MD: I had this dialog with someone calling themselves IMissLiberty on substack. We love to dissect these comments. In this conversation she is IML. I am TM (which is the same as MD). Here’s our dissection.

IML: The value of things is based on what you are willing to pay for them.

TM: Correct… sort of. It’s determined by negotiation…and that takes two parties. Once created (by making a promise spanning time and space and certifying it) money serves as any other object in simple barter exchange [SBE]…until it is destroyed (on promise delivery). In the interim it’s just stuff…like gold or dollars or pork bellies…or bottled water.

IML: Money is for saving the value of work and cost you already paid to produce something you sell today, not today’s cost to mine more.

TM: Money once created serves as the most common object in any SBE.

IML: Further, an ounce of gold found in your great grandmother’s treasure box is worth the same as the one mined and refined today–even though the costs were completely different in dollars or in whatever currency the older ounce was made.

TM: An ounce of gold is not different than a cement block…or money (after creation and before destruction) . It’s simply an object of SBE. It doesn’t matter who created it, when they created, where they stored it, what they paid for it. It’s just stuff. It’s not money. It’s just a primtive substitute…and hasn’t served as money in my nearly 80 year life time.

IML: The mining cost sets a floor but it doesn’t control demand.

TM: Supply and demand for each object (as viewed by the traders for that particular trade) dictate the trade. It’s the “negotiation” stage of all trades…SBE or otherwise. The other two stages are “promise to deliver” and “delivery”…which in SBE in the “here and now” happen simultaneously.

IML: Supply and demand are both involved in the future price of something you earn today.

TM: The so-called “price” is the exchange rate for two objects in SBE. It is set by the traders in the “negotiation” phase of the trade. The future price is estimated by “self proclaimed artists…like appraisers”…and Black and Shoals…and manipulated by governments and banks…and other imagination figments like LIBOR. It’s always a figment of someone’s imagination. However, if we’re talking about money in a “real money process”, it is always in units of HUL’s (Hours of Unskilled Labor). This simplifies the trade by twice: Both parties now know the “real undisputed value” of one of the objects. (a) It is in perpetual free supply; (b) it is in perpetual perfect supply/demand balance; (c) it is free of external loads…like interest; (d) it has no time value…doesn’t gain of lose with time or over space; (e) it costs nothing to create or destroy; (f) and cannot be counterfeited. They are left to agreeing on the value of the other object in the SBE. Ask a HUL to take an hour to make a hole; measure the hole; you will “always” get the same size hole (other conditions being equal) in all time and space.

IML:One could buy gas and store it, but gas is too volatile to carry in one’s wallet and has a limited shelf life and thus lose value.

TM: True, but irrelevant when it comes to money. Gas is not and never will be money. It’s just stuff…an object of SBE.

IML: Gold and silver have a non-perishable advantage as a store of your past costs/work.

TM: So do cement blocks. They’re all just stuff. Cement blocks have outperformed gold and silver over the last five years. When traded for dollars, gold and silver have gone up and down…cement blocks have only gone up.

IML: If I babysat for an hour in 1966 and got paid in two quarters I could spend that 50 cents to buy two gallons of gas any time in the future, and maybe more as the cost of extracting gas gets more efficient–as long as the quarters were silver.

TM: Great choice of examples. I hired baby sitters in 1966. They were paid 6 quarters per hour (I think my wife paid them 2 quarters)…same as my summer job in 1962. If we had real money then I would have paid them one HUL per hour. It was SBE.

IML: If they weren’t silver (counterfeit, paper, digital) they would barely pay the gas tax.

TM: In 1964 I paid one quarter (containing silver) for one gallon of gas (SBE). In 1965 I traded one quarter (containing no silver) for one gallon of gas (SBE). It proved the quarter itself traded for the gas. What it was made of (i.e. its intrinsic value) played no role. It’s even more dramatic today. You pay 10+ quarters (containing zero silver…or 90% silver) for a gallon of gas. You’re foolish to trade the silver quarters because they trade for more value in a different context…e.g. in making photographic film. That’s how money works. And why commodity money doesn’t work. In the case of coin: (1)the cheaper you can make it; (2) the more durable you can make it; (3) the more precisely you can control its dimensions (ie. weight, diameter, thickness); (4) and the more difficult you can make counterfeiting…the better. But it’s still just stuff when it comes to SBE.

IML: “Compared to the dollar” a decaying rubber-band yardstick is no better at measuring carpet than a dollar price over time, except it will fail much sooner and be replaced with something more useful.

TM: And this is the same for any object of SBE. An 1848 ounce of gold was worth more than an 1850 ounce. Supply changed dramatically in those years. At the end of the 1800’s the value of gold and silver gyrated…until by law they claimed silver was not legal tender…only gold and so-called gold backed paper was legal tender (another government imagination figment). In 1973 the French were owed some huge amount of money…let’s say it was $1B. The USA claimed an ounce of gold could be purchased for $35. The French knew by experience it cost $70+ to trade (SBE) for an ounce of gold. The French said, keep your dollars USA. You agreed to settle the debt in gold and we’ll take the gold. Tilt went the so-called “lie” called the gold standard. Nixon didn’t cause the failure. He just could no longer lie about it as his predecessors had. If we were on a “real money process”, the units of the debt would have been HULs and guaranteed never to change their value over time and space. Such fictions as gold stability have existed over all time and space.

An interesting exercise when comparing and contrasting two competing choices. If one of the choices is current practice and the other one is a claimed improvement, reverse their positions. Assume the new choice is the current practice, and vice versa. Now which one is harder to sell? This technique removes the inertial advantage all current practice has. It illustrates dramatically how ridiculous most “conservative” practices are. Electric cars vs ICE (Internal Combustion Engine) cars is a good case to practice on.

IML: If 1913 had been gold instead of a central bank, the income tax would still only tax the top 1% as promised, and it would be enough for peace and prosperity, but not enough for war.

TM: This is the Achilles heel of all government controlled money. Governments collect taxes to pay interest to the money changers who institute them. Governments sustain themselves through counterfeiting of money they claim to control. Central Banks are figments of the money changers imagination forced upon governments. They need them for another figment of their imagination…that being “reserves”. In a “real money process” there are no reserves. No one has to put their savings in a bank for the bank to loan out ten times that savings at a 4% spread (i.e.40% which doubles in less than 2 years) . And thus there is no such thing as a “run on the bank”. All trades are completely separate and isolated.

This is an interesting definition of a capitalist…i.e. two years. They create a bank; capitalize it; accept deposits; loan out ten times the deposits at 4% spread; double their money in 2 years; take 1/2 off the table removing all their original risk; and wallah…look mom, I’m a capitalist. What’s not to love about capitalism.

IML: The miners and refiners produce more when the price offered is higher than the cost of production. They stop when they are not offered enough, and then the supply drops. If they are hungry, they will produce enough for food or for dollars for food–it’s a market price.

TM: You can say the same for farmers growing corn or raising pigs. They’re just stuff in SBE.

IML: There is always demand for metals. Try to imagine life without them.

TM: Try to imagine life without food…or without water where it doesn’t rain much. Both are just stuff in SBE. In the case of rain it is genuinely free. In the case of food…not so much. And in times of food and water shortages, metals play second fiddle.

IML: Imagine filling your cavity with bitcoin or paper.

TM: I have. See this to know about Bitcoin: https://moneydelusions.com/wp/?s=bitcoin. Bitcoin dramatically illustrates that DEFLATION is even worse than INFLATION. The only “proper” level of each is zero. No process can measure it. And only a “real money” process can guarantee it to be zero…it’s the nature of the process: INFLATION = DEFAULT – INTEREST = zero.

IML: There is no similar floor under fiat currencies. The dollar and bitcoin are ultimately worth their weight in gold ($0).

TM: When you know what money is (i.e. a promise to complete a trade over time and space); when you know where money comes from (i.e. created by traders like you an me buying stuff with time payments); when you know where money goes (i.e. returned and destroyed with each time payment…or mitigated by INTEREST collections of like amount when DEFAULTed). The operative relation is: INFLATION = DEFAULT – INTEREST = Zero.

I value gold these days at roughly $2,000 per ounce. If you take all the gold in the whole world and divide it by the number of people, you get about one ounce per person as I recall…i.e. roughly $2,000…i.e. roughly 200 HULs. First, that’s not near enough for anybody’s need in trade…not in the near term…certainly not over time and space. But more importantly, the HULs are the only object guaranteed to have exactly the same value in every SBE. Gold goes up and down. Dollars go up…until they call the loans…then they go down dramatically. And as usual with all fake money…up is down and down is up when you think about it.

MD: The Mises Monks are always great fodder for illustrating the spread of confusion and delusions as to what money “really” is. Let’s dissect this one.

One of history’s greatest ironies is that gold detractors refer to the metal as the barbarous relic. In fact, the abandonment of gold has put civilization as we know it at risk of extinction.

MD: How’s that for an opening line? The Monks never disappoint. “Greatest Ironies”; “gold detractors”;” barbarous relic”: Yet they never seem to be able to tell us what money really is. But this may be going too far. Removing “gold” will “risk extinctions”?

Gold’s main use is in jewelry and plating electrical contacts. Once used to fill teeth, it’s been a very long time since gold was used for that (except for Negros who use it to decorate their faces.) And in no lifetime of anyone living today has gold served as money. And silver ceased serving as money in 1965…almost 10 years before Nixon declared the obvious…that the so-called gold backing of the dollar was a giant fiction…a fraud on which the French called them out.

The only risk to extinction was use of mercury amalgamating silver to fill teeth. It was shown to be poison…like lead in paint and gasoline. Precious metals have never been money. They are just clumsy expensive stand-ins for what money really is…”a promise”. And what do these Monks call real money? They call it “fiat money”…and make it a derogatory slur. Since when is a “promise” derogatory. Let’s continue.

The gold coin standard that had served Western economies so brilliantly throughout most of the nineteenth century hit a brick wall in 1914 and was never able to recover, or so the story goes. As the Great War began, Europe turned from prosperity to destruction, or more precisely, toward prosperity for some and destruction for the rest. The gold coin standard had to be ditched for such a prodigious undertaking.

MD: Served economies “brilliantly”? Economic panics were as regular then as pandemics are becoming today. And in 1913 (a year before this so-called brick wall), the Federal Reserve Act began to plague us with the money we have today…a money that States freely counterfeit…and that money-changers collect interest on…and that both manipulate to deliver the so-called “business cycle”. “Prodigious undertaking”? Oh please!

If gold was money, and wars cost money, how was this even possible?

MD: A Mises Monk might be close to getting something right here. You can’t support a war if you can’t pay for it. And if gold is money…with only about one ounce per person on Earth (less than $2,000)…you’re not going to support war with gold. But you can by counterfeiting. They claim Lincoln did this to finance the USA Civil War in the 1860’s…and that’s correct. But when that counterfeit money (Greenbacks) was paid back, it ceased to be counterfeit. It “proved” to be “real” money. That hasn’t happened with any war since. The State just rolls its counterfeit money over by taking out new loans to pay off the old.

First, people were already in the habit of using money substitutes instead of money itself—banknotes instead of the gold coins they represented. People found it more convenient to carry paper around in their pockets than gold coins. Over time the paper itself came to be regarded as money, while gold became a clunky inconvenience from the old days.

MD: Well, the Monks being right didn’t last long did it? Here at Money Delusions we know money is an “in-process promise to complete a trade spanning time and space”. It is only created by traders like you and me. It begins as a ledger entry…open to all to see. And it ends with delivery on the promise and reversal of that ledger entry documenting the promise…again for all to see. In the interim it may remain a ledger entry; it may become a “demand deposit” (i.e. check); it may become a paper chit (currency); it may become a token (a coin). As such, it becomes the most common object of every simple barter exchange. But in the end it becomes a reversing entry in a ledger and is extinguished forever…for that trading promise. And if the promise is broken (defaulted) an “interest collection” of like amount is immediately made to recover the “orphaned” money. This guarantees perpetual perfect balance of supply and demand for the money itself…and thus zero “inflation”.

Second, banks had been in the habit of issuing more bank-notes and deposits than the value of the gold in their vaults. On occasion, this practice would arouse public suspicion that the notes were promises the banks could not keep. The courts sided with the banks and allowed them to suspend note redemption while staying in business, thus strengthening the government-bank alliance. Since the courts ruled that deposits belonged to the banks, bankers could not be accused of embezzlement. The occasional bank runs that erupted were interpreted as a self-fulfilling prophecy. If people lined up to withdraw their money because they believed their bank was insolvent, the bank soon would be. People had no idea their banks were loaning out most of their deposits. They did not know fractional reserve banking, a form of counterfeiting, was the norm.

MD: That’s not a “habit”…it’s by design. Money-changers instituted the State. The State chartered the Banks (owned by the Money-changers)…and gave them a 10x leverage advantage over traders like you and me. And when those scoundrels abused even that enormous privilege, the State they created defended them…as designed. It’s not a government-bank alliance. The State is a “creation and tool” of the Money-changers. And the State fiction of Laws sealed the deal. They pass one law that dilutes the golden rule and bammo…everything else that isn’t against the law (but violates the golden rule) is suddenly legal. And that obvious problem created here brings us 40,000 new laws each year…trying to put the Genie back in the bottle…trying to make us comply with that one simple golden rule.

And why didn’t the people know this was going on? Because there was “secrecy” in banking. Money requires “authentication” of the trader creating it and “transparency” of the promise to all lookers. And “defaults” are evident to all lookers “immediately”…and immediately mitigated by “interest collections” of like amount.

Here again, the Monks get close to saying what’s going down. Money “is” fiat…and that’s good. It’s what makes it so efficient in trade. But a “real” money process gives “no” trader an advantage…not even the Money-changers; their States; or their Banks. In this context, the “fraction” is not 10x…but rather infinite to the trader. And there is no reserve. Unlike a water well, you don’t have to prime the pump. But if you don’t replace the water you pump, you don’t get to pump again…until you replace that water. Lots of metaphors going on here.

Gold coin redemption requirements put limits on fractional reserve banking. Such limits were not welcomed by banks. Since banks could loan to the government, limitations also capped government spending, so the government did not like the limitations of gold coin redemption either.

MD: What “coin redemption requirements”? They were always a fiction. Gold coins were never used in my lifetime. And silver coins quit being used in 1964…and changed nothing in the behavior of traders… proving that precious metal was not money. Rather, it was the “token” that was money. At the same time, the paper money which said “Silver Certificate” changed to saying “Federal Reserve Note”…and as far as traders like you and me were concerned, nothing changed.

We never asked for the silver promised by those certificates. We had no use for it. It weighed too much and was too bulky. But for non-traders, the change was large. These non-traders are called “investors”. They’re really just gamblers. And they immediately gobbled up all the silver. You can now buy it on eBay (google “Silver Roosevelt Dimes 90% Junk Constitutional Circulated *Guaranteed Cheapest!”). It sells for (i.e. trades for) $4.50 for 10 dimes…dimes that used to trade for two candy bars…before State counterfeiting withered the dollar to its current condition.

And “government limitations”? Does anyone really believe there is such a thing as a government limitation? All governments are by their very definition “unlimited”!

Which brings us to the wall gold allegedly hit.

Preparing for War Means Preparing for Inflation

In his 1949 book, Economics and the Public Welfare, economist Benjamin Anderson tells us, “the war [in 1914] came as a great shock, not only to the masses of the American people, but also to most well-informed Americans—and, for that matter, to most Europeans.” And yet, Germany, Russia, and France began accumulating gold prior to the war (with Germany starting first in 1912). Gold was taken “out of the hands of the people” and carried to the reserves of the Reichsbank, the German central bank. People were given paper notes “to take the place of gold in circulation.”

MD: It goes all the way back to the Battle of Waterloo! … and for all time before that! All wars are “bankers” wars (i.e. money-changer wars). And if they had a “real money process” back then, they could have taken up all the gold they wanted. Traders had no use for it. There are no “reserves” in a real money process. It’s promises with which we deal. The only thing that can destroy a promise is to destroy the record of the promise…or destroy the person who made the promise. And a “real money process” mitigates such contingencies with “interest collections of like amount.” It’s simple arithmetic. Who pays the interest? Only traders who have a propensity to default pay it. And those traders have to work that much harder if they want to continue to trade at all, because once the defaults get too large, the marketplace ostracizes them.

When war broke out in August 1914, Gary North explains that the pre–World War I policy of gold coin redemption was

independently but almost simultaneously revoked by European governments. . . . They all then resorted to monetary inflation. This was a way to conceal from the public the true costs of the war. They imposed an inflation tax, and could then blame any price hikes on unpatriotic price gouging. This rested on widespread ignorance regarding economic cause and effects regarding monetary inflation and price inflation. They could not have done this if citizens had possessed the pre-war right to demand payment in gold coins at a fixed rate. They would have made a run on the banks. Governments could not have inflated without reneging on their promises to redeem their currencies for gold coins. So, they reneged while they still had the gold. Better early contract-breaking than late, they concluded.

MD: Earth to Monks. You just made our case. You’ve shown that precious metals are no cure to State deviance and malfeasance. A “real money process” has no State sponsorship. It has no Money-changer sponsorship. It has only trader and their marketplace sponsorship. And it depends on “authenticating” the trader and “accounting” for the trader’s promises. By the classical triple “A”s of trade: (1) Authentication; (2) Authority; (3) Accounting; all “responsible” traders (i.e. those with no propensity to default) have equal “authority” to create money. Those with non-zero propensity to default pay insurance “premiums” which are called “interest collections”. And they’re not arbitrarily set in the smokey rooms of LIBOR . They always equal “defaults incurred”. I’ve always wondered why banks always tell us the “prevailing interest”…but never show us the “prevailing defaults”. Now I no longer wonder. It enables their “business cycle”. It enables the “front running”of economic perturbations they themselves cause by “throttling” the money supply …supposedly in the interest of controlling inflation (which they cause) and maintaining full employment (which they can’t control at all).

If governments had not broken their promise to redeem paper notes for gold coins, they would have had to negotiate their differences rather than engage in one of the deadliest wars in history. Abandoning the gold coin standard, which had always been under government control, was the deciding factor in going to war.

MD: Duh! How about we do an “iterative secession”. How about we do without government altogether.

Though the US did not formally abandon gold during its late participation in the war, it discouraged redemption while roughly doubling the money supply. Blanchard Economic Research discusses the situation in “War and Inflation”:

MD: If gold is money, how did they “double” the money supply? These Monks are beyond stupid. In a “real money process”, you can only double money supply by doubling trader promises. And traders don’t make promises they can’t see clear to delivering. But get rid of government and the money-changers that create it and bammo…a doubling of trade would be minuscule.

War also causes the type of inflation that results from a rapid expansion of money and credit. “In World War I, the American people were characteristically unwilling to finance the total war effort out of increased taxes. This had been true in the Civil War and would also be so in World War II and the Vietnam War. Much of the expenditures in World War I, were financed out of the inflationary increases in the money supply.”

MD: When it comes to money, there’s only one type of inflation. That is when supply exceeds demand for the money itself. And this is impossible in a “real money process”. And as we pointed out earlier, the Civil War was different from all following wars. The Greenbacks were “all” recovered (“Greenbacks then became freely convertible into gold“)

Governments had a choice to make: fight a long, bloody war for specious reasons, or retain the gold coin standard. They chose war. US leaders found their decision irresistible. It was not J.P. Morgan, Woodrow Wilson, Edward Mandell House, or Benjamin Strong who would be fighting in the trenches.

When we hear that “going off gold” was the prerequisite for global peace and harmony, we should remember places such as the Meuse-Argonne American Cemetery in France, where grave markers seemingly extend to infinity. These are mostly the graves of young men who died for nothing but the lies of politicians and the profits of the politically connected. Gold wanted no part in the slaughter. But politicians and bankers knew a paper fiat standard was the monetary prerequisite to achieving their goals.

MD: Every time I ask one of the Mises Monks how you can use gold as money when there’s only one ounce per person on Earth? …i.e. less than $2,000…1/2 what someone at Home Depot makes in a month! The line goes dead.

Conclusion

John Maynard Keynes, who coined the term “barbarous relic” in reference to the gold standard, wrote about the world that was lost when gold was abandoned:

What an extraordinary episode in the economic progress of man that age was which came to an end in August, 1914! . . . The inhabitant of London could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery upon his doorstep. . . . He could secure forthwith, if he wished it, cheap and comfortable means of transit to any country or climate without passport or other formality, could despatch his servant to the neighboring office of a bank for such supply of the precious metals as might seem convenient, and could then proceed abroad to foreign quarters, without knowledge of their religion, language, or customs, bearing coined wealth upon his person, and would consider himself greatly aggrieved and much surprised at the least interference. But, most important of all, he regarded this state of affairs as normal, certain, and permanent, except in the direction of further improvement, and any deviation from it as aberrant, scandalous, and avoidable.

If Keynes had read what he wrote, he might have been a better economist. And we might be living in a better world today.

MD: This is shades of the Red vs. Blue; The Donkeys vs. the Elephants; the Harlem Globe Trotters vs. the Washington Generals; the Keynesians vs the Mises Monks. You’re never going to solve a problem when you’re given two choices, both bad, and both controlled by a single non-choice. Such is democracy. Long live democracy.

George Ford Smith is a former mainframe and PC programmer and technology instructor, the author of eight books including a novel about a renegade Fed chairman (Flight of the Barbarous Relic), a filmmaker (Do Not Consent), and an advocate of stateless market government. He welcomes speaking engagements and can be reached at gfs543@icloud.com.

If The Fed Starts A Digital Currency, It Had Better Guarantee Privacy Tyler Durden’s Photo by Tyler Durden Tuesday, Apr 05, 2022 – 08:00 PM

MD: As always, Money Delusions will use the true definition of “real” money to annotate this article. The article appear in ZeroHedge.com as “If the Fed Starts A Digital Currency, It Had Better Guarantee Privacy”. And the title itself reveals confusion about what money is…and what its characteristics are. This begins by knowing what money is (i.e “an in-process promise to complete a trade over time and space”); how money is created (i.e. transparently in plain view by traders like you and me); how money is destroyed (i.e. also transparently by the trader delivering as promised); what happens if the trader “defaults” (i.e. “interest” of like amount is immediately collected); and how money trades in the interim (i.e. anonymously as any other object of simple-barter-exchange). Let’s get started:

Authored by By Andrew M. Bailey & William J. Luther via RealClearPolicy.com,

President Biden’s latest executive order calls for extensive research on digital assets and may usher in a U.S. central bank digital currency (CBDC), eventually allowing individuals to maintain accounts with the Federal Reserve. Other central banks are already on the job. The People’s Bank of China began piloting a digital renminbi in April 2021. India’s Reserve Bank intends to launch a digital rupee as early as this year.

MD: They immediately exhibit that they don’t know what money is. “Banks” have nothing to do with “real” money at all. It is the most obvious corruption of real money. And “digital” is just one of many forms of money.

Most commonly, money is just an entry in a ledger. In some cases it is in the form of coins and currency…both carefully designed to resist counterfeiting. In some cases it is in the form of a check (i.e. against a demand deposit). And we already have a fairly digital form of money in “debit cards”…a link to your ledger records that you carry in your purse. “Credit cards” are not an example of money. Rather, they are an example of “money creation”.

When you charge something on a credit card, “you” are creating money…a promise to complete a trade over time and space. When you use a “debit card” you are merely submitting proof that you hold some previously created money.

A CBDC may upgrade the physical cash the Federal Reserve already issues – but only if its designers appreciate the value of financial privacy.

Cash is a 7th century technology, with obvious drawbacks today. It pays no interest, is less secure than a bank deposit, and is difficult to insure against loss or theft. It is unwieldy for large transactions, and also requires those transacting to be at the same place at the same time — a big problem in an increasingly digital world.

MD: And before cash we had the tally stick…which claims to be the best implementation of money. And tally sticks were “real” money. They represented a promise to complete a trade over time and space. They worked better than gold. In fact, they could claim any kind of “backing” the trader’s agreed to (e.g. pork bellies). But nobody “traded” tally sticks. Thus, in that respect they weren’t money at all. They really were close to “crypto” in that respect…but much cheaper to create. You could create a tally stick with a twig and a knife. Today’s crypto requires insane amounts of electricity waste to create. They call it “proof of work”…which of course is nonsense.

Nonetheless, cash remains popular. Circulating U.S. currency exceeded $2.2 trillion in January 2022, more than doubling over the last decade. The inflation-adjusted value of circulating notes grew more than 5.5 percent per year over the period. And U.S. consumers used cash in 19 percent of transactions in 2020.

MD: Actually, the money changers are revealing the imminent collapse of cash. They hold lots of cash (counterfeited by government) and are doing everything they can to exchange it for real “property”. I get a dozen calls a day from “so-called investors” who want to “buy” my property. It’s a game of musical chairs. They don’t want to holding it when the “reset” comes as they know it will be instantly worthless. And also note, with “real” money, inflation is perpetually zero. No adjusted valuation is ever necessary.

Why is cash so popular, despite its drawbacks? Cash is easy to use. There are no bank or merchant terminal fees associated with cash. And, most importantly, it offers more financial privacy than the available alternatives.

MD: In actuality, cash is “not” easy to use. You almost never see it being used…even in restaurants and bars. I use it in bars just to keep score. I take a certain amount of cash, which when I’ve used it up I know I’m about to have had too much to drink. I spend lots of time explaining to other patrons why I can’t let them buy me a beer.

When you use cash, no one other than the recipient needs to know. Unlike a check or debit card transaction, there’s no bank recording how you spend your money. You can donate to a political or religious cause, buy controversial books or magazines, or secure medicine or medical treatment without much concern that governments, corporations, or snoopy neighbors will ever find out.

MD: With a “real” money implementation, there is no need for banks to be involved. All that is necessary is a “block chain” like implementation that resists the “three general problem” and counterfeiting. And when properly implemented, the “block chain” implementation is cost free. It has no use for “proof of work”. It “knows” it’s keeping track of performance on promises.

Privacy means you get to decide whether to disclose the intimate details of your life. Some will happily share. That is their choice. But others will prefer to keep those details private.

MD: But keep in mind, while “real” money used in trade is “always anonymous”, it’s creation is always “open and transparent”. Awareness of this distinction is crucial.

In a digital world, personal information can spread far and wide. And it can be used to exclude or exploit people on the margins. The choice about what information to share is important. For some, flourishing depends on carefully choosing how much others know about their politics, religion, relationships, or medical conditions.

Financial privacy matters just as much as privacy in other areas. What we do reveals much more about who we are than what we say. And what we do often requires spending money. In many cases, meaningful privacy requires financial privacy.

MD: Again, keep in mind that money is only concerned with the problem of “counterfeiting”. It cares not at all who is using it and for what. But people using it must know and expect it is genuine…i.e. not counterfeited. And of course we all know the principal counterfeiters of money are governments. For a “real” money process to exist, it’s operation must be transparent and impervious to any attempts to control or to counterfeit it. It is simply about record keeping.

Privacy also operationalizes the presumption of innocence and promotes due process. You are not obliged to testify against yourself. If law enforcement believes you have done something unlawful, they must convince a judge to issue a warrant before rifling through your things. Likewise, financial privacy prevents authorities from monitoring your transactions without authorization.

MD: Law doesn’t apply to a “real” money process. But open communication and mitigation is crucial. Again, it’s about making counterfeiting impossible. And when detected it must reveal who did the counterfeiting; see that the counterfeiting doesn’t happen again; and treat the counterfeiting for what it is… a “default”. And thus it immediately mitigates it with “interest” collection of like amount. This must be totally transparent…so the marketplace can ostracize the perps. Who pays the interest? Other irresponsible traders.

The recent executive order, to the administration’s credit, notes that a CBDC should “maintain privacy; and shield against arbitrary or unlawful surveillance, which can contribute to human rights abuses.” But a reasonable person might worry that the government is paying lip service to privacy concerns.

MD: A principle “axiom” must be observed at all times. If you are considering a government solution to any problem, you are still looking for a solution. Government is “never” the solution to any problem. It is just a magnifier of the problem.

A recent paper from the Fed, offered as “the first step in a public discussion” about CBDCs, suggests the central bank has no interest in guaranteeing privacy at the design stage. Instead, it maintains that a “CBDC would need to strike an appropriate balance […] between safeguarding the privacy rights of consumers and affording the transparency necessary to deter criminal activity.” The Fed then solicits comments on how a CBDC might “provide privacy to consumers without providing complete anonymity,” which it seems to equate with “facilitating illicit financial activity.” A U.S. CBDC, in other words, will likely offer much less privacy than cash.

MD: No central entity (especially a central bank) is ever involved in a “real” money process. Rather, it is the “process” that is the entity. As such, the process is universally used and totally transparent to all traders at all times.

We do not deny that financial privacy benefits criminals and tax cheats. Such claims tend to be exaggerated, though. In reality, it is a small price to pay for civil liberty. That due process applies to everyone — criminals included — is no reason to scrap the Fourth or Fifth Amendments.

MD: Taxes implies government…so it is a non-starter. If government participation was ever a valid option, it would be the “only” viable option. You would pay taxes (and only taxes) for everything. Your gasoline, your groceries, your clothing…all would be free. You would just pay tax and it would be covered out of that. Some people call this communism. Some call it insurance. It’s all nonsense.

Policymakers may be tempted to compromise on financial privacy when implementing a CBDC. Instead, they should attempt to replicate the privacy afforded by cash. Like non-alcoholic beer, the Fed’s “digital form of paper money” would superficially resemble the real McCoy while lacking its defining feature.

MD: Policy is the the marker here. No process is every properly governed by policy. The closest we should ever come to adopting policy is the “golden rule”. Policy is different from process. Money is a “process”. It cares nothing about policies like full employment and setting inflation at 2% (while continuously failing by a factor of 2).

MD: Note: There are charts

embedded in this article

which link back to the original. In time they will likely get

broken.

MD: A proper MOE (Medium of Exchange or Money) Process

treats all “traders” equally. But this instance does bring on to

the stage an important case. What limits should be placed on the

size of “promises” it will embrace…and why?

The case is fairly simple for individuals. It easily embraces

the case for viable shelter (buying a house). It easily embraces the

case for viable transportation (buying a car). It easily embraces

the case for unanticipated medical needs (supplementing insurance).

But how does it deal with the case for highly leveraged promises?

I will answer this question as I read the article and

intersperse my comments. Hopefully it will address these issues. The

most important issues are regarding “leverage” and detection of

“rollovers”.

The only way to get really wealthy in any society is through

unusual leverage.

Banks grant themselves 10x the leverage you and I have. As

individuals we have no leverage. We work an hour…we make some

number of HULS (note: HULs…Hours of Unskilled Labor… are the

ideal MOE measure). We must be really really good at what we do

(e.g. neurosurgery) to be worth 10x what we were in high school).

The mom and pop shop has almost no leverage. They “are”

the business. But as they grow they hire help. And that is the

beginning of their leverage growth. They take a piece of their

workers’ labor as if they performed it themselves. As they grow they

retain earnings but may also take on debt (i.e. they make money

creating promises) or they take on partners (sell shares in their

company). The money creating case is problematic. You can’t just say

I want to create a car company and create $100B (or 10B HULS).

Then we have the financial wizards. They claim to be able to

deploy surplus HULs better those who earn those HULs. And they take

a piece of the action if they succeed. They don’t suffer if they

fail; their clients do the suffering. They use options, derivatives,

high speed trading, and myriad other tricks to multiply the natural

leverage this game brings them.

Selling shares is not problematic. Each shareholder has to

decide how he’s going to come up with the money to pay for his

share. And the business itself decides how it will reward his

participation. There are many games being played in this space to

help mom and pop keep control as they grow. For example, they can

give themselves options to buy shares as payment. They can mix debt

and equity instruments as warrants. The options have proven to be

inexhaustible…their consequences unknowable and unsupportable.

Such tactics are of no concern to the MOE process. Its only

interest is in the “reasonableness” of the money creation and

tracking its return and destruction. That means assessing the

trader’s propensity to default and monitoring his performance in

real time. And we know how to address such issues. We call them

actuaries. They have great experience in the mutual casualty

insurance business.

So now lets see how we address this very unusual but real

instance of a threat to the MOE process. More importantly, we see

how the MOE process places the responsibility exactly where it

belongs…with the promise maker and with the process behavior. This

characteristic gives some assurance of self discipline.

If the trader screws up, the trader must back his failed

promise or he must pay the consequences (i.e. be banned from

creating money…as we know all governments will be banned if they

don’t change their behavior).

If the process screws up (i.e. supports an irresponsible

trader), it must penalize oncoming traders (responsible or

irresponsible) immediately. They pay INTEREST (which is returned if

they prove to be responsible).

Now to the article. My interspersed comments appear formatted

as this pretext is formatted. And please bear with me…I’m thinking

through this as I write and it’s worth at least what you’re paying

for it.

==================

Well, with everyone and everything else getting a bailout, may as

well go all the way.

MD: What a remarkable opening. Is that like “if rape

is inevitable, relax and enjoy it”?

Two months after we

reported that the state of California is trying to turn

centuries of finance on its head by allowing businesses to walk away

from commercial leases – in other words to make commercial debt

non-recourse – a move the California Business Properties Association

said “could cause a financial collapse”, attempts to bail

out commercial lenders have reached the Federal level, with the WSJ

reporting that lawmakers have introduced a bill to provide

cash to struggling hotels and shopping centers that weren’t able

to pause mortgage payments after the coronavirus shut down the U.S.

Economy.

MD: Well, the concept of “throwing good money after bad” is well known. And this likely falls into that category. Shopping malls have become a thing of the past. They had their 50years in the sun and have now been made obsolete by a better idea (.e.g. Amazon). The handwriting was on the wall way before the COVID-19 hoax and government lock-down suspended trade. COVID-19 is a neutron bomb attack. It kills people but doesn’t destroy things. For those still alive, a restart should be a simple process. Suspend the delivery on existing money creating promises until the external restrictions have been lifted. Continue to support new money creating promises using regular actuarial principles. Such principles will detect “rollover” attempts and reject them.

I think the obvious solution is to recognize the situation and do an “automatic extension” of promise time terms (the “time” part of the time and space spanning trade) of all affected promises, and move painlessly on down the road. Nobody gets hurt.

The bill would set up a government-backed funding vehicle which

companies could tap to stay current on their mortgages. It is meant

in particular to help those who borrowed in the $550 billion CMBS

market in which mortgages are re-packaged into bonds and sold to

Wall Street. What it really represents, is a bailout of the only

group of borrowers that had so far not found access to the Fed’s

various generous rescue facilities: and that’s where Congress comes

in.

MD: The problem as expressed here does not exist with a

proper MOE process. Money is not “backed” by anything but the

process. So there is no such thing as a CMBS market or

mortgage-backed securities and bonds. If we had a proper MOE

process, such techniques could still exist for those who want the

risk of non-responsible traders. But that is no concern or

responsibility of the money process. And the phrase

“government-backed funding vehicle” is a marker. This is not a

viable proposal with the word “government” in it.

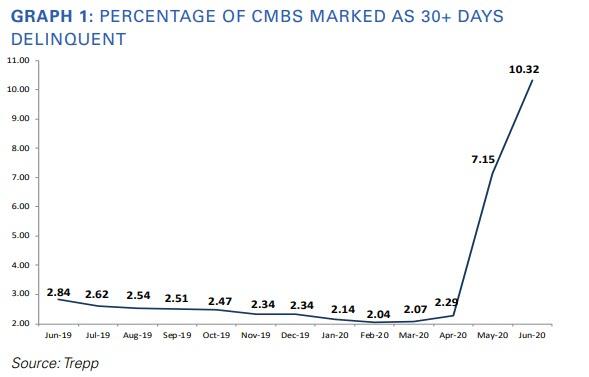

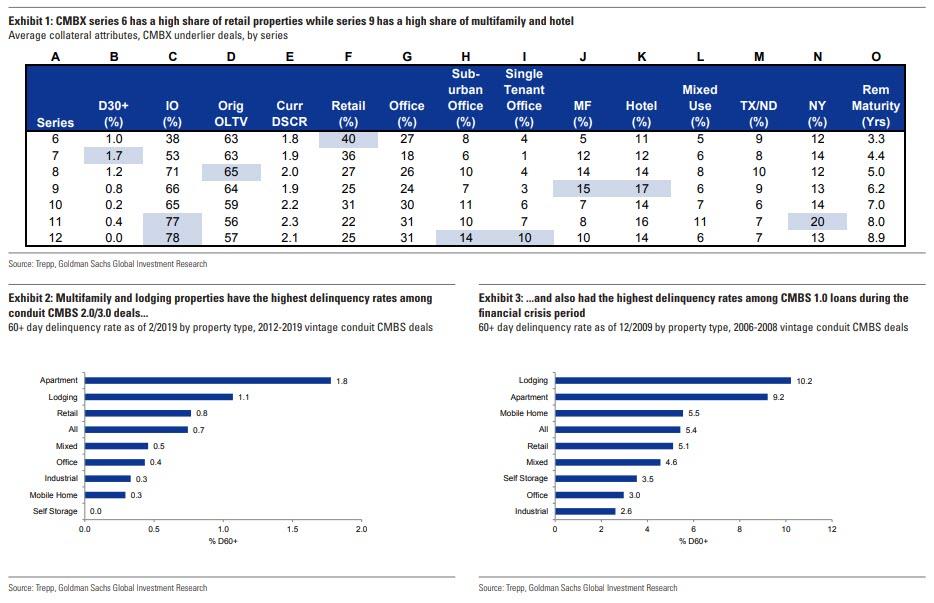

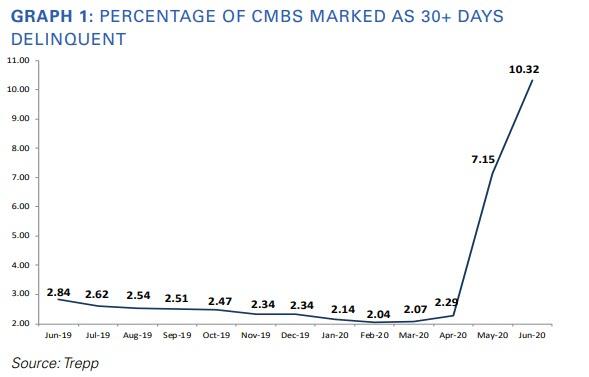

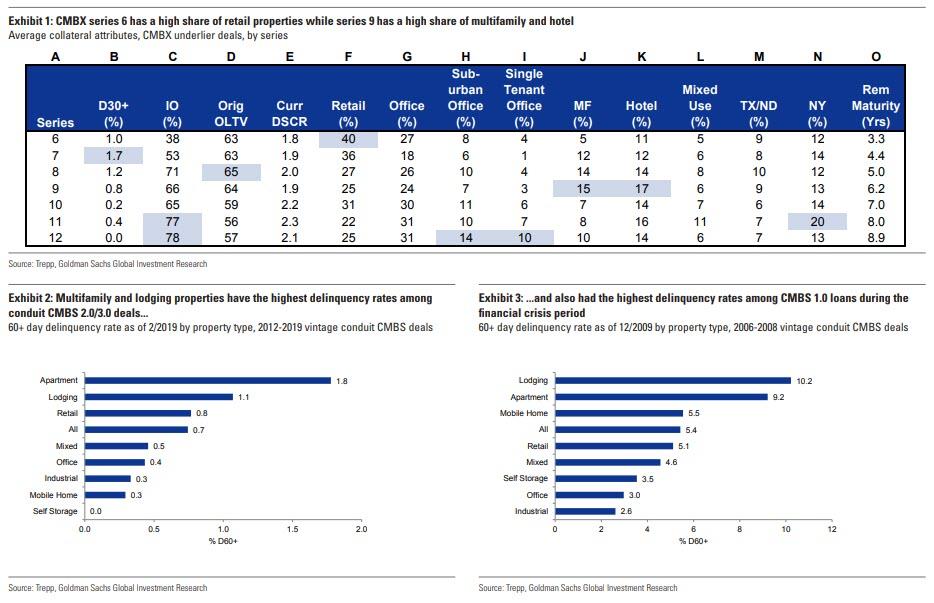

To be sure, the commercial real estate market is imploding, and

as we reported at the start of the month, some 10% of loans in

commercial mortgage-backed securities were 30 or more days

delinquent at the end of June, including nearly a quarter of loans

tied to the hard-hit hotel industry, according to Trepp LLC.

MD: And if those leases were taken on by trader created

money, then an automatic 30 day extension would have already been

applied to their promise. Such extensions could go on indefinitely.

There are no so-called investors involved at all. Mom and pop

created the money (they created money for the full lease as if it

was a purchase…but is paid out to the seller monthly) and this is

one of those unavoidable occurrences that the money process

naturally accommodates. Loan sharks anticipate this too. They take

the property. Moving these leases into the MOE process space stops

the domino effect such instances create.

MD: The above curve illustrates the superiority of the

MOE process solution. In April, the COVID-19 hoax lock down

occurred. Up until then the market was healthy and getting more

healthy. Then wammo!. With the MOE process, the above curve would go

flat…or maybe even continue to go down. And a new curve would

start up. That curve would be the automatic extensions of the time

component of the money creating promises. There is no pain to anyone

anywhere…and everyone is still responsible for their promise.

Note, this concept also applies to floor plans purchased in

anticipation of normal business sales performance…now interrupted

by the lock down. Such provisions are now provided by banks through

lines of credit or compensating balance loans…and they profit

exorbitantly.

“The numbers are getting more dire and the projections are

getting more stern,” said Rep. Van Taylor (R., Texas), who is

sponsoring the bill alongside Rep. Al Lawson (D., Fla.).

MD: In our system “sponsoring a bill” means “bowing

to a lobbyist”. That’s how our corrupt system works. That’s what

gives the wealthy so much leverage over the mom and pops. A proper

MOE process levels the playing field…at no cost or risk to anyone.

Under the proposal, banks would extend money to help these

borrowers and the facility would provide a Treasury Department

guarantee that banks are repaid. The funding would come from

a $454 billion pot set aside for distressed businesses in the

earlier stimulus bill.

MD: You’ve got to love that phrase “banks would extend money”. Folks. The banks don’t have money. They have a 10x leverage privilege. A proper MOE process makes that privilege unnecessary. Let the banks continue to exist if they want to. But the 10x privilege is an anachronism.

Richard Pietrafesa owns three hotels on the East Coast

that were financed with CMBS loans. They have recently had occupancy

of around 50% or less, which doesn’t bring in enough revenue to

make mortgage payments, he said.

MD: And here is a case where we have to ask: where does the money come from? When you buy a house over time you can securely make that money creating promise. You know what you expect to make and purchase a house accordingly. But if the income is interrupted its your problem to find a replacement for it.

But Pietrafesa has no way of replacing his interruption. Such deals are heavily leveraged (OPM…other people’s money). He couldn’t get the MOE process to allow this money creating trade in the first place. He would have to rely on forming a collective to get his hotel deal done. And if the collective fails, well, as individuals in the collective, they have an incentive to keep it from failing or they lose their share. The MOE process may allow their trading promise to Pietrafesa…but would not allow Pietrafesa’s promise to the owner of the hotel he purchased. For example, just like buying a house with time payments, they could actuarially show they could buy a piece of a hotel with time payments…and be responsible if it fails.

He said he is now two months behind on payments for one

of his properties, a Fairfield Inn & Suites in Charleston, S.C.

He has money set aside in a separate reserve, he said, but his

special servicer hasn’t allowed him to access it to make debt

payments.

MD: Here we have the domino effect. He’s paying a “special servicer” to cover this risk. He’s buying insurance. It’s an actuarial problem. And insurance companies are the ultimate leveragor. In insurance CLAIMs = PREMIUMS. The money is made on the investment income. But with a real MOE process which guarantees zero INFLATION, investment income can’t benefit from the leverage INFLATION gives. The insurance business becomes a risk mitigation business with a proper MOE process…as it should be.

“It’s like a debtor’s prison,” Mr. Pietrafesa

said.

MD: An MOE process does not have a provision for penalizing. It only has a provision for naturally ostracizing. Pietrafesa would have to pay INTEREST if he DEFAULTs and tries to create money again. And he has to make up that DEFAULT to become a responsible money creating trader again. It’s the natural negative feedback stabilizing loop of the process.

Those magic words, it would appear, is all one needs to say these

days to get a government and/or Fed-sanctioned bailout. Because in a

world taken over by zombies, failure is no longer an option.

MD: These days are no different than other days. In the

olden days the zombies were taken over by the Rothschilds…through

their J.P.Morgan agency. It was and is a protection racket…just

like the mafia runs. A proper MOE process removes the leverage and

drives them out of business…kind of like legalizing drugs drives

those dealers them out of that business. Ultimately, people need to

be responsible for their own stupidity…but not for the stupidity

of others.

While any struggling commercial borrower that was previously in

good financial standing would be eligible to apply for funds to

cover mortgage payments, the facility is designed specifically for

CMBS borrowers.

MD: Thus, the leverage is in the ability to lobby. Such

advantage needs to be eliminated…in a very natural, not

legislative, manner. A proper MOE process goes far in enabling that.

It gets better, because not only are taxpayers ultimately on the

hook via the various Fed-Treasury JVs that will fund these programs,

but the new money will by default be junior to existing insolvent

debt. As the Journal explains, “many of these borrowers have

provisions in their initial loan documents that forbid them from

taking on more debt without additional approval from their

servicers. The proposed facility would instead structure the

cash infusions as preferred equity, which isn’t subject to the

debt restrictions.“

MD: The taxpayers are not on the hook. Our current

process with no stabilizing negative feedback will just keep

escalating until it blows itself up. Then most people (not in the

inner circle with advance warning) lose; it resets; and starts all

over again…with the insiders picking up the pieces for pennies on

the dollar. We now pay over 3/4ths of what we earn to governments.

Where does communism begin? Where does slavery begin?. It’s not a

good system folks. We’ve been duped. And praising the constitution

and wrapping ourselves in the flag is not going to fix it. It was

broken when it was installed…the anti-federalists got it right but

lost the argument.

Yes, it’s also means that the new capital is JUNIOR

to the debt, which means that if there is another economic downturn,

the taxpayer funds get wiped out first while the pre-existing debt –

the debt which was unreapayble to begin with – will remain on the

books!

MD: When a building collapses, it’s kind of immaterial

whether the lower floors or the upper floors collapse first. When

this calamity happens, the dirt this house of cards stands on is the

only thing of value.

Perhaps sensing the shitstorm that this proposal would create,

the WSJ admits that “the preferred equity would be considered

junior to other debt but must be repaid with interest before the

property owner can pull money out of the business.”

MD: And this is how we get 40,000 new laws every year.

They start with a bad process (i.e. principles diluted by laws) and

are stuck with a huge maintenance problem.

What was left completely unsaid is that the existing impaired

CMBS debt will instantly become money good thanks to the

junior capital infusion from – drumroll – idiot taxpayers who won’t

even understand what is going on.

MD: “will instantly become money”: Let’s examine

this. We know what money is. So somehow he’s saying that some trader

instantly makes a promise spanning time and space here. Who’s the

trader, the taxpayer? Well that’s no different than what we have now

with government doing perpetual rollovers of their trading promises.

That’s not money creation. That’s counterfeiting. We already know

that.

How did this ridiculously audacious proposal come to being? Well,

Taylor led a bipartisan group of more than 100 lawmakers who last

month signed a letter asking the Federal Reserve and Treasury to

come up with a solution for the CMBS issues. Treasury Secretary

Steven Mnuchin and Fed Chairman Jerome Powell have indicated that

this may be an issue best addressed by Congress.

MD: “asking the Federal Reserve and Treasury to come

up with a solution”? They’re the problem. Institute a proper MOE

process and we drive out the problem. That allows us to address

issues in a “proper” context rather than an “opportunist”

context.

In other words, while the Fed will be providing the special

purpose bailout vehicle, it is ultimately a decision for Congress

whether to bail out thousands of insolvent hotels and malls.

MD: The malls have no future. They are the buggy whip

of a previous era. They need to be plowed under and reseeded. But

the hotels are viable. They are just suspended in time. If they’re

collectively owned they are the responsibility of the members of the

collective. They are suspended in time. They are not failing. And

suspension carries no cost in this instance except maintenance.

Remember, with a propper MOE process, money has zero time value.

Failure? That’s something else again. It all get’s back to the

individual traders’ responsibility and recourse. A proper MOE

process should allow small traders to create money to tide

themselves over the temporary situation. It should not support large

highly leveraged traders to do so. It’s an actuarial problem.

And if some in the industry have warned that an attempt to rescue

the CMBS market would disproportionately benefit a handful of large

real-estate owners, rather than small-business owners, it is because

they are precisely right: roughly 80% of CMBS debt is held by a

handful of funds who will be the ultimate beneficiaries of this

unprecedented bailout; funds which have spent a lot of money

lobbying Messrs Taylor and Lawson.

MD: Handful of “funds”. What is a fund but a

collective… where the manager gets the gains and the participants

get the losses. People who buy into a fund roll their own dice. When

the fund is a pension fund, only the pensioner should have control.

With perpetual zero inflation, placing their pension under a rock is

a viable solution.

Of course, none of this will

be revealed and instead the talking points will focus on reaching the

dumbest common denominator. Taylor said the legislation is focused on

– what else – saving jobs. What he didn’t say is that each job that

is saved will end up getting lost just months later, and meanwhile it

will cost millions of dollars “per job” just to make sure

that the billionaires who hold the CMBS debt – such as Tom Barrack

who recently

urged a margin call moratorium in the CMBS market – come out

whole.

MD: Saving jobs “is” the issue. These workers are

suspended in time. It’s their responsibility to provide for

themselves. They can do this by creating money to tide themselves

over (say for a year or two if necessary). A proper MOE process could

actuarially support this money creation.

Say we have the maitre-d of the hotel restaurant. It’s

pragmatic for him to span this interruption and go back to work as if

nothing happened. So he creates a time and space spanning money

creating promise. He creates two years of normal income to be paid

back 1/100th monthly. The payback begins two years hence and proceeds

100 months. When he goes back to work he begins paying back,

essentially cutting his own salary a manageable amount. And while

suspended, he can put up dry-wall and make some pin money.

For the bar-back it’s a little different. He may make a money

creating promise covering 3 months income to be paid back monthly

beginning in three months over a two year span. And he immediately

goes looking for a replacement job…maybe putting up dry-wall. His

job is not his “career”.

“This started with employees in my district calling and saying

‘I lost my job’,” Taylor said, clearly hoping that he is dealing

with absolute idiots.

MD: An idiot institutes processes that have built in

domino effect.

And while it is unclear if this bill will pass – at this point

there is literally money flying out of helicopters and the US deficit

is exploding by hundreds of billions every month so who really gives

a shit if a few more billionaires are bailed out by taxpayers –

should this happen, well readers may want to close out the trade we

called the “The

Next Big Short“, namely CMBX 9, whose outlier exposure to

hotels which had emerged as the most impacted sector from the

pandemic.

MD: The money flying out of the helicopters is

counterfeit. It will go directly to producing INFLATION. It will only

create taxes to the extent the money-changers demand their tribute

payments…that’s where “all” taxes go.

With a proper MOE process the domino effect is mitigated; a

natural stabilizing negative feedback mechanism prevails; and a

pragmatic self controlled recovery is instituted. Remember. When you

have a government solution to a problem, you just have the same

problem multiplied and are still looking for a solution.

Alternatively, those who wish to piggyback on this latest

egregious abuse of taxpayer funds, this crucifxion of capitalism and

latest glorification of moral hazard, and make some cash in the

process should do the opposite of the “Next Big Short”

and buy up the BBB- (or any other deeply impaired) tranche of the

CMBX Series 9, which will quickly soar to par if this bailout is ever

voted through.

MD: And the real character of so-called “investors”

is revealed and amplified. Without a proper MOE process, money is the

chips in an opportunist, privileged casino called capitalism.

Traderism is where real money lives.

MD: So here we have another good example where a proper MOE process doesn’t “treat” a problem; rather it anticipates it and prevents its effect.

[MD] The provocative (and ill-informed) title of this article begs some annotation. At Money Delusions, it is obvious and provable to us that not only is money debt, it always has been and it always will be. Money is a promise to complete a trade over time and space … and a promise is obviously a debt.

So let’s see what this moron Shorty Dawkins has to say on the subject.

When the Federal Reserve System was established in 1913, it transferred the power of the US Treasury vis-a-vis the creation of money, into the hands of the Federal Reserve. The Fed creates money out of thin air and loans it to the US Treasury in the form of interest bearing debt instruments. Thus, the money of the US is based on debt. With over $20 trillion in Federal debt, the interest paid on that debt in fiscal year 2018 is estimated to be $310 billion. That’s no small amount!

[MD] What was actually transferred was the propensity to counterfeit. Neither the Treasury nor the Fed create money. Only traders create money. You can’t give a single example where money is created that a trader is not involved and did not initiate it … that is, unless it is created by counterfeiting. And regarding the interest paid: If the process is a “real” process, the interest paid is exactly equal to the defaults experienced. Why don’t we ever see these people quoting defaults experienced?

What if money were not created out of debt? Is that possible? Sure. If the powers of the Federal Reserve were taken back by the US Treasury, it would be possible to spend money into existence, rather than into existence as debt.

[MD] Can he say anything more stupid? “Spend money into existence?” And if not into debt, into “existence” as what? Kind of left something out didn’t you Shorty?

The Federal budget for 2018 is: Total expenditures: $4.094 trillion. The total estimated revenue: $3.654 trillion. This leaves a projected deficit of $440 billion. Since the deficit must, under the current Federal Reserve System, be borrowed from them, at interest. Thus the deficit grows and next year’s interest payment will increase.

[MD] If a “real” money process were in existence, the government creating this debt would only do it once … and then be excluded from the marketplace as a trader. Deadbeat traders are automatically excluded when their interest load (due to their propensity to default) comes to equal the trading promises they seek to have certified.

However, if the US Treasury were to create the money, it could simply spend it into existence to cover the deficit. No interest need be paid! As the previous debt interests of the Federal Reserve came due, they could be paid off by money created by the US Treasury in the same manner. Eventually, the entire debt could be paid off in this manner.

[MD] “No interest need be paid” is true only for responsible traders. Governments are not responsible traders. In fact they never deliver. They just roll over their trading promises … and that is default … and purposeful default is counterfeiting! I’ll bet Shorty has a perpetual motion machine he would like to show us as well.

Beware! This is not free money!

[MD] In a “real” money process, money is “always in free supply”. That’s not to say it is “free money”. Rather, it says money “never” restricts the trading intentions of responsible traders who create it. They “always” deliver on their promises.

It may sound like free money, but it isn’t. As more money is spent into creation, inflation takes its toll. The true definition of inflation is the increase of the money supply above the value of goods and services produced. When the money supply increases faster than the value of production, there is more money chasing fewer goods and prices rise, as the value of the money decreases. If too many dollars are created, the value of the dollar decreases. Under the Federal Reserve System the value of the dollar has decreased by 98%, meaning that something bought in 1913 for $1 would now cost $98, disregarding any increases in productivity of a particular product.

[MD] In a “real” money process, inflation takes no toll … it is guaranteed to be perpetually zero. The true definition of inflation is the amount that supply of the money itself exceeds the demand for the money … and we know in a “real” money process, supply and demand for the money itself is perpetually in perfect balance.

The fraud of the Federal Reserve System is that it was sold as a means of preserving the value of the dollar and that it would prevent crashes in the economy. Both of these selling points have not proven accurate. There have been multiple crashes of the economy since the Fed was established, including the Great Depression.

Ideally, the US dollar should be backed by gold and silver, or some tangible item, but that discussion is for later. First things first. We must End the Fed.

[MD] Gold and silver and any other commodity cannot maintain perpetual perfect balance of supply and demand for themselves. So obviously they are useless as money. Thus, your later discussion can be suspended. You don’t know what your talking about Shorty … and that is easy to prove.

The Federal Reserve has never been good for the public. It has only been good for the big banks. They love it, because it makes them money. Who pays? We do. We are slaves to debt. Isn’t it time to eliminate the Fed and turn its powers over to the US Treasury, where it belongs?

[MD] Even the blind squirrel occasionally finds an acorn. Congratulations Shorty. Governments are created by the money changers … always have been, always will be … unless we can effect iterative secession and have it our way in our own space.

Have you enjoyed the post ?

[MD] It brought some amusement. It was easy fodder for illustrating how stupid the gold bugs are.

I am a writer of novels, currently living in the woods of Montana. My 5 novels can be seen here: https://oathkeepers.org/my-5-books-shorty-dawkins/

[MD] Frightening. Hopefully that doesn’t lead to the natural conclusion that there are people reading your novels. Stupidity is already widespread enough don’t you think Shorty?

{kind=link}

{kind=link}

{kind=link}