cryptocurrencies that use the randomized block selection method.

MD: This looks like an open invitation to corruption and manipulation. And when you have a “randomizing” process, the pseudo-random number generator must be open and fixed. Everyone must use the same process. The same random seed must yield the same next random number. This is problematic for obvious reasons.

HN: Coin Age based selection

The coin age based system selects the next forger based on the ‘coin age’ of the stake the potential forger has put up. Coin age is calculated by multiplying the number of days the cryptocurrency coins have been held as stake by the number of coins that are being staked.

MD: Look how long Bitcoin ran before people started to pay attention … it was several years. During that time they were giving coins away just to make it look like there was activity. Mining costs were trivial and the supply grew very quickly with the demand not growing at all. Now that it is starting to catch on (the hook is getting set), these early worthless “coins” own the process. What’s not to like about that? Duh? A Ponzi scheme with no Ponzi.

HN: Coins must have been held for a minimum of 30 days before they can compete for a block.

MD: This is building a time constant into the process … and is open for manipulation. A proper MOE process has no openings for manipulation at all.

HN: Users who have staked older and larger sets of coins have a greater chance of being assigned to forge the next block. Once a user has forged a block, their coin age is reset to zero and then they must wait at least 30 days again before they can sign another block

.

MD: How is this done? Does this mean the “timestamps” for the coins … used for determining age … can be manipulated too? What’s not to like?

HN: The user is assigned to forge the next block within a maximum period of 90 days, this prevents users with very old and large stakes from dominating the blockchain thereby making the network more secure.

MD: Another knob to manipulate … another opening for fraud and corruption … by regulators.

HN: Because a forger’s chance of success goes up the longer they fail to create a block, forgers can expect to create blocks more regularly. This mechanism promotes a healthy, decentralized forging community.

MD: This is classic complication delivering fairness. Hint people: Fairness is not complicated. But it does go against something that is current flawed wisdom … wisdom that says centralization is good. This says centralization is “not” good. So let’s apply that wisdom … iterative secession. BTW: With a “proper” MOE process, there can be any number of independent processes as long as they all deliver the same transparency and follow the same simple rule (DEFAULT perpetually equals INTEREST collected). No system can be better in any way so all competing systems are equal in performance to the traders using it.

HN: Peercoin is a proof-of-stake system based cryptocurrency which uses the coin age selection process combined with the randomized selection method. Peercoin’s developers claim that this makes a malicious attack on the network more difficult, since purchasing more than half of the coins is likely costlier than acquiring 51% of proof-of-work hashing power.

MD: Notice how all these “complicated” processes have “developers” making “claims” and solving open flaws in other complicated processes … such flaws being prone to “malicious attacks” … opened by their complexity.

HN: Most proof of stake coins that pay a reward in the form of a transaction fee for verifying transactions and creating new blocks, set a target interest rate which users can expect to earn from staking their coins.

MD: Another knob (interest) that a proper MOE process knows should never exist but rather should be an automatic negative feedback mechanism with no opening for intervention. A proper MOE process has no monetary policy. Rather, it precludes it totally.

HN: In the case of cryptocurrencies where forgers create new coins, this rate also becomes the maximum rate at which the currency supply is inflated over time.

MD: “Maximum rate”? For inflation? Over time? What a joke. They clearly have no understanding of what money is. Hint: Don’t try to create a money process without know what money is. Hint: Money is “an in-process promise to complete a trade over time and space and is “always” and only created by traders”.

HN: Proof of stake systems are more environmentally friendly and efficient, as the electricity and hardware costs are much lower than the costs associated with mining in a proof of work system.

MD: A “proper” MOE process is “perfectly” environmentally friendly and efficient. It costs nothing to create and destroy money. There is no “profit” to be made in the process anywhere. The total cost is always borne by the traders and is trivial to the size of their trades. Ideally, it is absorbed as an implicit default and is paid through interest collections on deadbeat traders. Responsible traders pay nothing at all.

HN: A greater number of people are encouraged to run nodes and get involved because it is easy and affordable to participate in this system; this results in more decentralization.

MD: In a proper MOE process, the only incentive to become a node is to decrease latency … and that is a huge incentive. It’s like a communication system with no backbone. Rather it is a mesh system where all nodes make up the connection path. This would be an obvious improvement over the current (easily manipulated) internet process. Can you say “network neutrality?”

HN: This is only a general guide to the proof of stake system. Each cryptocurrency issuer will most likely customize this system with a unique set of rules and provisions of their own as they issue their currency or switch over from the proof of work system.

MD: But the different monies themselves must be indistinguishable to the “users” (as opposed to the “creators”) of the money. And they must be non-counterfeit able.

HN: Additionally, this is a rapidly evolving industry, and apart from proof of work and proof of stake, there are currently several other systems and methodologies of transaction verification and block creation being tested and experimented with.

MD: All equally complicated and demented I’m sure.

MD: You can’t get so-called crypto currencies right if you don’t know what money is. Money is obviously and provably “an in-process promise to complete a trade over time and space.” Money is “always”, and “only” created by traders making such promises. Money is destroyed as those traders deliver as promised. And if they fail to deliver as promised the resulting DEFAULT is immediately reclaimed by INTEREST collections from new money-creating traders with a like propensity to default.

Knowing this, let’s parse this article and expose this writer’s delusions.

Bitcoin suffers a big correction after swinging wildly in the last 10 days of December. … Sometime in the next three months we will see a sell-off as latecomers panic and sell. Long-term investors will remain in bitcoin and it will creep back up, but will not revisit its December highs.

MD: Admission of failure. “Real” money doesn’t have big corrections and swings. In fact it never swings at all.

I nailed it.

Bitcoin peaked about a month ago, on December 17, at a high of nearly $20,000. As I write, the cryptocurrency is under $11,000 … a loss of about 45%. That’s more than $150 billion in lost market cap.

Cue much hand-wringing and gnashing of teeth in the crypto-commentariat. It’s neck-and-neck, but I think the “I-told-you-so” crowd has the edge over the “excuse-makers.”

Here’s the thing: Unless you just lost your shirt on bitcoin, this doesn’t matter at all. And chances are, the “experts” you may see in the press aren’t telling you why.

In fact, bitcoin’s crash is wonderful … because it means we can all just stop thinking about cryptocurrencies altogether.

The Death of Bitcoin…

In a year or so, people won’t be talking about bitcoin in the line at the grocery store or on the bus, as they are now. Here’s why.

Bitcoin is the product of justified frustration. Its designer explicitly said the cryptocurrency was a reaction to government abuse of fiat currencies like the dollar or euro. It was supposed to provide an independent, peer-to-peer payment system based on a virtual currency that couldn’t be debased, since there was a finite number of them.