Ethereum Co-Founder Responds To Sweden’s Cashless-Society Rethink

MD: We never know what we’re going to get into with these “cyber money” articles. Looks like someone’s having reservations about how well it works. And is it correct to refer to it as “cashless”?

If I have a $100 bill and I take it to a gas station and trade it for a tank of gas and $50 in change that’s a “cash” transaction. The gas station now has a $100 bill in their cash register. And they have one less $50 bill there. Further, they have $50 less gas in their buried tank. And I have $50 worth of gas in my truck. And I have a $50 bill in my wallet where I once had a $100 bill.

Now, does anything change if I give the gas station a debit card… or a credit card… or the gas station’s own branded credit card? It’s all just accounting. It’s all just moving “cash” around. Or is it? There’s an important distinction between a “debit” card and a “credit” card.

With a “debit” card, you have something keeping track of “cash you have”. With a “credit” card you have something keeping track of “cash you create”… cash you “don’t” have… cash you must return to complete your promise. Cash you have is an “in process promise to complete a trade spanning time and space” You don’t know who made that promise. You do know it wasn’t you. You are using it as the most common object in simple barter exchange.

But what about the “credit” card. It’s about “cash you create”. And when you “create” cash, “you” are making the “promise to complete a trade spanning time and space.” And it is “you” who must deliver on that promise. But it’s still cash. It’s still money. But it’s not money “you” have. It’s money the creator of the credit card has. These are terms referring to the same thing. At the end of the month you “pay” off your credit card… usually by making a deposit in an account. And what do you deposit in the account? Probably a check from your employer.

And that check from your employer… what is that? It’s a token that will eventually take cash out of his account and transfers it into your account. That is now a principal function of a bank. It’s a banking function that they charge you for.

In the beginning, it was no function of a bank at all. The function of a bank was to keep people from stealing your valuables… whether in a safe deposit box, or in their vault holding gold and silver… things people “believe” to have value. And you paid the bank for that safe keeping. And in the end, the bank occasionally lost your gold and silver… and said “sorry… it’s gone!”

So, are we clear what “cash” is? Are we clear that the term “cashless” is meaningless?

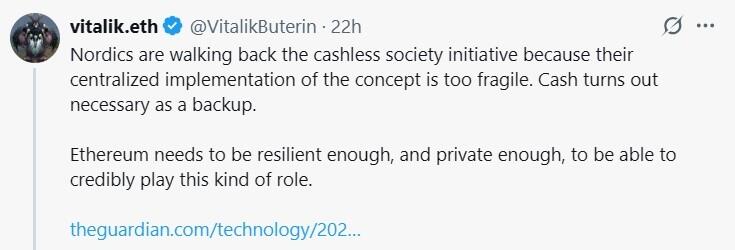

As Sweden reconsiders its push toward a cashless society, Ethereum co-founder Vitalik Buterin highlighted the fragility of centralized digital payments and the opportunity presented by decentralized payment alternatives.

MD: “Fragility of centralized digital payments”. I think this is the “thesis statement” of this article. Let’s keep it in mind as we proceed.

In recent years, Sweden has led the charge toward a cashless future, with digital payment platforms becoming widespread. However, as concerns over cyber-threats, civil defense and instability have emerged, Swedish authorities are now actively encouraging citizens to keep some cash.

MD: What he’s really saying is “keep your cash as stuff rather than as numbers in a ledger”. And is a token representing numbers in a ledger stuff? Well, we’re seeing how confused these geniuses are, aren’t we.

Buterin noted the reversal illustrates that while centralized solutions may be efficient, they may not be reliable during times of crisis.

MD: If tokens (i.e. stuff) representing numbers in a ledger is not a “centralized solution”, then what is it? Would it be better to call it a “universal” solution? I think so.

“Nordics are walking back the cashless society initiative because their centralized implementation of the concept is too fragile,” Buterin wrote, citing a March 16 article by The Guardian. “Cash turns out necessary as a backup.”

MD: Ethereum claims to be money. It falsely assumes that by keeping track of “pure waste” of electricity, money is created. And Ethereum is the ledger that keeps track of that. It’s obviously silly… but that’s the concept. They call it “proof of work”. And now they’re suggesting that that number in the ledger is actually worthless… even though it stands for actual waste. And as a backup, you should keep some “cash”. Now tell me, where did the cash come from?

A former central bank official predicted in 2018 that Sweden would be cashless after seven years. In 2025, the prediction mostly held, with only one in 10 transactions in the country being done in cash, according to The Guardian.

MD: This “one in 10” is probably a made up statistic. Do you really think it’s somebody’s job to keep track of so-called “cash” transactions as distinct from “non-cash” transactions?

Still, while the Nordic country was an early adopter of digital payments, its government published a brochure encouraging citizens to keep a week’s worth of cash in case of war or crisis. Sweden’s reconsideration has revealed the issue of centralized digital payment infrastructure remaining reliable in times of instability, Buterin suggested.

MD: “… in case of war or crisis…” This suggests that this ethereum stuff disappears or is otherwise inaccessible in some situations. And this isn’t true of what they’re calling cash… which is presumably “currency” and “coin”… tokens that don’t disappear for some reason. That suggests, if we are to have a truly cashless society, we need an indelible record. Could an SD card be made to act like an indelible record? It could if it could be encrypted with a password that only the owner knows. An invention is needed here.

Buterin said Ethereum can be a decentralized financial fallback in times of crisis. “Ethereum needs to be resilient enough, and private enough, to be able to credibly play this kind of role,” Buterin said.

MD: Seems to me what we need is a process that moves numbers from one ledger to another ledger with no central authority. That’s what needs to be invented.

When asked if fully offline zero-knowledge technology-secured private transfers were close to practical implementation, Buterin said the tech know-how is already there, but there are still limitations:

“We basically know how to do it, but with the limitation that any solution depends on trusted hardware and/or post hoc enforcement against double-spenders.”

MD: So basically what is it he thinks he knows how to do then?

Crypto payments exec thinks crypto won’t replace fiat

MD: Oh please! What’s with this “fiat”? See how their improper use of terms just throws a wrench in the works?

While crypto payment solutions are becoming more common, Mercuryo co-founder and CEO Petr Kozyakov has said that crypto will not replace fiat.

MD: And did his say that, somehow knowing everybody knew what he was talking about? Does everybody know what this “fiat” term means?

Kozyakov told Cointelegraph in an interview that crypto payments are seeing an increase in demand and adoption.

However, the executive said that instead of cryptocurrencies fully replacing fiat money as a payment method, the two payment options will coexist.

MD: Is that different than saying “cash” and “currency” and “checks” and “credit cards” and “debit cards” and ATM machines should coexist?

Kozyakov told Cointelegraph that people will use crypto when it’s easier and more practical.1,1375

MD: What makes it “hard” and “less practical”? Are these people of value? Are they paid (i.e. do other people give money to them for putting out this nonsense). How advanced must a society become to be so confused about value?

Marathon Digital Holdings, Inc. is a digital asset technology company, which engages in mining cryptocurrencies, with a focus on the blockchain ecosystem and the generation of digital assets. The company was founded on February 23, 2010 and is headquartered in Las Vegas, NV.[1]

MD: So… we know they ‘re clueless about money. And located in Las Vegas, NV… maybe know something about gambling… which is what Bitcoin is… betting on the sure thing until the music stops.

The company was formerly known as Marathon Patent Group and was the patent holding company that is the parent of Uniloc, allegedly a patent troll company.[2][3] Marathon purchased patents related to encryption in the 2010s[citation needed] and in 2021 it was known for its purchases of bitcoin[4] and bitcoin mining equipment[5] and a joint venture to use 37 MW from the Hardin Generating Station Montana coal plant to power an adjacently-constructed Marathon bitcoin data center.[6]

MD: So they’re leveraging leverage. A “patent holding company”. What’s not to love about the patent system. If there was anything that should be repealed, it’s definitely that part of the Constitution. But it is an open lesson into creative abuse of any system. These guys give patents value… when 99% of them clearly have no value, even if they do work. Looks like they actually got into the electricity wasting business which “is” Bitcoin mining. Why are they using coal in Montana? Has all the water in the Columbia River Gorge already been wasted?

The company changed its name to Marathon Digital Holdings, effective March 1, 2021. Its chief executive officer is Fred Thiel.[7]

MD: Fred Thiel. Wonder if he’s any relation to Peter Thiel… the claimed co-inventor of PayPal with Elon Musk… a trivial application to write BTW. We’ll look into that. Here’s what Wikipedia has to say about Thiel (… and doesn’t seem to have anything to do with Peter Thiel).

Fred Thiel

Born

1960

Nationality

American

Occupation

Businessman

Board member of

Marathon Digital Holdings NoCell Technologies Oden Technologies Sequent Software OptConnect Inc. Gatekeeper Systems

Fred Thiel (born 1960) is an American business executive and the current CEO of Thiel Advisors and Marathon Digital Holdings.[1][2] Thiel is the former CEO of GameSpy, Local Corporation, and Lantronix.

MD: How’s that for some big names and strong background?

Thiel serves as past chairman of the board of the Young Presidents’ Organization‘s technology network and is chairman of the Fintech subnetwork. He also serves on the boards of several other companies including Oden Technologies, OptConnect, Gatekeeper Systems, and Sequent Software.

Thiel was vice president and general manager of the business storage unit of CMD Technology in 1997.[3] From 1998 to 2002 Thiel was the CEO of Lantronix,[4] where he doubled the company’s revenue growth and led to its initial public offering in 2000.[5] Thiel was the CEO of GameSpy from 2003 to 2004 before GameSpy merged with IGN.[6] Thiel was the managing partner of the software group at Triton Pacific Capital Partners from 2007 to 2012.[7]

Thiel met Heath Clark, founder and CEO of Local Corporation though the Young Presidents’ Organization,[5] and joined Local Corporation’s board of directors in January 2013.[8] He became the chairman of the board of Local Corporation in January 2014, and CEO in May 2014 following Clark’s resignation due to health reasons.[9] Thiel was CEO until 2015, and was responsible for Local Corporation’s partnership with FraudLogix to prevent advertising fraud.[10]

MD: Two years at Local. And into fraud. The plot thickens.

Thiel has headed Thiel Advisors, an advisory firm, since 2013.[11] Through Thiel Advisors, Thiel advises organizations such as EQT Partners and Graham Partners, their portfolio companies, and various mid-sized companies on value creation strategies. Thiel was appointed to the board of directors of Marathon Patent Group in April 2018[12] and became CEO of Marathon Digital Holdings in April 2021[13]

MD: “Value Creation Strategies”: Money “is” value creation. I’ll bet Thiel has no clue what money is. But look… we still have no clue about any value proposition yet. How can that be?

MD: I took an executive class at MIT once. Didn’t know that was a big deal. Well, looks like another dead end. I wonder what ChatGPT knows about this?

MD: What can you tell me about Fred Thiel?

ChatGPT

As of my last update in September 2021, Fred Thiel is a business executive and entrepreneur. However, please note that my information might not be up to date, and developments may have occurred after my last update.

At the time of my knowledge cutoff, Fred Thiel was known for his involvement in the technology and cybersecurity sectors. He served as the CEO of various cybersecurity companies and had extensive experience in managing and advising technology-focused organizations.

If you are looking for more recent and accurate information about Fred Thiel, I recommend conducting an online search or checking reliable news sources for the latest updates.

MD: How about Marathon Digital HoldingsChatGPT

As of my last update in September 2021, Marathon Digital Holdings (formerly known as Marathon Patent Group) is a digital asset technology company focused on cryptocurrency mining. Please note that my information might be outdated, and developments may have occurred after my last update.

At that time, Marathon Digital Holdings was primarily engaged in mining Bitcoin and had been working to expand its mining operations. They aimed to leverage their expertise in blockchain technology and data center operations to become a significant player in the Bitcoin mining industry.

It’s important to remember that the cryptocurrency space is highly dynamic and can experience rapid changes. For the most current and accurate information about Marathon Digital Holdings, I recommend checking their official website, recent news articles, or financial reports.

MD: Well, we come up empty again. Let’s look further for something concrete. Well, they have a very pretty website. That’s usually a negative for me. Let’s dissect it.

MD: Looks like they’re well lawyered up. You need to acknowledge this disclaimer to see inside their website:

Marathon Digital Holdings (“Marathon,” “MARA”) does not offer financial services, nor direct investment opportunities to the general public. We have no consumer facing products or services. We will never ask you to send money or open an account. Please remain vigilant and be wary of bad actors who may be misappropriating our brand and corporate identity.

MD: What does it mean when the boogeyman cautions you to watch out for the boogeyman?

About Us

Marathon Digital Holdings is one of the largest, most energy efficient, and most technologically advanced Bitcoin mining companies, as well as one of the largest holders of Bitcoin (“BTC”) among publicly traded companies in North America.

We differentiate by investing in the most advanced technologies and leveraging innovative techniques to convert energy into economic value while helping keep Bitcoin’s ledger up to date and secure, one block at a time.

MD: How can they consider themselves energy efficient when Bitcoin is a “pure waste of energy”. A “real money process” costs virtually nothing to operate. There is no mining involved. Good thing they’re doing it one block at a time… cause that’s how blockchain (or even chains without blocks) works.

Operations

Bitcoin is decentralized, and so are we. We use various strategies and business models, including outsourcing to third-party hosting providers or hosting our own operations, to maintain a diversified portfolio of Bitcoin mining sites in multiple states and countries.

MD: Wow… how innovative. These days with so many server farms out there this is pretty easy to do.

Investors

Marathon Digital Holdings is a publicly traded company (NASDAQ: MARA). Our investor relations website includes detailed information on our financial performance, our latest corporate updates, SEC filings, and more.

MD: Has anyone ever seen one of these “investor” thingies? We’ll go a little further and then see if we can find their annual report and dissect that.

Partner With Marathon

We work alongside companies, municipalities, and institutions that have stranded power, expertise in energy and microgrids, cutting edge Bitcoin mining technologies, and a keen interest in researching or supporting Bitcoin. We offer our partners access to our unique expertise in building and scaling Bitcoin mining operations as well as the opportunity to help support the Bitcoin network.

MD: “Stranded power”? That’s a new one. “Microgrids”? That’s another new one. “Keen interest in researching or supporting Bitcoin”? Why is that? OK, so that’s their shingle. Let’s go in. They call it “Getting started”. They’ve got five more bullet points. I’ll scan them, but I think my assignment is to look at their annual report… so I need to move along

Funding & Mentorship

We support builders. We invest in smart people, who are passionate about leveraging technology to solve Bitcoin’s and the Bitcoin mining industry’s largest problem.

MD: Whoops. That eliminates me!

Company Profile

Marathon Digital Holdings (NASDAQ: MARA) is one of the largest, most agile, and most sustainably operated Bitcoin miners in North America. The company converts energy into economic value by processing Bitcoin transactions, creating newly minted Bitcoin (“BTC”), and keeping Bitcoin’s distributed ledger up to date and secure.

MD: Address is now in Ft. Lauderdale, Florida, not Las Vegas. Most Florida cons are operated over on the Tampa/St. Pete side. They say they process Bitcoin transactions. That means they know how to add and subtract. They create new Bitcoins (waste energy) and they keep Bitcoin’s distributed ledger up to date and secure (now that’s huge, because the whole Bitcoin concept says nobody can do that… because everybody does that. It’s kind of like the internet DNS). Before we look at their financials, we’ll look at the operations… it’s good to know what somebody claims to do.

Diversified Portfolio Approach to Bitcoin Mining

Each Bitcoin mining deployment comes with its own set of constraints, and each requires a curated approach. We adapt accordingly. Overtime, we have used different strategies and structures to build a portfolio of Bitcoin mining operations that is designed to diversify risk across our organization.

MD: Says they crank out 23 EH/s. Anybody know what an EH is? We’re about to find out. Poor Google. It thinks it’s about “Environment Health and Safety”. But gotta love ChatGPT. Here’s what she says:

In the context of Bitcoin, EH/s stands for “exahashes per second.” It is a unit used to measure the total combined computing power of the Bitcoin network, specifically in terms of how many cryptographic calculations (hashes) it can perform in one second.

Bitcoin mining is the process by which new transactions are added to the blockchain and new bitcoins are created. It involves solving complex mathematical puzzles, known as cryptographic hash functions, which require significant computational power. Miners compete to find the correct solution to the puzzle, and the first one to do so gets to add a new block to the blockchain and is rewarded with newly minted bitcoins and transaction fees.

The network’s total hash rate is the sum of all the miners’ computing power, and it is measured in EH/s. As technology advances and more powerful mining hardware is introduced, the total hash rate of the Bitcoin network increases. A higher hash rate implies a more secure and robust network, as it becomes increasingly difficult for any single entity or group to control the majority of the network’s computing power (known as a 51% attack).

MD: For those of you who aren’t into the really big numbers game, an exa is a quadrillion gigas. If you started right now, you probably wouldn’t be there by lunch tomorrow. ChatGPT does pretty good, don’t you think? It’s not intelligent at all, but it sure has a good memory. MARA enumerates 6 sites where they do this wasting… and that is among “others”. It seems they are concerned with somebody getting more that 51% of the hashes. Trust me folks, you can’t waste enough energy in the whole universe… and all its black and grey and pink holes… to do that. I guess we know enough. We can now see how much money they claim to be making.

MD: I have obtained their earnings report dated May , 2023. Anybody can find their numbers. Here’s them applying creativity:

Q1, we grew our energized hash rate 64% from 7.0 exahashes to 11.5 exahashes. By growing our hash rate faster than the rest of the network and improving our uptime, we also increased our bitcoin production. We produced a record 2,195 bitcoin during the first three months of this year, which is a 74% increase from the prior year.

MD: If they’re growing at 74% a year they’re doing better than the banking scam. The bank scam grows at just 40% a year. But I don’t think that’s fast enough to corner the Bitcoin market. They either have to quietly do that, or be among the first to bail out… and looks like they’ll have lots of bailing to do.

“In addition to our energized progress, we also improved our financial position during the quarter. We increased our cash position by $12 million, reduced our debt by $50 million, and increased our unrestricted bitcoin holdings by 3,132 bitcoin after we prepaid our term loan and terminated our credit facilities with Silvergate Bank.

MD: What in the world is an “unrestricted bitcoin holding?”. Who’s restricting? Takes these financial thieves almost no time at all to make something simple ridiculously complicated.

We exited the quarter with approximately $124.9 million in unrestricted cash and cash equivalents and 11,466 bitcoin, the market value of which was approximately $326.5 million on March 31.

MD: If Bitcoin is such magic, why in the world would they have cash and cash equivalents? Buy Bitcoin with it… mui pronto.

“With more hash rate coming online in the months ahead, Marathon remains on track to reach our 23 exahash goal near the middle of this year. We remain optimistic that we can achieve our primary growth targets and establish Marathon as one of the largest, most energy efficient, and most technologically advanced Bitcoin mining operations globally.

MD: I asked ChatGPT who generates the most EH/s.

ChatGPT:

As mentioned earlier, the distribution of mining power in the Bitcoin network can change over time due to various factors. Some of the largest and most well-known mining pools in the past have been companies like Antpool, F2Pool, BTC.com, and Poolin. However, it’s important to note that the mining landscape is dynamic, and other pools or entities could have risen to prominence since my last knowledge update in September 2021.

To find the current information on the entities generating the greatest number of EH/s or the distribution of hash rate in the Bitcoin network, you can refer to real-time data provided by reputable sources that track the mining pools and hash rate distribution. Websites like Blockchain.com, BTC.com, and other blockchain explorers often provide such data. Additionally, specialized cryptocurrency news websites and forums might have updated information on this topic.

MD: Let’s see what Blockchain.com can tell us. It appears the current hash rate is 332.95 EH/s (https://www.coinwarz.com/mining/bitcoin/hashrate-chart). That’s more than 10 times MARA’s goal. I groped around a little while to see who the other big players were. I didn’t find what I was looking for… and of course I’m not interested in wasting more time on the subject. Would I invest in MARA? Stupid is as stupid does. I could have bought Bitcoin at $0.10. Instead I tried to explain to Andreson why it wasn’t, and never would be, money. Now he’s a gizzionaire… and I’m high, dry, looking for a ball player at the carnival.

Thanks for watching. Hit that “like” and “subscribe”. It really helps us here.

Marathon Digital Holdings Inc. (NASDAQ:MARA) price on Wednesday, July 19, rose 4.64% above its previous day’s close as an upside momentum from buyers pushed the stock’s value to $17.59.

MD: I presume we’re supposed to know about MARA already (i.e. COIK: Clear Only If Known). Let’s see how far we can get before we have to do our homework. Reaching into my pocket I have the $0.59. The $17 may be more problematic.

A look at the stock’s price movement, the close in the last trading session was $16.81. Turning to its 52-week performance, $19.88 and $3.11 were the 52-week high and 52-week low respectively. Overall, MARA moved 76.25% over the past month.

MD: I’m one of those gamblers that buys at $19.88 and sells at $3.11. I quit gambling long ago. Before I quit I even started betting against myself. I was still always wrong. Go figure.

The artificial intelligence (AI) revolution is already here. And it’s about to change everything we know about everything. According to Grand View Research, the global AI boom could grow from about $137 billion in 2022 to more than $1.81 trillion by 2030. And investors like you always want to get in on the hottest stocks of tomorrow. Here are five of the best ways to profit from the AI boom.

MD: Just like with money, everybody seems to be clueless about AI. You don’t get smart by contemplating your navel… or contemplating everybody else’s navel. They should call it AS… Artificial Stupidity. And there is more than enough RS (real stupidity) to go around.

Marathon Digital Holdings Inc.’s market cap currently stands at around $2.99 billion.

MD: Let’s see. $2.99B divided by $17.59… That means they’ve divided this fiction into 170 million pieces. Likely they’ve kept 50 million for themselves for which they paid nothing. And found other suckers to buy into their get rich scheme to the total tune of 120 million pieces. What’s not to love about leverage when it comes to finance.

Analysts project the company’s earnings per share (EPS) to be -$0.02, which has seen fiscal year 2023 EPS growth forecast to increase to $0.14 and about $0.49 for fiscal year 2024. Per the data, EPS growth is expected to be 104.50% for 2023 and 250.00% for the next financial year.

MD: Wow. The power of big numbers. Earning 2 cents a share… but times 120M shares, we’re talking real money… who said that, Everette Dirkson? And there are people out there that think “regulation” is the antidote for this, right? Wrong! It’s the enabler.

Analysts have a consensus estimate of $92.65 million for the company’s revenue for the quarter, with a low and high estimate of $78.29 million and $111.2 million respectively. The average forecast suggests up to a 271.80% growth in sales growth compared to quarterly growth in the same period last fiscal year. Wall Street analysts have also projected the company’s year-on-year revenue for 2023 to grow to $431.33 million, representing a 266.30% jump on that reported in the last financial year.

MD: It’s amazing we can be this far into this article and still be clueless about the “value proposition”. I guess everybody reading this already knows what’s going on here. We’re probably too dumb to be even reading this… let alone getting in on the game.

Revisions could be used as tool to get short term price movement insight, and for the company that in the past seven days was no upward and no downward review(s). Turning to the stock’s technical picture we see that short term indicators suggest on average that MARA is a 100% Buy. On the other hand, the stock is on average a 100% Buy as suggested by medium term indicators while long term indicators are putting the stock in 100% Buy category.

MD: A 100% Buy. What could possibly go wrong? We’ll reserve comment until we get to something of substance, ok?

6 analyst(s) have given their forecast ratings for the stock on a scale of 1.00-5.00 for a strong buy to strong sell recommendation. A total of 3 analyst(s) rate the stock as a Hold, 3 recommend MARA as a Buy and 0 give it an Overweight rating. Meanwhile, 0 analyst(s) rate the stock as Underweight and 0 say it is a Sell. As such, the average rating for the stock is Overweight which could provide an opportunity for investors keen on increasing their holdings of the company’s stock.

MARA’s current price about 17.67% and 50.35% off the 20-day and 50-day simple moving averages respectively. The Relative Strength Index (RSI, 14) currently prints 65.45, while 7-day volatility ratio is 9.73% and 10.73% in the 30-day chart. Further, Marathon Digital Holdings Inc. (MARA) has a beta value of 5.04, and an average true range (ATR) of 1.40. Analysts have given the company’s stock an average 52-week price target of $13.10, forecast between a low of $7.98 and high of $20.00. Looking at the price targets, the low is 54.63% off current price level while to achieve the yearly target high, price needs to move -13.7%. Nonetheless, investors will most likely welcome a 23.25% jump to $13.50 which is the analysts’ median price.

In the market, a comparison of Marathon Digital Holdings Inc. (MARA) and its peers suggest the former has performed considerably stronger. Data shows MARA’s intraday price has changed 4.64% in last session and 80.23% over the past year. Elsewhere, the overall performance for the S&P 500 and Dow Jones Industrial shows that the indexes are up 0.24% and 0.31% respectively in the last trading.

If we refocus on Marathon Digital Holdings Inc. (NASDAQ:MARA), historical trading data shows that trading volumes averaged 49.88 million over the past 10 days and 40.28 million over the past 3 months. The company’s latest data on shares outstanding shows there are 169.97 million shares.

The 0.20% of Marathon Digital Holdings Inc.’s shares are in the hands of company insiders while institutional holders own 37.50% of the company’s shares. Also important is the data on short interest which shows that short shares stood at 42.15 million on Jun 29, 2023, giving us a short ratio of 0.92. The data shows that as of Jun 29, 2023 short interest in Marathon Digital Holdings Inc. (MARA) stood at 24.80% of shares outstanding, with shares short falling to 43.09 million registered in May 30, 2023. Current price change has pushed the stock 414.33% YTD, which shows the potential for further growth is there. It is this reason that could see investor optimism for the MARA stock continues to rise going into the next quarter.

MD: Nope! We still have no clue what they do. Looks like we’ll have to find another article. This may not publish.

MD: I had this dialog with someone calling themselves IMissLiberty on substack. We love to dissect these comments. In this conversation she is IML. I am TM (which is the same as MD). Here’s our dissection.

IML: The value of things is based on what you are willing to pay for them.

TM: Correct… sort of. It’s determined by negotiation…and that takes two parties. Once created (by making a promise spanning time and space and certifying it) money serves as any other object in simple barter exchange [SBE]…until it is destroyed (on promise delivery). In the interim it’s just stuff…like gold or dollars or pork bellies…or bottled water.

IML: Money is for saving the value of work and cost you already paid to produce something you sell today, not today’s cost to mine more.

TM: Money once created serves as the most common object in any SBE.

IML: Further, an ounce of gold found in your great grandmother’s treasure box is worth the same as the one mined and refined today–even though the costs were completely different in dollars or in whatever currency the older ounce was made.

TM: An ounce of gold is not different than a cement block…or money (after creation and before destruction) . It’s simply an object of SBE. It doesn’t matter who created it, when they created, where they stored it, what they paid for it. It’s just stuff. It’s not money. It’s just a primtive substitute…and hasn’t served as money in my nearly 80 year life time.

IML: The mining cost sets a floor but it doesn’t control demand.

TM: Supply and demand for each object (as viewed by the traders for that particular trade) dictate the trade. It’s the “negotiation” stage of all trades…SBE or otherwise. The other two stages are “promise to deliver” and “delivery”…which in SBE in the “here and now” happen simultaneously.

IML: Supply and demand are both involved in the future price of something you earn today.

TM: The so-called “price” is the exchange rate for two objects in SBE. It is set by the traders in the “negotiation” phase of the trade. The future price is estimated by “self proclaimed artists…like appraisers”…and Black and Shoals…and manipulated by governments and banks…and other imagination figments like LIBOR. It’s always a figment of someone’s imagination. However, if we’re talking about money in a “real money process”, it is always in units of HUL’s (Hours of Unskilled Labor). This simplifies the trade by twice: Both parties now know the “real undisputed value” of one of the objects. (a) It is in perpetual free supply; (b) it is in perpetual perfect supply/demand balance; (c) it is free of external loads…like interest; (d) it has no time value…doesn’t gain of lose with time or over space; (e) it costs nothing to create or destroy; (f) and cannot be counterfeited. They are left to agreeing on the value of the other object in the SBE. Ask a HUL to take an hour to make a hole; measure the hole; you will “always” get the same size hole (other conditions being equal) in all time and space.

IML:One could buy gas and store it, but gas is too volatile to carry in one’s wallet and has a limited shelf life and thus lose value.

TM: True, but irrelevant when it comes to money. Gas is not and never will be money. It’s just stuff…an object of SBE.

IML: Gold and silver have a non-perishable advantage as a store of your past costs/work.

TM: So do cement blocks. They’re all just stuff. Cement blocks have outperformed gold and silver over the last five years. When traded for dollars, gold and silver have gone up and down…cement blocks have only gone up.

IML: If I babysat for an hour in 1966 and got paid in two quarters I could spend that 50 cents to buy two gallons of gas any time in the future, and maybe more as the cost of extracting gas gets more efficient–as long as the quarters were silver.

TM: Great choice of examples. I hired baby sitters in 1966. They were paid 6 quarters per hour (I think my wife paid them 2 quarters)…same as my summer job in 1962. If we had real money then I would have paid them one HUL per hour. It was SBE.

IML: If they weren’t silver (counterfeit, paper, digital) they would barely pay the gas tax.

TM: In 1964 I paid one quarter (containing silver) for one gallon of gas (SBE). In 1965 I traded one quarter (containing no silver) for one gallon of gas (SBE). It proved the quarter itself traded for the gas. What it was made of (i.e. its intrinsic value) played no role. It’s even more dramatic today. You pay 10+ quarters (containing zero silver…or 90% silver) for a gallon of gas. You’re foolish to trade the silver quarters because they trade for more value in a different context…e.g. in making photographic film. That’s how money works. And why commodity money doesn’t work. In the case of coin: (1)the cheaper you can make it; (2) the more durable you can make it; (3) the more precisely you can control its dimensions (ie. weight, diameter, thickness); (4) and the more difficult you can make counterfeiting…the better. But it’s still just stuff when it comes to SBE.

IML: “Compared to the dollar” a decaying rubber-band yardstick is no better at measuring carpet than a dollar price over time, except it will fail much sooner and be replaced with something more useful.

TM: And this is the same for any object of SBE. An 1848 ounce of gold was worth more than an 1850 ounce. Supply changed dramatically in those years. At the end of the 1800’s the value of gold and silver gyrated…until by law they claimed silver was not legal tender…only gold and so-called gold backed paper was legal tender (another government imagination figment). In 1973 the French were owed some huge amount of money…let’s say it was $1B. The USA claimed an ounce of gold could be purchased for $35. The French knew by experience it cost $70+ to trade (SBE) for an ounce of gold. The French said, keep your dollars USA. You agreed to settle the debt in gold and we’ll take the gold. Tilt went the so-called “lie” called the gold standard. Nixon didn’t cause the failure. He just could no longer lie about it as his predecessors had. If we were on a “real money process”, the units of the debt would have been HULs and guaranteed never to change their value over time and space. Such fictions as gold stability have existed over all time and space.

An interesting exercise when comparing and contrasting two competing choices. If one of the choices is current practice and the other one is a claimed improvement, reverse their positions. Assume the new choice is the current practice, and vice versa. Now which one is harder to sell? This technique removes the inertial advantage all current practice has. It illustrates dramatically how ridiculous most “conservative” practices are. Electric cars vs ICE (Internal Combustion Engine) cars is a good case to practice on.

IML: If 1913 had been gold instead of a central bank, the income tax would still only tax the top 1% as promised, and it would be enough for peace and prosperity, but not enough for war.

TM: This is the Achilles heel of all government controlled money. Governments collect taxes to pay interest to the money changers who institute them. Governments sustain themselves through counterfeiting of money they claim to control. Central Banks are figments of the money changers imagination forced upon governments. They need them for another figment of their imagination…that being “reserves”. In a “real money process” there are no reserves. No one has to put their savings in a bank for the bank to loan out ten times that savings at a 4% spread (i.e.40% which doubles in less than 2 years) . And thus there is no such thing as a “run on the bank”. All trades are completely separate and isolated.

This is an interesting definition of a capitalist…i.e. two years. They create a bank; capitalize it; accept deposits; loan out ten times the deposits at 4% spread; double their money in 2 years; take 1/2 off the table removing all their original risk; and wallah…look mom, I’m a capitalist. What’s not to love about capitalism.

IML: The miners and refiners produce more when the price offered is higher than the cost of production. They stop when they are not offered enough, and then the supply drops. If they are hungry, they will produce enough for food or for dollars for food–it’s a market price.

TM: You can say the same for farmers growing corn or raising pigs. They’re just stuff in SBE.

IML: There is always demand for metals. Try to imagine life without them.

TM: Try to imagine life without food…or without water where it doesn’t rain much. Both are just stuff in SBE. In the case of rain it is genuinely free. In the case of food…not so much. And in times of food and water shortages, metals play second fiddle.

IML: Imagine filling your cavity with bitcoin or paper.

TM: I have. See this to know about Bitcoin: https://moneydelusions.com/wp/?s=bitcoin. Bitcoin dramatically illustrates that DEFLATION is even worse than INFLATION. The only “proper” level of each is zero. No process can measure it. And only a “real money” process can guarantee it to be zero…it’s the nature of the process: INFLATION = DEFAULT – INTEREST = zero.

IML: There is no similar floor under fiat currencies. The dollar and bitcoin are ultimately worth their weight in gold ($0).

TM: When you know what money is (i.e. a promise to complete a trade over time and space); when you know where money comes from (i.e. created by traders like you an me buying stuff with time payments); when you know where money goes (i.e. returned and destroyed with each time payment…or mitigated by INTEREST collections of like amount when DEFAULTed). The operative relation is: INFLATION = DEFAULT – INTEREST = Zero.

I value gold these days at roughly $2,000 per ounce. If you take all the gold in the whole world and divide it by the number of people, you get about one ounce per person as I recall…i.e. roughly $2,000…i.e. roughly 200 HULs. First, that’s not near enough for anybody’s need in trade…not in the near term…certainly not over time and space. But more importantly, the HULs are the only object guaranteed to have exactly the same value in every SBE. Gold goes up and down. Dollars go up…until they call the loans…then they go down dramatically. And as usual with all fake money…up is down and down is up when you think about it.

MD: A common provocative phrase. Money is an “in-process promise to complete a trade over time and space.” Well, substituting this provable definition for the “money” in the phrase, we essentially get “time is an in-process promise”. Obviously, it is not. Rather it is a fourth dimension defining “when” something is located “where.” Further we know that money is “always and only created by traders like you and me.” Well, you and I don’t create time. So how can time be money. The real principle is the “time value of money”. Does money today have a different value than money last year…or money a year from now. The simple answer: In a “real money process”, the value of money never changes…not over time…not over space. Thus, we can’t say it has time value.

It’s a phrase you’ve heard before. And probably a phrase you’ve accepted as truth. And it’s certainly true that there are plenty of ways that time and money relate to each other.

But a few months ago, I started to wonder: Is time really money? And if not, how does that change the way I think about my time and my money?

MD: Shouldn’t you begin by defining both “time” and “money”?

Today begins a series exploring those questions. I’ll tackle them from different angles and different aspects of entrepreneurship so that we can make more intentional decisions about how we spend our time and our money.

MD: How we “spend” our time and our money? That’s like “making more intentional decisions about how we trade.” There are only two ways: (1) Simple barter exchange in the here and now. (2) Exchange spanning time and space.”

First, a little context.

“Remember, time is money” is a line from Benjamin Franklin’s 1748 essay, “Advice to a Young Tradesman.” He encourages the reader to consider the money they might spend if they take a day off, as well as the money they’d lose for not working. I don’t know about you, but I feel like I’ve been running that calculation on repeat since I was sixteen years old! At least in the US, it seems we’re born with this idea already encoded into our brains.

MD: This is kind of a false choice. When you’re working, you’re in the process of making a trade. Not all work results in useful gain. Further, when you’re idle you’re in the process of doing something besides trading your “time and effort” for something. “Rest” is just such a thing…and if you don’t make that trade regularly you will die of exhaustion. Regardless, this has nothing to do with money.

Max Weber cites this aphorism repeatedly in his book, The Protestant Ethic and the Spirit of Capitalism. He sees it as a sort of semiotic turning point—a shift from the godly ethic of vocation to the secular ethic of capitalism. And remember, this phrase dates back to at least 1748. That’s 274 years of cultural indoctrination to this idea.

Now, if all of that sounds like I’m firmly against considering time as money (or money as time), I’m not. But I do think it’s an incredibly complicated truism that’s worth interrogating instead of merely accepting as immutable.

To kick off this deep dive into the question of whether time is actually money, I wanted to talk about money. And what money actually is, how we think about it, why the way we think about money matters. So I called up Paco de Leon, who just released a fantastic new book called, Finance For The People. She’s also the founder of The Hell Yeah Bookkeeping, which serves production companies and creative agencies. Paco knows more than a thing or two about money. But I wanted to start with the basics:

MD: Well, let’s see if Paco does indeed know a thing or two about money.

What is money?

At its most fundamental level, Paco told me, “Money is a shared delusion.” Money is valuable because we believe it’s valuable, not because it has inherent worth. If you’ve ever heard the term “fiat currency,” this is what it refers to: money that’s based on an agreement rather than an intrinsic value.

MD: Does a promise have value? Yes…of course it does. We value promises continually throughout our lives. And some promises we come to “not” value…because we know they won’t be kept. But knowing “all” promises creating money “will” be kept, either by the creator of the promise (and thus the money), or by the process that “guarantees” that the promise is delivered…and thus has value.

How is this guarantee accomplished? Well, it’s a lot like “casualty insurance”. You can send a ship of goods half way around the word. You can buy an insurance policy to guarantee “you” get paid for those goods and your ship returns. This is called a “PREMIUM”. And if your ship doesn’t return, you make “CLAIM” on the insurance provider. And in the insurance business, the operative relation is: PREMIUMS = CLAIMS. The money is made on the “investment income” from the PREMIUMS.

The operative relation for money is INFLATION = DEFAULT-INTEREST =zero. If the promise is not delivered, that is DEFAULT. Mitigating DEFAULTs with immediate INTEREST collections of like amount “guarantees” zero INFLATION. The crucial issue is “how” do you collect INTEREST and who do you collect it from?

That answer is you put the INTEREST load on irresponsible traders who have a non-zero propensity to DEFAULT. This is the same as the actuarial process of insurance: those who have the most CLAIMs pay the HIGHEST premiums.

About 10 or 11 years ago, I went to a lecture on money & meaning at my alma mater. Yes, I am that kind of nerd. That was the first time I was introduced to this idea—this fact, really. Money becomes valuable because you and I (and millions of other people) believe it is valuable. We believe it strongly enough to use money as a means of exchange and pay taxes and wages. The government incentivizes us to believe that—but ultimately, without the trust of US consumers, the dollar just wouldn’t be as valuable.

MD: So the lecture didn’t tell you that government is a dead-beat trader? If someone repeatedly lies to you, does that incentivize you to believe them? Of course not. You are admitting…you are deluded by government. A “real” money process gives money value by guaranteeing the completion of a trading promise spanning time and space. It doesn’t require government. In fact, government behavior precludes it from creating money…i.e. a promise it is known never to deliver…but rather to just roll over with a new promise…to deliver on a failed promise with a new promise, also guaranteed to fail.

Further, this lecturer explained money exists to make exchanging goods—buying and selling—easier. Instead of every trade being a negotiation of how many eggs are worth a pound of wheat, we can assign a monetary value to each product and then independently decide whether we want to trade our money for the eggs or the wheat or a new phone.

MD: The common unit of measure is only part of the story. Our current money process gives a name to a certain amount of gold and/or silver. That name is the “dollar”. It assumes that the value of gold and silver never changes. That assumption is a delusion. If they had chose the name HUL (standing for Hours of Unskilled Labor), that would have been better. A HUL trades for the same size hold in the ground over all time.

We’re seeing this play out in real-time right now with cryptocurrency, my current research obsession. What do people believe bitcoin or ether is worth? And how does that value fluctuate based on the number of people who believe in its value? How is a quote-unquote currency impacted if few sellers accept it as payment from buyers? If you’re curious about how this “money is a shared delusion” thing plays out practically, learn about crypto and all the wild things happening in that market. (Hint: it’s not great.)

MD: Crypto (specifically Bitcoin) claims a solution to the “byzantine general’s problem”. Basically it tries to guarantee truth. It does this with a concept it calls “proof of work” and therefore proof of value. It’s another delusion. You don’t create value by digging a hole and then filling it in again. But you do expend work. A real money process makes no claims whatever about the value of the “promise” (i.e. money). It just guarantees that it is ultimately delivered on…and destroyed. The units of the promise refer to something that doesn’t change over time. A HUL (Hour of Unskilled Labor) is a good choice as previously noted. In the interim a HUL trades as the most common “object” in simple barter exchange.

Back to the kind of money we have a stable agreement about. It can be hard to integrate the idea that money is a shared delusion because it’s so integral to the way we navigate the world. Our survival, in many ways, depends on how we earn and spend money. Paco was fascinated with that duality; money is both imaginary and key to our contemporary existence. She said, “Once we start to examine what [money] is at its core, we can start to (examine[sic]) ourselves, ‘If this thing is based on belief, well, how else is the way I interact with it based on beliefs?’”

MD: Do you describe “insurance” as a “shared delusion”…because it’s so integral to the way we make promises? Our survival depends on being of value. And that means trading our time for sustenance. Paco evidently failed in her examination of what [money] is at its core. You plant seeds with the belief that they will grow into a plant that you can eat. If you have a brown thumb like I have, you don’t believe it. But you can see skilled farmers making things grow. For me, I choose not to trade my time in planting. Rather, I trade it for something the farmer wants…and I trade that for the fruits of “his” planting. Don’t make this more complicated than it is.

What we believe about money impacts how we interact with it.

It’s the reason you and I can make drastically different money decisions, and they’re still the right decisions for us. Money isn’t an immutable, universal Truth—but a fluid, relative representation of value, which is always individual. What I value is not what you value. What you value is not what I value. What we each value will be decided by our circumstances, values, personal preferences, and priorities. And even within that relativity, there’s also the question of how value is related to available resources. For instance, I might understand and appreciate the value of investing in a house in Montana right now. It’s where we plan to move in about five years. But saying the market there is volatile would be an extreme understatement. Could I put together a down payment to buy property there? Sure. But I have to weigh the value of that money against the potential risk of buying now versus purchasing a few years from now.

Money isn’t an immutable, universal Truth—but a fluid, relative representation of value, which is always individual.

Paco gave me an even better example. Imagine you’re at a restaurant with a friend, and the Happy Hour special is $1 oysters. If you’re not an oyster fan, know that that price is a steal. You say to your friend, “I love oysters! Let’s get a dozen—that’s such a good price.” But your friend is dubious. “$1 oysters?” they say, “That’s… suspicious.” Maybe they are old. Perhaps the restaurant got them from an unscrupulous purveyor. Maybe they’re just not very good. You and your friend are working with the same financial information on the surface. It’s Happy Hour, and the oysters are $1 each. But you bring your beliefs about money and value to the table, and your friend brings theirs. The result is two drastically different approaches to the potential purchase.

MD: But none of that has to do with money. That has to do with trade. Trade has three stages: (1) Negotiation; (2) Promise to deliver; (3) Delivery as promised. In simple barter exchange, (2) and (3) happen simultaneously in the here and now. Money enables (2) and (3) to happen over time and space. And money has nothing to do with “belief”. That’s all taken care of in stage (1)…and it only applies to the two parties involved.

Our values, personal histories, upbringing, geographic location, culture, class… all these things and more influence the way we approach the proverbial $1 oyster. So do the beliefs that we have about ourselves. Paco told me that many of her original stories about money were informed by her belief that she wasn’t good enough. It might be easy to write it off as a “money mindset thing.” Yet, her anxiety about not being good enough was based on real experiences. She told me, “Being queer and a woman of color has not been a nice day at the beach. I’ve heard family members talking about so-and-so being gay. I remember hearing that story and being like: okay, noted, not okay to be gay.” She also picked up the “not good enough” message from thirteen years of Catholic school—a privilege in many ways, but also a daily immersion into a story about being fundamentally flawed.

MD: If Paco was this easily conflicted about money, what did she have to say about trade? Could she compare and contrast the two? I think you were wasting your time with Paco. In the land of the blind, the one eyed person is of most value. In the land of the queer, the straight person has a value deficiency in at least one category of trade…that being an inter-personal relationship…which is the most equitable trade possible.

The worry about not being good enough coalesced into a story that she should take what she’s given and be grateful for it, grateful to be included, to belong. But eventually, she started to shift that story—and decided to go out on her own in order so she could take control of the value of her work on the open market. And… still, she was undercharging for bookkeeping services and consulting. “I was that $1 oyster,” she said. So the work continued. She pursued therapy and other ways of processing her beliefs and experiences to unpack why she was perennially coming up short on decisions about price.

MD: Again, this has nothing to do with money. She is addressing the (1) Negotiation state of trader.

This is what we mean when we talk about understanding your money mindset. It’s not about “charging what you’re worth” or investing in yourself. It’s really a process of unpacking unconscious stories, weighing them against cultural conditioning, and finding ways to resource yourself to shift your thinking. “Thinking bigger” is just a bandaid over a much bigger issue. If you try to cover your money wounds with “charge what you’re worth,” you won’t get very far without bleeding out. This is why so much money mindset advice feels like a panacea. Before we can write a more effective money story, we actually have to root out and process the old one.

Before we can write a more effective money story, we actually have to root out and process the old one.

“The quality of your thinking impacts the decisions you make,” Paco told me. That’s why she cares about really getting to the heart of how we think about money, rather than trying to plaster over it with affirmations and financial advice. When you say something like “charge what you’re worth” to cover over feelings of inadequacy, the inadequacy is going to leak through. Those unexamined feelings influence your decision-making. So you find a way to rationalize a decision prompted by your original, negative money story rather than the one you think you’re telling. Paco says:

“Just feel your damn feelings on the upfront! Recognize that you’re an emotional creature. Sometimes your feelings are going to get in the way. Feel them and manage them and regulate your nervous system.”

MD: Again…is irrelevant to money.

The Moral Quality of Money

When we start talking about how our beliefs impact our decisions with money, we inevitably land on assumptions about the moral quality of money. Money and what we do with it seem to signal whether we’re a good or bad person, a good citizen or a bad citizen.

MD: This is nonsense. If you have grapes and you want strawberries, money gives you an option. You can “sell” your grapes for some number of HULs …hours of unskilled labor. You know a HUL value because you traded in them at some point in your life…usually a job during high school. You then take those HULs and find someone with strawberries. And you negotiate that trade. Using money you have two negotiation steps. (1) grapes for HULs; (2) HULs for strawberries. If you make a bad trade on you grapes, you still have a chance of correcting it on your trade for strawberries. Or you can gain on both trades or you can lose on both trades. It’s about your ability to trade. It’s not about money.

The messages around this can come from the oddest places—or, maybe, the most predictable least helpful places. For instance, in an interview on cable news, former Labor Secretary Elaine Chao said that low-wage workers had a patriotic duty to get back to work. Prosperity gospel preachers tell you that wealth is a sign of god’s favor. And the vast majority of the political machine in the US has been touting the welfare queen as the ultimate moral villain since Reagan.

MD: And again, be that as it may, it has nothing to do with money.

These messages aren’t the whole of the moral lessons we learn about money—they’re just the tip of the iceberg. They’re signposts of a pervasive, inescapable message about money; having money is good and, if you don’t have it, you better work your ass off for more of it so you can be good.

Paco said:

“We are overly focused on our own personal shortcomings, right? You did this wrong. You are bad. You are not disciplined. But what I really think what we need to focus on when we feel these negative feelings of shame and guilt is exploring and understanding where they came from. Who taught you that you should be ashamed of this? Where did you pick that up? Was it a move? Was it a song? Was it your grandparents?”

MD: I wonder what Paco would have to say about trading for art?

She said we pick up these expectations from family, friends, and society. When we violate that behavior, we feel bad. The answer? Paco says that financial pros need to help people heal the parts of them that are broken to help the people they serve to heal.

MD: And don’t forget the things we pick up from advertising and other forms of information and/or brainwashing.

Nowhere is moralizing more prevalent than in discussion about debt. But as Trump and other billionaires have proved repeatedly, debt only seems to be bad when you’re the wrong kind of person with that debt on your balance sheet. So I asked Paco: what’s the deal with debt?

MD: While you were at it, did you ask her “what’s the deal with a promise”? Is a promise a debt? Of course it is. The issue is “who are you indebted to?”

As is her gift, Paco gave me a great analogy. Debt is like fire, she said. Fire has benefits—it lets us cook our food, for instance. But if that fire gets out of control? Well, then there’s a problem. Debt has significant benefits. Without the invention of the 30-year mortgage, many of us would not be able to own real estate. Without a loan or a business credit card, we might not be able to make investments in the growth of our companies. But debt can quickly get out of control. And that’s when it becomes a problem. “We shouldn’t look at things with this tunnel vision of ‘debt is bad,’” Paco said. Black and white thinking rarely (maybe never?) benefits us.

MD: The “30 year mortgage” illustrates the scam that is our existing money system. (1) It assumes someone is “lending” you the money when in actuality, “you” are “creating” it. (2) It assumes you must pay “interest” on the money you have still not returned. Both are false in a “real” money process. In a “real” money process, money is in perpetually free supply. It never changes its value. And it imposes no resistance to trading (e.g. interest load).The effect? It has zero time value.

Is time money?

As I mentioned, I’m really interested in exploring the maxim, “time is money.” In what ways is that true? In what ways is it not true? And how might a fundamental, unexamined belief that time is money benefit or harm us and our work? So I asked Paco for her thoughts. She told me that there was a long time where she definitely ascribed to this philosophy. She’d make calculations about what she wanted to buy and whether the price was worth the amount of time it would take to earn that amount. She said it wasn’t a horrible way to think about money—but it’s certainly not the only way to think about the relationship between time and money.

MD: You took time to write this article. I took time to make these annotations. I received nothing in trade for my effort. That makes me a fool. What did you receive for writing the article? You received nothing from me. If you have advertisers they “may” have received “eyeballs” and paid you accordingly. Or you may benefit in some indirect way from educating me. That being the case I would be receiving negative education… would that be deception? Or reading my comments “you” would be being “properly” educated. Which of us is more valuable? Has nothing to do with money does it!

For instance, when she started hiring, she realized that she could create leverage with other people’s time. As a business owner, she could use their work to earn more. She also thinks about how money can buy time, “Time is a non-renewable resource. Money is a renewable resource.” And, of course, she’s very interested in investing in a way that produces more money without more time spent on work.

MD: “Money is a non-renewable resource”: Try this? You can make money writing this article. You can obtain a hole by digging. If you need a hole, would you choose to spend your time writing this article for money…then trading that money for a guy to dig your hole? What if it takes twice as long to dig the hole yourself than to have the guy do it. Did you “reclaim” some non-renewable time? You know the old axiom: work smarter, not harder.

Paco and I agree that the danger in believing “time is money” is that it often reinforces conditioning around productivity and usefulness. We learn at an early age that the goal is to get as much done in a certain period of time as possible—the more ways we can hack our time to produce more, the more we’re rewarded. We’re also taught to evaluate our worth to society from the perspective of productivity. Taking time off, therefore, risks getting you labeled as lazy. And that brings us back to the core belief Paco (and I) have had to wrestle with: Am I enough? Am I doing enough?

MD: And again, that’s all irrelevant.

“Am I deserving of the space to just be a human appreciating the sunshine on my face? I want to normalize wanting to chill,” she told me.

“To me, money is freedom and it’s power. It allows me to live a life of dignity.”

MD: And if sea shells were money does that make picking up sea shells bring you more freedom and power? You know it doesn’t. You can’t just call something money and make it be so. It’s the process that brings the value. And a process that thinks sea shells have common value is inferior to a process that thinks HULs have value. In sea shells, like in paintings, the value is in the beholder. With money using HULs, the traders are more likely to value them identically. Certainly over time that is true: People no longer trade in sea shells. Sea shells have lost their value as a trading object long long ago.

As we started to wrap things up, Paco told me that she really wants people to be able to live a life of dignity. Yes, we need to concern ourselves with our own personal finances. But we should also be concerned about the public policies that would allow all people to live dignified lives. She said, “let’s just solve that problem first. And then luxury will follow.”

MD: If “all” people just took care of themselves “all” would be fine. That’s everyone’s first task…take care of yourself.

I’ve been rolling the idea of “dignity” around in my mind since I talked to Paco. Who is denied dignity? What are the mechanisms that enforce that denial? What does a dignified life look like, and how much does it cost?

Paco does such a great job of addressing the things we can control about money. And she also does a great job acknowledging that there is much that’s out of our control. This is certainly true when it comes to dignity, as well. We can do a lot for ourselves to ensure a dignified life. But for many of us, factors out of our control make it incredibly difficult. So, what policy changes could we advocate for so that all people could have access to a dignified life? What community care projects could help more people live with dignity?

MD: If you have money and you created it, you must eventually return it as you promised and it is destroyed. If you obtained your money in trade, it’s no different than grapes you obtained in trade…except for the process. With a “real” money process, you can put your money under a rock for 10 years…then take it out and trade it for the same size hole in the ground as you could 10 years ago. With grapes…well, they rotted 10 years ago. And with our counterfeit dollar, you can trade for a hole that is 2/3rds as big…assuming 4% inflation caused by government counterfeiting.

We all have room to work on our beliefs about money, and many of us have enough space to start changing the larger conversation, too.

MD: Actually, everything in your article is about “trade”…not “money”.

David Lawant this is my bio More posts by David Lawant.

MD: This blog named MoneyDelusion.com (note singular, not plural like this one) I tripped over. It was created in 2020. MoneyDelusions.com (note plural…was created three years earlier in 2017). This David Lawant is likely a Mises Monk. He’s posted three articles to his blog…one each day for three days…and then nothing. I wonder what he thinks he’s up to. Let’s see if he knows anything about money. If he does he’ll be the first Mises Monk I’ve found who does…and wouldn’t that be exciting!

A Medium of exchange (MoE) is an economic good that is used in exchange for other goods. Money is nothing more than a special case of media of exchange that happens to be universally accepted through a process that has already been well described elsewhere. Under this definition Bitcoin is not money because it’s not commonly accepted (yet), but it certainly is a MoE. For this text you can read these two concepts as synonyms, as everything here about money can be generalized to media of exchange without any loss in meaning.

MD: Right off the bat it looks like he doesn’t get it. A “medium” is the environment (control) within which “media” exists. It’s a minor point…unless his confusion goes deeper. Nope: Second sentence his thinks “money” is a special case of “media”. This is wrong. Money “is” the media. Different “cases” would be like ledger entries, demand deposits, coins, currency, etc. And what is this “universally accepted process described elsewhere”? Now he swerves into correctness…Bitcoin “is” not money…but it looks like it’s “acceptance” that is not mature enough…and thus will eventually be money. He’s wrong. It’s not created correctly. That’s what keeps it from ever being money. That’s what makes it just being stuff of simple barter exchange like gold and silver. And read that last sentence again. He is “money deluded”…that’s for sure.

Media of exchange are not a payment system, as Pierre Rochard correctly and insistently emphasizes. Although a payment system might be a nice-to-have feature to transfer a MoE form one hand to another, it is important to understand that these are completely orthogonal concepts. The channel through which a good is exchanged is not important for the economic analysis of a MoE. What matters is that the good is primarily used to be exchanged for other goods. Ludwig von Mises traced this confusion to a juridical view of money:

…the principal, although not exclusive, motive of the law for concerning itself with money is the problem of payment. When it seeks to answer the question ‘What is money?’ it is in order to determine how monetary liabilities can be discharged. For the jurist, money is a medium of payment. The economist, to whom the problem of money presents a different aspect, may not adopt this point of view if he does not wish at the very outset to prejudice his prospects of contributing to the advancement of economic theory.

MD: See…I told you he was a Mises Monk…and his brain is thoroughly contaminated. We here know that money is “an in-process promise to complete a trade over time and space.” It is always, and only, created by traders like you and me. It may never circulate as an object of simple barter exchange…but virtually always does. And when it does, it trades like any other object that two traders are willing to exchange. But its process is what makes it special. Real money has zero intrinsic value. But when properly protected from counterfeiting, it is the most efficient and most trusted of any object of simple barter exchange. This is because its value never changes over time and space. This is because there is no interest load associated with using it. And it is because the “process (e.g. medium) guarantees this to be so. It cannot operate any other way.

Some Bitcoiners question whether it makes sense to stress so much the MoE aspect of money if it is only a stage in the evolutionary process brilliantly depicted by Nick Szabo (collectible, store of value, medium of exchange, and unit of account). The point, as Szabo points out, is that something special happens when an economic good becomes a medium of exchange.

MD: Here you see a very common attribute of the Mises Monks…that is worship of other Mises Monks. They’re truly a mutual admiration society. It is a religion…and misguided like all religions. But the key thing to note here: An economic good does not “become” a medium of exchange (or even properly a “media” of exchange). Money is not an economic good…it is a “promise”. And “real” money is a promise that is guaranteed to be kept. It’s designed into the process. The sidebar explains it in very simple terms.

Categorization of Economic Goods

One of the most basic distinctions in economics is the one between consumption and production goods, usually called by Austrian economists as first-order and higher-order (second-order, third-order, etc…) goods. We can get away for now with the following simplified definition: first-order (consumption) goods satisfy direct human needs and higher-order (production) goods are used to produce lower-order goods.

MD: Money has no interest in what it is being traded for or how it will be used…or why it is being traded. Why should it? Why do they make this complicated? If I trade money for a hammer, do I care if it’s used to pound nails or to blacksmith wrought iron…or just to hang on the wall? If this article tells us why “he” cares we’ll correct him at that instant.

There’s nothing intrinsic about whether a good is first or higher order. For example: I can consume a certain amount of water to satisfy my thirst (i.e., water as a first-order good) or alternatively I can provide this same amount of water to cattle which I will ultimately consume as food (i.e., water as a second-order good and cattle as a first-order good).

First- and higher-order economic goods, albeit ultimately connected to a fundamental theory of value, are different enough to be treated separately in many instances. As Jesus Huerta de Soto puts it: “this classification and terminology were conceived by Carl Menger, whose theory on economic goods of different order is one of the most important logical consequences of his subjectivist conception of economics”.

Peter Paul Rubens’ representation of an altcoiner trying to spin up a monetary system (c. 1614–1616)

MD: More praise for fellow Mises Monks. Look how far we are into this article and he still has said nothing that has to do with money. He’s just tried to act like an intellectual. We know that as “double talk”. And watch out for creation of a new “..ist”…in this instance “subjectivist”. Does the world really need any more “ists”?

We have thus defined that media of exchange are goods that have no real “utility” aside from being exchanged for other goods, which in turn have real “utility” of their own. So how do we classify media of exchange? Are they first-order (consumption) or higher-order (production) economic goods? Is there anything especial about media of exchange that warrants a special analysis of them?

MD: When you realize that it’s the entire trading universe that is the “medium” of exchange, you don’t have to classify anything. In trading, those who prefer to trade for gold know its value. If they trade in silver, they know its value. What is different about “real” money is “its value never changes.” This can’t be said for any other object of simple barter exchange.

MD: The preferred unit for money is the HUL (Hour of Unskilled Labor). For all time in the past it has traded for the same size hole in the ground. And in a “real” money process, it will trade for the same size hole in the future. It is the traders who decide in their personal trades how many HULs is being traded.

MD: And this is a great simplification over the complicated process he alludes to. In his process you have to know the changing value of every good and service …in your mind. But when it comes to “real money” as one of the exchanged objects, you always know its value. When you were in high school (i.e. unskilled labor) you knew exactly what people were willing to pay for it. With the improperly managed dollar, people were willing to pay me $1.50 for a HUL. Today they are willing to pay $8.00. Why? Because the improper “dollar process” has allowed counterfeiting. They have allowed the supply/demand balance to change over time…and it is with supply continually outstripping demand through government counterfeiting (i.e. making promises they never keep)…counterfeiting “inflates” the supply. It’s just that simple.

Media of Exchange Are a Sui Generis Type of Economic Good

The number of economists who don’t have good answers to these questions is astounding. Most simply classify media of exchange as a higher-order good by exclusion. They don’t have direct “utility”, so they cannot be first-order economic goods.

MD: Here we see the pot calling the kettle black. I’m going to just let him spew on here. To put what he writes in context, he thinks gold is money. He thinks money “always” has intrinsic value. Gold thus gets its value by digging dirt and refining it. But dirt in your back yard isn’t going to give you any gold…no matter how much you refine it. And you can argue until you’re blue in the face that you put as much work into your backyard dirt as the gold professional put into his. He got gold…you didn’t. He got something to trade for his HULs…you didn’t. But when you know money is a promise, and you know “real” money comes from a process that “guarantees promises”, you don’t need to screw around with things like gold. I’ll let you read on yourself for a while. These guys make me tired..

Austrian economists think this approach is simplistic and inconsistent. They defend a three-fold categorization of economic goods: first-order (consumption) goods, higher-order (production) goods and media of exchange. This is a key proposition in Ludwig von Mises’ indispensable Theory of Money and Credit. He even criticizes his master Eugen von Böhm-Bawerk and defends the position of Karl Knies, economist of the rival German historical school, in this respect:

Production goods derive their value from that of their products. Not so money; for no increase in the welfare of the members of a society can result from the availability of an additional quantity of money. The laws which govern the value of money are different from those which govern the value of production goods and from those which govern the value of consumption goods.

The peculiarity of media of exchange, and by extent of money, as economic goods is clearly exposed by a simple conundrum. We know intuitively that every economic good can command a price because it has “utility”. If the “utility” of a MoE is to have purchasing power (i.e., a price), how to we get out of this circular reference to understand how money has value? Mises derived his famous regression theorem to solve this apparent circularity by introducing the time element, but this is outside the scope of this text. What matters for us is that media of exchange are unique because their “utility” and purchasing power coincide. As Murray Rothbard puts it:

Without a price, or an objective exchange-value, any other good would be snapped up as a welcome free gift; but money, without a price, would not be used at all, since its entire use consists in its command of other goods on the market. The sole use of money is to be exchanged for goods, and if it had no price and therefore no exchange-value, it could not be exchanged and would no longer be used.

MD: Here is a good time to comment on this thing they call “price”. It’s how much of the stuff you have and are willing to trade for how much of the stuff your trading partner has and is willing to trade. If the “stuff” is real money, you both know exactly what is being traded…one hour of unskilled labor…and it’s guaranteed. You can convert that to dollars, marks, franks, ounces of gold, or pork bellies. It’s up to you to decide on that conversion. But one thing you don’t have to do with “real” money. You don’t have to decide what a HUL is worth. You always know, because at one point in your life your were one…an hour of unskilled labor. So if you’re using “real” money, your trade just got less risky by a factor of two (i.e. one of the objects being traded is “guaranteed” not to change over time and space). Let’s let him blab on further for a while..