MD: You can’t get so-called crypto currencies right if you don’t know what money is. Money is obviously and provably “an in-process promise to complete a trade over time and space.” Money is “always”, and “only” created by traders making such promises. Money is destroyed as those traders deliver as promised. And if they fail to deliver as promised the resulting DEFAULT is immediately reclaimed by INTEREST collections from new money-creating traders with a like propensity to default.

Knowing this, let’s parse this article and expose this writer’s delusions.

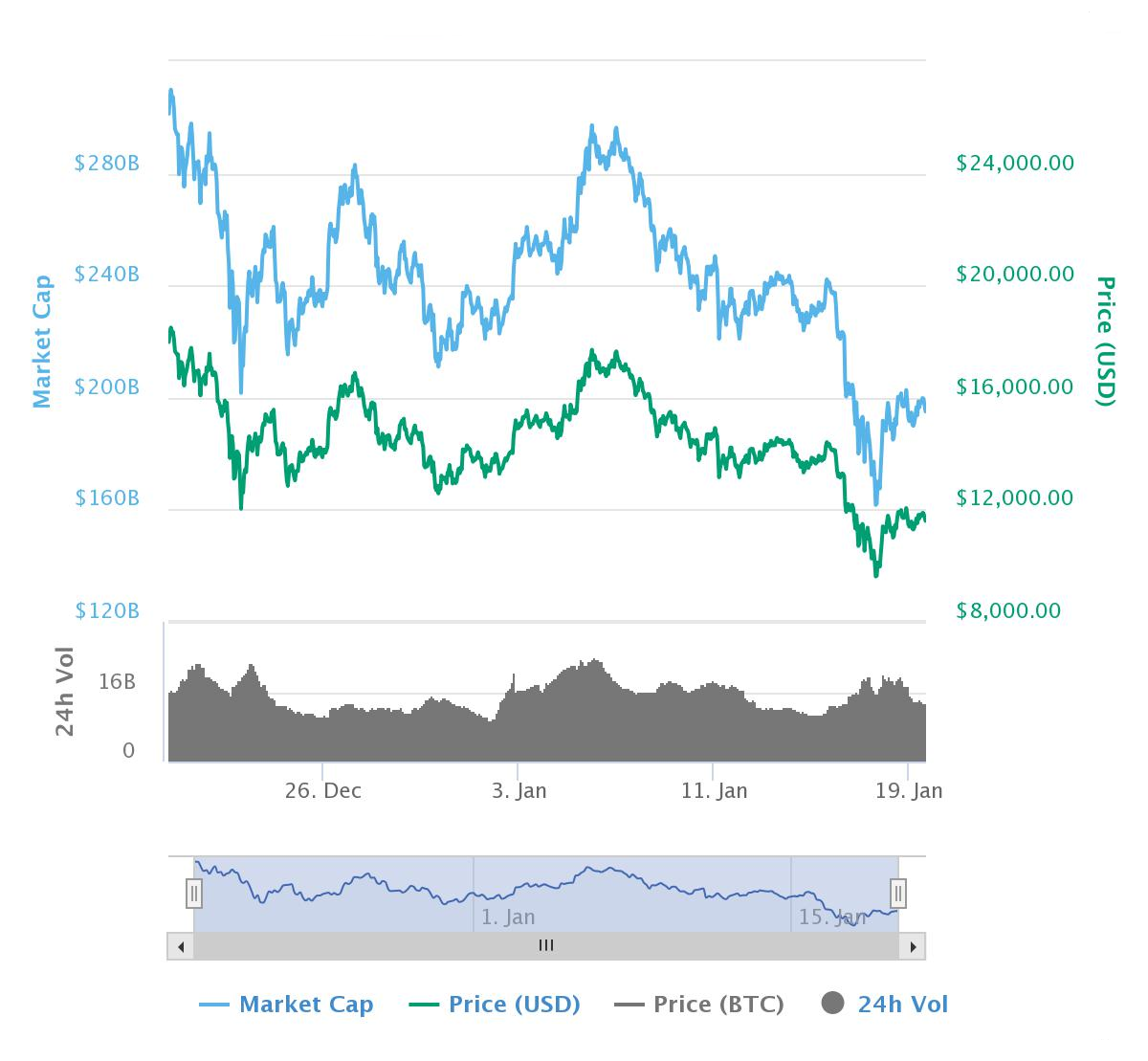

Bitcoin suffers a big correction after swinging wildly in the last 10 days of December. … Sometime in the next three months we will see a sell-off as latecomers panic and sell. Long-term investors will remain in bitcoin and it will creep back up, but will not revisit its December highs.

MD: Admission of failure. “Real” money doesn’t have big corrections and swings. In fact it never swings at all.

I nailed it.

Bitcoin peaked about a month ago, on December 17, at a high of nearly $20,000. As I write, the cryptocurrency is under $11,000 … a loss of about 45%. That’s more than $150 billion in lost market cap.

Cue much hand-wringing and gnashing of teeth in the crypto-commentariat. It’s neck-and-neck, but I think the “I-told-you-so” crowd has the edge over the “excuse-makers.”

Here’s the thing: Unless you just lost your shirt on bitcoin, this doesn’t matter at all. And chances are, the “experts” you may see in the press aren’t telling you why.

In fact, bitcoin’s crash is wonderful … because it means we can all just stop thinking about cryptocurrencies altogether.

The Death of Bitcoin…

In a year or so, people won’t be talking about bitcoin in the line at the grocery store or on the bus, as they are now. Here’s why.

Bitcoin is the product of justified frustration. Its designer explicitly said the cryptocurrency was a reaction to government abuse of fiat currencies like the dollar or euro. It was supposed to provide an independent, peer-to-peer payment system based on a virtual currency that couldn’t be debased, since there was a finite number of them.

MD: Delusion admission: When you’re talking about “real” money, there is a perpetual perfect balance between supply and demand for the money itself. And of course both are finite and both vary in lock step.

That dream has long since been jettisoned in favor of raw speculation. Ironically, most people care about bitcoin because it seems like an easy way to get more fiat currency! They don’t own it because they want to buy pizzas or gas with it.

MD: Common slur from those deluded about money. They call it “fiat” currency. Since all money represents a promise, and all promises are fiat, all money is fiat. Slur bounces right off.

Besides being a terrible way to transact electronically — it’s agonizingly slow — bitcoin’s success as a speculative play has made it useless as a currency. Why would anyone spend it if it’s appreciating so fast? Who would accept one when it’s depreciating rapidly?

MD: Bitcoin’s major flaw in this regard is its insistence on keeping track of every single trade (and thus fractioning) of the bitcoins once created. This is totally unnecessary. All you must keep track of is the creation of “real” money by traders and the destruction of it as they deliver as promised. You must keep track of defaults and meet them immediately with like interest collections. Beyond that, the “real” money trades totally anonymously.

Bitcoin is also a major source of pollution. It takes 351 kilowatt-hours of electricity just to process one transaction — which also releases 172 kilograms of carbon dioxide into the atmosphere. That’s enough to power one U.S. household for a year. The energy consumed by all bitcoin mining to date could power almost 4 million U.S. households for a year.

MD: Tying the Bitcoin nonsense to the global warming nonsense is truly humorous. That not-withstanding, a “real” money process consumes virtually zero energy. The trees have to look elsewhere for their carbon dioxide.

Paradoxically, bitcoin’s success as an old-fashioned speculative play — not its envisaged libertarian uses — has attracted government crackdown.

MD: Governments are helpless (in a competitive sense) in defending themselves against a “real” money process. Once people see it, the nonsense of government itself is quickly exposed and governments wilt on the vine … a bloodless war ending quickly.

China, South Korea, Germany, Switzerland and France have implemented, or are considering, bans or limitations on bitcoin trading. Several intergovernmental organizations have called for concerted action to rein in the obvious bubble. The U.S. Securities and Exchange Commission, which once seemed likely to approve bitcoin-based financial derivatives, now seems hesitant.

And according to Investing.com: “The European Union is implementing stricter rules to prevent money laundering and terrorism financing on virtual currency platforms. It’s also looking into limits on cryptocurrency trading.”

We may see a functional, widely accepted cryptocurrency someday, but it won’t be bitcoin.

MD: All will fail just as bitcoin will fail. Why? Because none of them behave as real money. Nothing can out-compete real money. At best, it can only tie. And “Real Money Processes” (RMPs) can co-exist. They follow the same rules, concepts, principles, and actions. Thus, the exchange rate between any, and all other RMPs is perpetually 1.0000. It’s the nature of an RMP to never change value over time and space.

…But a Boost for Cryptoassets

Good. Getting over bitcoin allows us to see where the real value of cryptoassets lies. Here’s how.

To use the New York subway system, you need tokens. You can’t use them to buy anything else … although you could sell them to someone who wanted to use the subway more than you.

In fact, if subway tokens were in limited supply, a lively market for them might spring up. They might even trade for a lot more than they originally cost. It all depends on how much people want to use the subway.

MD: Subway tokens are close to “real” money. They are created by those intending to travel. They are destroyed as they complete their trip. In the process, there is perfect balance between supply and demand for them. They fail as real money because they can only be used in one very narrow marketplace … the subway.

That, in a nutshell, is the scenario for the most promising “cryptocurrencies” other than bitcoin. They’re not money, they’re tokens — “crypto-tokens,” if you will. They aren’t used as general currency. They are only good within the platform for which they were designed.

MD: With real money, there is no distinction between tokens, coins, currency, or ledger entries. The money can move from one form to the other with perfect freedom. Just like a baton plays no role in running a race, the tokens themselves play no role in actual trading. They are simply a score keeping mechanism. And they only exist in one form at a time for a specific HUL (Hour of Unskilled Labor… the unit of measure of an RMP).

If those platforms deliver valuable services, people will want those crypto-tokens, and that will determine their price. In other words, crypto-tokens will have value to the extent that people value the things you can get for them from their associated platform.

MD: Nonsense. The proper unit of measure of real money would be the HUL (Hour of Unskilled Labor). It never changes its value over time and space. It always trades for the same size hole in the ground. So does real money.

That will make them real assets, with intrinsic value — because they can be used to obtain something that people value. That means you can reliably expect a stream of revenue or services from owning such crypto-tokens. Critically, you can measure that stream of future returns against the price of the crypto-token, just as we do when we calculate the price/earnings ratio (P/E) of a stock.

MD: Tokens and currency are real assets with “recorded” value, not intrinsic value. If I have currency and I exchange it for a ledger entry, that currency (which has never had intrinsic value but does have trading value) can be burned and there is no change in value anywhere. But it can only be put back into exchange by exchanging it with HULs in other forms (e.g. ledger entries or coins). Money in the form of currency or tokens is only money when it is involved in trade. And if someone puts them under a mattress, it “is” involved in trade. However, if the process exchanges it for a ledger entry and the currency or token is placed on a pallet, it and everything else on that pallet has zero value … just like a baton sitting in a locker before or after a race plays no role in a race.

Bitcoin, by contrast, has no intrinsic value. It only has a price — the price set by supply and demand. It can’t produce future streams of revenue, and you can’t measure anything like a P/E ratio for it.

MD: This is a major major delusion. Money has a unit of measure (ideally the HUL – Hour of Unskilled Labor) but no price. This is because the supply/demand ratio is guaranteed to be perpetually unity. It’s value is in the eyes of the traders. The RMP process itself sees its value as an Hour of Unskilled Labor (HUL). Everyone has traded their time as a HUL at some point in their life. For example, they may mow a lawn for an hour… or babysit for an hour. For perspective, today a HUL trades for about $15.00. 70 years ago when my labor was unskilled, a HUL traded for $1.50. And back in 1913 when the scam known as the Federal Reserve was created, a HUL traded for about a penny.

One day it will be worthless because it doesn’t get you anything real.

MD: Real money will always have value as long as “responsible” traders exist. Responsible traders don’t default. They use money as it should be used … as an in-process promise to complete a trade over time and space. And the vast majority of us are responsible traders. There are really very few deadbeats and the proper money process quickly makes them uncompetitive traders… they are naturally ostracized from the marketplace.

(For more of my thoughts on the differences between cryptocurrencies and crypto-tokens, click on the video below.)

Ether and Other Cryptoassets Are the Future

The crypto-token ether sure seems like a currency. It’s traded on cryptocurrency exchanges under the code ETH. Its symbol is the Greek uppercase Xi character (Ξ). It’s mined in a similar (but less energy-intensive) process to bitcoin.

MD: Oh really? What is the distinction? What is the difference?

But ether isn’t a currency. Its designers describe it as “a fuel for operating the distributed application platform Ethereum. It is a form of payment made by the clients of the platform to the machines executing the requested operations.”

MD: With real money a process is needed to keep track of things. But that cost is negligible compared to the cost of the things being tracked.

Ether tokens get you access to one of the world’s most sophisticated distributed computational networks. It’s so promising that big companies are falling all over each other to develop practical, real-world uses for it.

Because most people who trade it don’t really understand or care about its true purpose, the price of ether has bubbled and frothed like bitcoin in recent weeks.

MD: This isn’t because of misunderstanding. It’s because there is no guaranteed perpetual balance between supply and demand for the stuff.

But eventually, ether will revert to a stable price based on the demand for the computational services it can “buy” for people. That price will represent real value that can be priced into the future. There’ll be a futures market for it, and exchange-traded funds (ETFs), because everyone will have a way to assess its underlying value over time. Just as we do with stocks.

MD: Does this suggest it somehow maintains perfect supply/demand balance for the money itself? How does it do that???

What will that value be? I have no idea. But I know it will be a lot more than bitcoin.

MD: Proving you are deluded. If you knew what money was and you knew what you speak of to be money, you know perpetually what its value will “always” be. It will always be a HUL.

My advice: Get rid of your bitcoin, and buy ether at the next dip.

MD: This reminds me of the quip “you have to love standards … there are so many to choose from”.

MD: If you understand money, you know the proper process to enable it “guarantees” perpetual perfect supply/demand balance for the money itself. Thus, it is neither inflationary nor deflationary.

The Bitcoin process thinks (like the gold bugs think) that money needs to be rare to be viable. This is nonsense of course. But Bitcoin is enormously “deflationary” as a consequence of its process. Supply is severely limited and ultimately capped. Demand is exploding because of this (because it is deflationary) … not because Bitcoin is viable money.

Nobody in their right mind owning bitcoins would ever part with them (unless the inevitable collapse was in progress). That’s the nature of a “deflationary” asset. The only appeal to bitcoins is their anonymity. And thus it is illicit trade that is really finding bitcoin useful. Everyone else holding them is gambling … plain and simple.

I have never tried to really understand the underlying process of bitcoin mining. The reason for this is the process is bogus on its face. It has no way of matching supply and demand. If this is a characteristic of all cryptocurrencies (and block chain mechanisms) in general, then all are not viable. However, I see no reason a block chain concept cannot be devised that creates new transparent, unchangeable blocks at zero cost. Then the proper MOE process uses the block chain to deliver the necessary “transparency” attribute of a proper MOE process.

As always, I’ll now intersperse comments as appropriate to highlight these obvious principles and violations thereof.

There’s a debate raging over what, exactly, bitcoin and the thousand or so other cryptocurrencies actually are. Some heavy-hitters are weighing in with strong, if not always coherent opinions:

MD: Oh really? What is being debated? That they are money?

Jamie Dimon calls bitcoin a ‘fraud’

JPMorgan Chase CEO Jamie Dimon did not mince words when asked about the popularity of virtual currency bitcoin.

Dimon said at an investment conference that the digital currency was a “fraud” and that his firm would fire anyone at the bank that traded it “in a second.” Dimon said he supported blockchain technology for tracking payments but that trading bitcoin itself was against the bank’s rules. He added that bitcoin was “stupid” and “far too dangerous.”

————————

Peter Schiff: Even at $4,000 bitcoin is still a bubble

One of the best-known among the bears, investor Peter Schiff, is now making his case in even stronger terms for why bitcoin has advanced ever farther into bubble territory.

MD: It went into bubble territory right out of the box.

Schiff, who predicted the 2008 mortgage crisis, famously referred to bitcoin as digital fool’s gold and compared the cryptocurrency to the infamous bubble in Beanie Babies.

Moreover, the recent run-up in bitcoin hasn’t softened Schiff’s view: If anything, it’s reinforced his sense of impending doom.

Schiff told CoinDesk:

“There’s certainly a lot of bullishness about bitcoin and cryptocurrency, and that’s the case with bubbles in general. The psychology of bubbles fuels it. You just become more convinced that it’s going to work. And the higher the price goes, the more convinced you become that you’re right. But it’s not going up because it’s going to work. It’s going up because of speculation.”

MD: The fact that it is going up is proof that it “does not work”. Real money never goes up or down. It stays constant over all time and space.

“What it comes down to is that bitcoin ain’t money.”

“Libertarian-minded crypto fans saw this was a way to liberate people from the government,” he said, concluding:

“I think it will have the opposite effect. People are going to lose money. This could really backfire, giving libertarian ideals a bad name by making fiat look good. The downside can be really spectacular.”

MD: Actually, a competitive proper MOE process would give people an alternative to the “improper” MOE process commanded by the money changers and the governments they institute. If instituted properly (i.e. guaranteeing zero inflation), and in multiplicative fashion (like credit cards) nobody would continue to use government money, It couldn’t compete. The government would be forced to demand use of government money (for more than just paying taxes) and that would tip their hand … i.e. that they are simply the money confiscation machine instituted by money changers. Right now that machine is confiscating 3/4ths of everything each of us makes.

————————

Cryptocurrencies are currencies with no government in the middle. No bank in the middle. No organizations in the middle keeping track of all your payments, or taking advantage of your spending so they can invade your privacy, and on and on.

Cryptocurrencies solve trillions of dollars’ worth of problems, which is why they will be worth trillions of dollars one day.

MD: He says about three things that are right and then caps it off by saying something that proves they solve no problems at all.

Consider the potential:

There is currently $200 trillion in cash, money and precious metals used as currencies in the world. Meanwhile, there’s only $200 billion in cryptocurrencies. Cryptocurrencies are eventually replacing traditional currencies.

MD: If he knew what he was talking about … i.e. what money really is … he would also say there are currently $200 trillion in-process trading promises (net of government counterfeiting that is demonstrably about 4%). But of course that isn’t true because government trading promises are always defaulted … i.e. counterfeiting right out of the box.

So that $200 billion will eventually rise to the level of currencies. And probably sooner than we can imagine.

MD: Admitting he is clueless about money. Supply and demand for real money rise and fall in lock step.

Ask yourself, why does the world need multiple currencies? There’s actually no real reason. The only reason we have a U.S. dollar and also a Canadian dollar is that in 1770 the people in Canada decided not to join the U.S. So an artificial border created two currencies. It’s all dictated by artificial borders.

MD: Actually, it’s because “none” of the world’s currencies are from a “proper” MOE process. If we had a proper MOE process that “guaranteed” zero inflation, then there would be no need for multiple currencies (exchange rates would be perpetually constant). However, there always should be multiple processes in operation … just like there should be multiple insurance companies in operation. They’re addressing an identical problem and are disciplined and driven to efficiency by transparency and competition.

In the past, an ounce of gold would be accepted almost anywhere in the world. In that sense, unbacked modern fiat currencies are a step backwards.

MD: As it is today. Gold becomes more acceptable in trade as the MOE process in place becomes more and more “improper” (i.e. tolerates more and more counterfeiting by governments and more and more tribute demands by the money changers. Gold is just a clumsy inefficient stand-in for real money.

But in cryptocurrency world, there are what I call “Use Borders.” Every currency is defined by its use. For instance, Ethereum is like Bitcoin but it makes “smart contracts” easier. Contract Law is a multi-trillion dollar industry so this has a huge use case. Filecoin makes storage easier. It’s a $100 billion industry. And on.

Studying the “use” cases, and the effectiveness of the coin to solve those use cases can help us make investment decisions confidently.

MD: KISS (Keep is Simple Stupid). Money is not about “use cases” … it is about trade over time and space. Block chains may be about use cases, but those cases are not cryptocurrency. They’re not currency at all. Who ever thought of a contract as being currency? Just trapped myself didn’t I … because in a proper MOE process, the money represents a contract … a promise by a trader to the whole trading community that he will deliver on a trade over time and space.

This is the great promise of cryptocurrencies and why they will change the world. It’s just getting started.

No normal non-expert should expect to make sense of the above. So let’s just assume that the cryptocurrency universe will continue to expand for a while and narrow the discussion down to a single question: Are cryptocurrencies inflationary? That is, will their spread lead to higher or lower prices for the average person, and greater or lesser financial instability for the markets, and what does this mean for today’s fiat currencies?

MD: That’s his judge of inflation? Higher (or lower prices)? Prices are just a crude measure of inflation. Inflation can’t be measured. But a proper process can guarantee it to be zero … and thus requires no measurement. No block chain process I have ever seen described attempts to maintain perfect balance between supply and demand for the money (i.e. trading promises) it represents.

MF: I suggest you continue to read this article if you find it interesting. If you do, I suggest you continue to annotate it in your mind knowing the principles of “real” money and how they apply. This article is making me tired.

One common opinion is that cryptocurrencies can’t be inflationary because their owners have to pay for them in fiat currencies. So one bitcoin bought means one dollar, yen, or euro sold, with the net effect on prices being zero.

This makes intuitive sense at first glance, but only holds for the moment of purchase. Consider what happened after someone in, say, 2014 exchanged dollars for bitcoins. The dollars held most of their value, which means the total amount of dollar purchasing power in the world remained constant. But those bitcoins went up by several thousand percent, dramatically increasing the purchasing power – and thus the potential inflationary impact – of the bitcoin complex.

In a Tweet on Saturday, Assange said the group’s investment in the cryptocurrency has seen a return greater than 50,000% since 2010. Wikileaks began investing in bitcoin back then because global payment processors like Visa, Mastercard, and Paypal were under pressure by the U.S. government to block the ability of the group to take payments.

In fact, Bitcoin has seen a more-than 9 million percent return over the dates Assange references. In certain periods in 2010, bitcoin was trading for mere pennies. According to coindesk.com, one unit of bitcoin is now worth a record high of roughly $5,700. Anyone buying bitcoin through much of 2011 and 2012, when one unit was sometimes trading below $1 and was often under $10, would indeed see a return on investment of more than 50,000%, assuming they never sold.

The difference between Wikileak’s purchasing power pre and post-bitcoin is immense. If Assange decides to spend his windfall on goods and services he’d have, at the margin, an inflationary impact on the stuff he buys.

So the answer to the question of cryptocurrencies’ impact on price levels depends on how their values change. If they rise after people buy them, then they’re inflationary. If they rise a lot, they’re potentially very inflationary.

In this sense, it might be helpful to view cryptocurrencies as assets like houses or stocks rather than as money. When they rise relative to fiat currencies they increase the purchasing power of their owners, generate a “wealth effect” in which owners feel richer and more comfortable with splurging, and in that way push up prices. Based on the following chart, a lot of early adopters are feeling a whole lot richer these days.

Which then leads to what might be the major cryptocurrency theme of the coming year: Why would governments allow such an inflationary supernova to explode right in front of them when they presumably have the power to stop it? Here’s one possible — and of course disturbing — answer:

Will cryptocurrencies trash cash? ‘Fedcoin’ could do it

Economist Ed Yardeni of Yardeni Research asks the obvious question: Why would central banks—which derive their power as the centralized gatekeepers of fiat currency creation, check clearing and payment processing—embrace a movement that’s primary motivation has been to usurp this power in a decentralized way?

Part of that, according to St. Louis Federal Reserve president James Bullard, is recognition that the technology has achieved critical mass. Thus, there’s a fear of being left behind as the very foundations of banking and monetary policy—intermediation, funds transfers, transactions—rapidly change, not unlike the way the creation of mortgage-backed securities and credit default swaps changed housing finance in the mid-2000s.

There’s another, more self-serving purpose: Central banks could use their own cryptos to put the squeeze on paper currency. Why? To facilitate the use of negative interest rate policy, which has been deployed in Europe and Japan in recent years in half-baked forms. Currently, in Switzerland, short-term interest rates are at -0.75%.

When another recession hits, especially if one comes soon, a dive to even deeper rates of negative interest would be hampered by the hoarding of cash since banks would charge for deposits (vs. absorbing the cost of negative rates themselves, as they’re doing now). This is known by the economics cognoscenti as the “zero lower bound” in that interest rates cannot go much below negative before the traditional functions of deposits, loans and fractional money creation break down. Mattress stuffing ensues en masse.

The Fed is clearly thinking about it. In testimony to Congress last year, Fed chairman Janet Yellen admitted policymakers “expect to have less scope for interest-rate cuts than we have had historically,” adding she would not completely rule out the use of negative interest rates.

The BIS—the central bank of central banks—in its latest quarterly review posited that a crypto backed by the Fed “has the potential to relieve the zero lower bound constraint on monetary policy.” Any distinction between regular dollars and this new “Fedcoin” could be removed by establishing a fixed one-to-one valuation. Any competition from the likes of bitcoin could be squashed by regulation; not unlike how the private ownership of gold was outlawed in the 1930s when it threatened the Fed’s ability to ease credit conditions.

At the risk of being repetitious, pretty much all of the above looks good for gold and great for silver.

MD: Remembering what money really is … “an in-process promise to complete a trade over time and space” … that it is only created by traders … and that for any given trading promise, it only exists for the duration of that promise … and that during that interim time, there is perpetual perfect supply/demand (i.e. zero inflation) of that money created … knowing all that, look how silly such articles like this become.

MD: Note (2025): We are now referring to the MOE (Medium of Exchange) as the RMP (“Real Money Process”). It’s a better description. We’re not involved with the medium (albeit the HUL is media). Rather, it’s a “process” of keeping track of promises… and mitigating DEFAULTs with INTEREST collections, immediately on discovery. And the process maintains the operative relation: INFLATION = DEFAULT – INTEREST = zero.

by Izabella Kaminska

In 1999, the actor Whoopi Goldberg made a bold decision. Rather than be paid for an endorsement for a dotcom start-up, she took a 10 per cent stake in the business. It seemed wise. At the time, everyone was investing in internet businesses and a rush of initial public offerings was making early investors into millionaires. I was reminded of this amid a flurry of news about the new boom in cryptocurrencies — and their celebrity backers. Ms Goldberg’s venture, Flooz, was billed as the future of money in a digital world and it hoped one day to rival the dollar.

MD: Let’s see if there is evidence that they had any clue about what money is before starting this venture. Nope!

The way it worked, however, was much less revolutionary. The service resembled a gift certificate: customers paid in dollars and received Flooz balances. These could be redeemed at participating merchants, with the hope that credits would one day circulate as money in their own right.

MD: What’s the point? How were they supposed to work without dollars kicking them off in the first place? When they replaced the dollar, what was going to create them?

The problem for Flooz was that little prevented mass replication of its model. One prominent competitor, Beenz, differed only slightly, by allowing its units to trade at fluctuating market prices.

MD: A “proper” MOE process can have no competitors. A competitor either does the exact same thing as this proper MOE process, or it isn’t competitive. And since there is no money to be made in the process (contrasted to the similar casualty insurance process where money is made on investment income), it’s not going to attract many competitors. It would be the trading commons themselves who would steward the process. We have experience with this. The internet is just such a process example … a technology commons.

Like banking syndicates before them, the ventures decided to club together for mutual benefit by accepting each other’s currencies in their networks. Even so, by 2001 both companies had failed, brought down by a lack of the one ingredient that counts most in finance: trust. Flooz was knocked by security concerns after it transpired that a Russian crime syndicate had taken advantage of its currency, while the fluctuating value of Beenz soon put users off.

MD: “Fluctuating value turning users off” is a good sign. Users aren’t as clueless as these entrepreneurs.

Their loss turned into PayPal’s gain, the latter succeeding precisely because it had set its aspirations much lower. Rather than replace established currencies, PayPal focused on improving the dollar’s online mobility, notably by creating a secure network that gained public support. This, it turned out, is what people really wanted.

MD: And PayPal missed the real opportunity by not following up. If they had gone ahead and implemented micro-transactions, I would be paying a tiny price (maybe 1 cent; 5 cents?) for reading this article. That day has to come. Supporting the likes of FT with advertising and subscriptions is just plain nonsense.

Did we learn anything from the failures of the internet boom? Apparently not. In what is looking increasingly like a new incarnation of dotcom fever, celebrities are endorsing virtual currency systems. Heiress and reality TV star Paris Hilton tweeted this week that she would be backing fundraising for LydianCoin, a digital token still at concept stage. It offers redemption against online artificial intelligence-assisted advertising campaigns.

MD: Advertising campaigns “are” artificial intelligence. We know it as propaganda. It’s annoying … and really dangerous when it reaches the minds of the stupid.

Baroness Michelle Mone, a businesswoman, announced she would be accepting bitcoin in exchange for luxury Dubai flats. What is particularly striking about this path to riches is its “growing money on trees” character.

MD: What is “particularly striking” is that someone would part with their bitcoins for one of her flats … knowing the extraordinary deflationary nature of bitcoins.

While the internet boom was dominated by IPOs, linked to a potentially profitable venture to come, this time it is “initial coin offerings” igniting investor fervour. Most ICOs do not aspire to deliver profits or returns. Indeed, from a regulatory standpoint, they cannot — most lawyers agree doing so could classify them as securities, drawing regulatory intervention which would force them into stringent listing processes.

MD: If they knew what real money was, they would know that every trader (like you and me contracting for a house or car with monthly payments) is making an ICO. What in the world is it going to take to get these brilliant idiots to recognize and understand the obvious?

That opinion was substantiated in July when the US Securities and Exchange Commission warned: “Virtual coins or tokens may be securities and subject to the federal securities laws” and that “it is relatively easy for anyone to use blockchain technology to create an ICO that looks impressive, even though it might actually be a scam.”

MD: Now isn’t that the pot calling the kettle black. The SEC is itself a scam.

So most ICOs make do by selling tokens for pre-existing virtual currencies for promises of direct redemption against online goods, services or concepts, or simply in the hope the tokens themselves will rocket in value despite offering nothing specific in return.

MD: Stupid is as stupid does. If you know that zero inflation is the right number for any money you don’t go looking for “rocketing” value. An ideal unit for money is the HUL (Hour of Unskilled Labor). We were all a HUL doing summer jobs in high-school so we can relate to them any time in our lives … and to any trade we make. The HUL itself has not changed over all time. It trades for the same size hole in the ground. With median income now at about $50,000 per year, the median person is able to trade his skilled hours for about 3.5 HULs these days. If we have been using a “Real Money Process” (RMP) all these years, the median person would be a 3.5x’er. The 3.5x factor is the real measure of value (i.e. what someone is able to trade their hours for).

They still think they can succeed where other parallel currency systems have failed, by bolting into pre- established blockchain-distributed currency systems such as Ethereum or bitcoin.

MD: A proper MOE process is totally transparent when it comes to the money creation/destruction parts of the process. Block-chain techniques (i.e. universally accessible ledger) would be helpful to enhance that transparency. But there would be no mining involved. New blocks would have to be created at any time at zero cost.

These already come with a network of token-owning users. But with the numbers of conventional merchants that will accept these currencies falling rather than rising, these holders need something more compelling to spend their digital wealth on. As it stands, the real economy can only be accessed by cashing out digital currency for conventional money at cryptocurrency exchanges. This comes at some expense.

MD: So far, the expense is insignificant … because of the enormous “guaranteed” continual deflation of the cryptocurrency itself (their ridiculous mining process). It’s kind of like the reverse of our government run lotteries. With government lotteries, you are guaranteed to lose (except for the minuscule chance you win). With cryptocurrency, you are guaranteed to win (until everyone loses as what is essentially a Ponzi scheme … with no Ponzi … it all comes down).

But with regulators clamping down on how exchanges are governed, token holders who cannot or do not want to pass through know-your-customer and anti-money laundering procedures remain frozen out.

MD: What’s disconcerting is the knowledge that if we instituted a “proper” MOE process, the regulators would clamp down on it too. It would make their current counterfeiting impossible … and it would make it impossible for money changers to demand tribute. That would just not stand. Regulators and governments everywhere are a major part of our problem.

That leaves their holdings good for only three things: virtual currency speculation, which is ultimately a zero-sum game; redemption against dark-market goods or capital control circumvention. It is assumed ICOs offering real goods, services or real estate in exchange for cryptocurrencies can somehow tap into this sizeable, albeit potentially illicit and restricted, wealth pool.

MD: Real estate wants positive inflation. Money changers in real estate do not want real money (there’s no leverage in it … time value of real money is guaranteed to be perpetually 1.0000) … and for sure they don’t want money that is guaranteed deflationary.

Yet if competing unregulated economies really start gaining traction, governments will act. China’s central bank has already branded ICOs an illegal form of crowdfunding and more rulings are expected from other jurisdictions in coming weeks.

Then again, if history teaches us anything, the system’s own propensity to cultivate fraud and unnecessary complexity in the face of more secure and regulated competition may be the more likely thing to bring it down.

MD: Actually, if you crowd (i.e. encroach on) the money changers existing con … “they” are likely to bring it down. “Real” money crowds money changers out of existence. That will not stand. Too bad for us traders and producers in society.

When given the choice, people usually opt for security.

MD: Which of course we don’t have … if you call government taking 3/4ths of everything we make …. you can’t call that security. I call it slavery. If you call money changers taking “all” taxes we pay as tribute … leaving governments (which the money changers instituted to protect their con) to sustain themselves by counterfeiting … I call that criminal.

izabella.kaminska@ft.com Copyright The Financial Times Limited 2017. All rights reserved. You may share using our article tools. Please don’t copy articles from FT.com and redistribute by email or post to the web.

MD: I am openly violating this request. My comments are far more valuable than anything to be learned in this article. And the fairest way to make my comments is to intersperse them in the disinformation that these articles present.

MD: Money Delusions has no illusion for what money is (see right sidebar). Bitcoin, like gold, is a clumsy stand-in for “real” money.

Well, it looks like they’re taking it a step further. On the one hand, they’re trying to give it stability while on the other hand they’re trying to give it leverage. In both cases, Bitcoin’s foundations are firmly planted in quicksand.

And the allure of Bitcoin? “It doesn’t require trust … there is no entity to be trusted”.

Well, a good way to study issues is to inspect the limits. On one limit, we have no Bitcoins. At that limit, confusion about money remains unchanged. At the other limit, everything is the Bitcoins … and just looking at the algorithm this limits the number … thus infinite value is at the upper limit. Traders (like you and me) can’t trade in that environment. When we promise to trade 360 monthly payments of money for a house today, we want that money to be worth exactly the same every one of those months. “Real” money behaves this way. Bitcoin money does not. Every month, the Bitcoin we must return is harder for us to earn.

Fisco, a Japanese financial information company, announced this week a unit of the company has issued a bitcoin bond.

MD: Where are the Bitcoins going to come from when these bonds mature? Where are the Bitcoins going to come from that pay the coupon? Bitcoin is hopelessly deflationary. Thus, buying a Bitcoin bond puts huge pressure on the seller to deliver higher valued Bitcoins when the bond matures. How are they going to do that? And with the value (through scarcity) of Bitcoin continuously increasing, the bond will continuously increase too. Why in the world would Fisco create such a thing? What’s in it for them?

The bitcoin bond “brings digital currencies into the world of high finance,” said Dan Doney, chief executive officer of Securrency.

MD: High finance is nothing but highly leveraged gambling. It only works with inflation. It strangles itself with something deflationary like Bitcoin. High leverage is instant death for these gamblers facing deflation … and with Bitcoin, that deflation is guaranteed in exponentially increasing fashion … until it just collapses totally out of self strangulation.

The development of bitcoin options, futures and now bonds could help the often volatile digital currency become a better-established asset class.

MD: “Real” money is not volatile. It is in perpetually perfect supply/demand balance. It is in perpetual free supply. Thus, there is no need for options, futures, or bonds of any kind. How could it be more obvious that Bitcoin is a terminally stupid idea?

Bitcoin is getting closer to looking like a traditional financial product.

MD: Oh really? Can you buy a ribeye steak at the super market with one?

Japanese financial information firm Fisco announced Monday it is experimenting with the country’s first bitcoin-backed bond. The news follows other announcements in the last several weeks for bitcoin options, futures and an exchange-traded fund tracking bitcoin derivatives in the U.S.

“I think it’s a very healthy and natural progression of the space,” said Adam White, Coinbase vice president and general manager of its GDAX exchange, told CNBC in a phone interview.

MD: Adam White. Might as well be Joe Jones in searching for what becomes of that idiot and his predictions.

Derivatives products will allow for greater liquidity, better price discovery and lower volatility, White said. “I think products like derivatives or an ETF effectively allow traders to do two things: speculate and hedge risk on the price speculation.”

MD: Why does Bitcoin need greater liquidity? A “real” money process has perfect liquidity. There is no restriction on its supply and it maintains perpetual perfect supply/demand balance … zero inflation. It requires no price discovery. It’s value is permanently in units of HULs which never change. You don’t need derivatives for it because leveraging zero does nothing. You don’t need ETFs for it because there are no exchanges. All money exchanges on a 1 for 1 basis after “real” money drives out all less efficient money.

Bitcoin price 12-month performance

Source: CoinDesk

MD: Now look at that! A “Real” money price performance curve is a straight horizontal line … for all time. Why would any trader want to make a promise spanning time and space with a time dependent curve like that? He wouldn’t!

Bitcoin has more than quadrupled in price this year, hitting a record above $4,500 Thursday and notching a market value of $74 billion amid growing institutional investor interest in the digital currency.

MD: Over the same period, any “real” money would have remained at exactly the same price. Traders? What would you rather have? Your trading promise spanning time and space linked to … an unpredictable accelerating object or to a perfectly static object?

Many governments and financial institutions see enormous potential for improving transaction security and efficiency using the blockchain technology that supports bitcoin.

MD: But does that blockchain technology dictate the scarcity Bitcoin exhibits (and cherishes)? If not, blockchain technology would be enormously helpful to “real” money too. Real money requires complete transparency of the money “creation” process and blockchain (if in free supply) would facilitate that.

But the surge in investor demand has also revealed access issues with third-party storage systems and trading platforms that fall short of the more established Wall Street markets.

MD: What is being stored is just information (ledger entries) … and it’s essentially replicated so can’t be destroyed. The blockchain, being universally distributed, implies no storage at all? It would be an increasingly rare case where “real” money using a blockchain would have to be in coin or currency form which could be physically destroyed.

Bitcoin’s price is also prone to massive swings of several hundred dollars within a day. With bitcoin futures in the works, investors will be able to protect themselves from potential sharp drops in prices through hedging.

MD: Why? “Real” money is certainly not so prone! Why are people using and advocating Bitcoin being so skittish? Remember, it requires “no trust”!

The ability to hedge bitcoin investments paves the way for other products, such as bonds.

MD: Insurance is useless when the insurer is guaranteed to fail.

Fisco’s three-year bitcoin bond was issued by its digital currency exchange unit for an internal trial on Aug. 10, according to a Google translate of the press release.

The bond has a three percent annual interest rate and returns bitcoins when it matures, the release said. The total worth of the bond was 200 bitcoin, or $900,000 at Thursday’s prices.

MD: 3% paid in Bitcoins? Where are those coming from? And they’re only paid at maturity? Thus, a buyer would have to wait three years before realizing he was scammed? With an annually paid coupon, he would know the bond writer was room temperature in one year.

The bitcoin bond “brings digital currencies into the world of high finance,” said Dan Doney, chief executive officer of Securrency, which plans to launch a platform at the end of the year to allow investors to buy stocks using bitcoin. Doney was chief innovation officer at the U.S. Defense Intelligence Agency before co-founding Securrency in 2015.

MD: World of high chicanery!

The biggest challenge is “it is very difficult to predict the price of bitcoin tomorrow, let alone a year from now,” Doney said.

MD: … just as is gold. And just like gold, you can be sure it will go up over time. It has to. It is deflationary by design. Next thing they will invent is a dollar / bitcoin cocktail trying to match the dollars inflation with the bitcoins deflation. If they are able to do that perfectly, they arrive at “real” money. Why not just institute “real” money to start with. It is guaranteed to stay real … perpetually in real time.

A bitcoin-backed bond would allow large institutions to store value using the digital currency and potentially be more open to accepting bitcoin as payment, analysts said.

MD: Ah … so they think it’s a storage problem? Why? Because the dollar is inflationary? Or because it might catch fire and turn to ash? Why would large institutions store value as something that is guaranteed to blow up (or more accurately, blow-down) by design?

“It is interesting financial firms are trying to get their arms around the currency and what it can be,” said Brian Patrick Eha, author of “How Money got Free: Bitcoin and the Fight for the Future of Finance.”

MD: If I could get that guy to comment, I would welcome an opportunity to annotate his book. Otherwise, by the title, reading it would be a waste of time.

MD: If you can create a fiction like the VIX and trade it, you can create any fiction and trade it. What’s not to love about that? It’s going to become a pretty cluttered landscape isn’t it? Compare that to “real” money. Regardless of how many purveyors there are, they will all trade 1 for 1 for each other. It’s the nature of the process.

MD: You can make a market in cow dung and clear it. What’s the big deal?

Historically cryptocurrencies “were very much a domain for crypto anarchists and tech-savvy people, and that has changed in the last couple years,” said Niklas Nikolajsen, CEO of Swiss-based digital currency broker Bitcoin Suisse. “This means a whole new ballgame of people are going to get access to the market.”

MD: Right. Like religion changed after they first printed the bible. It just enabled more corruptions and variations of something that was a hoax to start with … something of the sole domain of the monks on high… (and the soul domain of the stupid) .

WATCH: Trader explains when to buy bitcoin

Here’s when you should buy Bitcoin, according to one trader

MD: Buy until it becomes a trading black hole by self strangulation. Don’t even worry about the buy low/sell high wisdom. It will essentially always be buy high/sell higher. Just before the limit, your return is infinity squared. At the limit, it strangles itself.

Host of The Bitcoin Podcast and BlockChannel, Blockchain Analyst at Novetta, Bitcoin Junkie, and former academic in high-performance computational chemistry.

NOTE UP FRONT: I express my opinions here (at least at the end of the article). If you don’t like them and don’t have evidence to support your dislike, then go kick rocks.

MD: I definitely have evidence … and proof, so I don’t expect to be kicking rocks (or pounding sand). But I predict I’ll ultimately end up doing just that. Cognitive dissonance is the strongest force I’ve seen in human nature. It has sustained all religions and enabled new ones.

ICO (Initial Coin Offering) is a not problem when you have a “proper” MOE process. Only traders create money. They do it by making a trading promise spanning time and space and get it certified by the process.

It initially is just a record entry with the “score keeper” doing the certification. It usually quickly gets converted to a record entry in some other trader’s ledger or as currency or coin. In the case of the latter two, there are two instances of each: (1) physical media in circulation; (2) physical media in storage.

In both cases they ideally have HULs (Hours of Unskilled Labor) as their units of measure. These are universally known to never change trading value over time and space … you always get the same size hole in the ground when you trade one HUL for a hole in the ground.

In case (1) the HULs (money) serve in small simple barter exchange transactions … like buying a candy bar. In case (2) they are totally valueless … as long as they don’t enter circulation. They can be destroyed with no impact on trade what-so-ever. That is not true of those in case (1).

In any case, for this trading promise, no money exists before the promise, nor after final delivery (or mitigation of default by interest collection of like amount). And all money is just such a promise. From this emanates the guarantee of perpetual zero inflation. Start with 0; end with zero; 0 minus 0 is zero.

Things are moving forward quite rapidly in this space; I simply don’t have time to look at all the ICOs (ya know, full time job, podcast, wife, and stuff), but this one struck me as different while also being wildly anticipated.

MD: Multiple “proper” MOE processes can co-exist simultaneously and compete. The only front they can compete on is efficiency (and thus lowest cost and interest to traders using them in money creation).

This article digs into the Status platform ICO model, how it differentiated itself from other models, and what the results were. If you aren’t sure what they do, go read about em here.

MD: I see a case where the brilliant mind has complicated a non-problem.

You might want to start by reading their recap of the ICO. Ya know, cause they wrote it.

This was all done using Project Jupyter notebooks and the Pandas package. The transactions were retrieved using my Python bindings to the Etherscan.io API (tagging Matthew Tan). The methodology is very similar to my previous articles mentioned earlier, and the Jupyter notebooks of all of it can be found in a new Github repo.

MD: I ignored Python from the first time I saw it. You can’t use “white space” as a programming element. It’s a fundamental concept … one that if ignored will come back to bite you over and over and over again. And I have some experience. I created GLEE (see WithGLEE.com).

In particular, I retrieved all transactions from the SNT Crowdsale contract address from Etherscan.io, and parsed out the ones that had an error or had a value of 0 ETH, for both external and internal transactions. The values refunded by the internal transactions are removed from the corresponding external amounts when grouped together. This is my dataset. All conclusions and numbers are derived from that. I don’t do an errored transaction analysis on this one, one may come afterwards if no one else does it, but people like CodeTract have been doing an excellent job of this for other ICOs. Go check out their stuff.

MD: See how complicated things can become when you’re totally confused about the problem to begin with? Think concepts! What are the concepts? KISS!!!

I’m happy to see that others are doing analysis of this space, so we can see more of the trends developing.

Status.im ICO Summary:

The Status platform prides itself on really caring about their community, the Ethereum community, and learning from previous ICO models.

MD: A “proper” MOE process cares nothing about the “community”. It has the requirement that “all” traders and “all their money creating promises” and “all their deliveries on those promises” and “all their defaults and immediate mitigating interest collections of like amount” are “always” totally transparent to everyone in any community … whether they create the exchange media or just use it in trade or are just watching. Noting is secret at the money creation or the money destruction stage of a “proper” MOE process. All “use” of the money is perfectly confidential.

By learning from previous ICO models, I mean attempting to widely distribute your token to those who are interested in its utility in the midst of a fever-pitched, FOMO induced, and irrationally exuberated (made that one up!) investor community ready to flip your ICO for profit.

MD: Contrast this nonsense with a widely recognized “proper” MOE process concept. To help, consider a Mutual Casualty Insurance Company. It is owned by the members (the users … the traders). CLAIMs perpetually equal PREMIUMS. Any money made on investment income in the meantime goes to reduction of premiums and application to costs of operation. A “proper” MOE process is only contrasted by having no investment income … there is nothing to invest. Thus, costs have to be recovered by interest collections.

But just like a Mutual Casualty Insurance Company, there can be any number of them … competing against each other. For all intents and purposes, in the risk community, they are all the same. They differ in efficiency (lower premiums, better claims service).

Proper MOE processes have a notable difference here. The exchange rates between them are perpetually 1.000. There is free exchange between them. There is no such thing as exchange of one insurance policy for another … except in the case of re-insurance which is an internal, not external, practice.

What was their plan? Two-fold:

MD: I’m not going to comment further on this concept. It is a non-issue. With a “proper” MOE process, it never comes up. I’ll scan ahead to see if there is anything else I take issue with. It’s silly for me to nit pick details when the whole process is bogus and misguided in the first place.

They created a pool of “Genesis Tokens” (SGT) to give to early contributors that clearly showed they wanted to help the platform grow, which were given out at the discretion of the core devs. This token pool corresponded to a maximum of 10% of the total token supply. After the contribution period, SGT could be converted to the ICO token (SNT) so early contributors could “get in” on the ICO token for being a contributor early. Basically, early disbursement of tokens that map to a given percentage of the total.

As for the crazy investors, they implemented a soft-cap, and subsequent “Dynamic Ceilings.” What is that? Well, you should read it from the people who implemented it here like a smart person, and then frown at my shitty explanation here. My explanation of Dynamic Ceilings, just imagine that as time went on, large investments only got a portion of their investment accepted, and the rest was refunded. This was an attempt to increase the time window for smaller investors, and slowly make it more difficult for large investments to get in. The effect of this was for every transaction that got an amount kicked back, there is one regular tx and two internal txs, for example ( numbers are for illustration ):

1.) User attempts to send 100 ETH

2.) Over time, smart contract says "screw you big investor, give the little guys a chance!"

a.) Smart contract accepts 20 ETH

b.) Smart contract refunds 80 ETH

3.) User gets 20 ETH worth of SNT and 80 ETH refund

** Note that percentages changed as time went on.

Here are the stats I pulled from various sources, as well as my personal analysis of the transactions themselves.

Start Block: 3,903,900

End Block: 3,908,029

Investment Time Period: 4,129 blocks or ~17.20 hrs

So this one got a bit hairy when summing up investor amounts from the smart contracts. You’ll notice (you probably didn’t notice) that I’m off by ~559 ETH from the reported numbers by the smart contracts themselves. This is because of the dynamic ceilings they employed.

So my analysis got a few of these transactions mixed up when combining external and internal transactions, which make my numbers slightly off, sue me (don’t). This annoys the shit out of me, but I don’t have the time to fix what went wrong. The trends will be the same, which is the main point of this article.

Total Supply Distribution:

Below is the Status graphic from the previously linked Contribution article for your convenience.

Note that the Status Genesis Allocation is “up to 10%.” Well, they didn’t actually give all of their allocation out, so the real numbers are as follows:

Status Genesis Token Holders: 6.92894026 %

Public Contribution: 44.07105974 %

Status Core Dev: 20 %

Reserved for Future: 29 %

Public Contributor Investment Distribution:

The remainder of this article is discussing that ~44% piece, specifically on how much of the total supply these investors control, and their distribution. In other words, we’d like to see how well the ICO did in “spreading their seed,” if you will. Were they premature like the majority of highly popular ICOs, or did they pace themselves well despite the crazy excitement?

MD: This is not an issue with a “proper” MOE process. There are no investors. There is no control. There is just federation of the process (like franchising of a restaurant when the franchisor … think PayPal without a linkage to banks … dictates operations and standards and otherwise has no interest).

With a “proper” MOE process, “all” franchisees must exhibit perfect transparency and thus exhibit perpetual perfect balance between the supply and demand for the money they certify. This means real time monitoring for defaults with immediate mitigation by interest collections of like amount.

Each unique address was summed up, giving its total contribution, and then placed into an “investor bin” that corresponds to how big of an investor they are. These bins are broken up by orders of magnitude of ETH, i.e.:

Important Note: These value percentages are relative to the TOTAL SNT SUPPLY, which shows what type of investor has what control over the entire Status platform. Also, it should be noted that these numbers are only good for showing the distribution at the moment the ICO ended. More on this later. Here is the table of investors:

MD: I really can’t believe this much work has gone into a concept that is so easily dispelled as total nonsense. No wonder the cognitive dissonance is so strong.

and the plot:

click the pic to blow it up

click the link below to bring up an interactive version

We can see from the numbers that smaller amount investors have significantly more control of the token supply than previous ICOs that I’ve analyzed. This is a significant pullback from the trend of very few people controlling the vast majority of tokens, albeit the trend still exists.

It should also be noted that this does not take into account the extra ~7% of token holders that are early contributors to the platform.

A few responses reminded me to point out that a unique address is not indicative of an individual, and such assumptions should not be made. I have discussed this in my TokenCard article, and did not include such a discussion. I guess it is prudent to say something.

MD: This does imply an issue that a “proper” MOE process has. At the money creation point, no trader is anonymous, no trader has more than one identity, no two traders have the same identity, and all traders are individuals … partnerships, corporations and governments need not apply. Common AAA principles (Authentication, Authorization, and Accounting) are strictly adhered to throughout.

Due to the way the ICO was structured, the savvy investor was incentivized to break up his desired large contribution amount into many smaller addresses, and spamming them into the ICO to try and see what sticks. If enough of this happens, then you basically sybil (not quite sybil, but you get it) the ICO into a DoS situation, which is what we saw. I don’t have enough data to say how much of the network congestion was due to this, maybe someone else will do a sweet analysis of that.

MD: With a “proper” MOE process there are no investors … savvy or otherwise. And there are no incentives. It’s all about trade and traders (like you and me). Further, there is no “time value of money”. Inflation is guaranteed to be zero. Thus, the cherished factor (1+i)^n is 1.000 for all “n” (“i” being always zero). Gamers in finance will need to find other work

There are some indicators that this was not the entire case, which you can read about in my response to Nick Johnson below, if you’re interested. There is another simple plot in there, for the people who just want eye candy.

People are hating on Status for various reasons, which are mainly driven from garbage understanding of how the Ethereum network works, and misplacing blame.

MD: You’re going to get that when you have a totally bogus concept with brains and no experience at the helm. KISS is unknown to them.

It was clear the fervor was there. They were aware of it, and managed to raise a bunch money while still allowing “the little guys” en masse. You can’t really argue with that… look at the distribution.

MD: Ponzi had no trouble getting takers either. Heck, his scheme was doubling their money in two to three months. And none took their money out. They couldn’t afford to. It was destined to double again in two to three months.

This is a good time for me to introduce the definition of a capitalist and the proof:

Definition: A Capitalist is two years and an elite privilege.

Proof: Give a person a privilege of starting a bank with $1M. They can then create 10x that in money which they lend to traders at a 4% spread. That gives them 40% per year return. It doubles their money in less than two years. They take back their $1M and let the other $1M which they made ride forever after (or for their remaining 28 year career). 30 years later they can cash out at $24,000M … and for 28 of those years they had no skin in the game at all!

What’s not to love about capitalism … if you have the privilege!

You’re not going to have capitalism (or its alter-ego, communism) if you institute a “proper” MOE process.

So I believe that Status took steps in the right direction of both allowing smaller investors to contribute to an ICO, as well as being sure of putting tokens directly into the people that contributed early. This allowed people who actually helped build the system also take advantage of the ICO craze that is clearly going on. Full disclosure, I received SGT tokens for early contributions, which made me personally not inclined to participate in the ICO. I would predict that other SGT holders also felt this way, thus removing our would be transactions into the clusterfuck that was the contribution period.

MD: More full disclosure required. What did you give for those SGT tokens? Here again, you have issues that only exist because you’re working with a bogus concept!

The Dynamics Ceiling approach worked to keep a constant supply of incoming transactions of lower value over a longer period of time. The network congestion that people blame Status for is not their fault, unless you can blame them for building something MANY people wanted to contribute to.

MD: I’m an atheist but “OH MY GOD!!!” “Dynamics Ceiling? KISS!!!!

I talk at length about these network congestion issues raised from the ICO craze with MyEtherWallet’s Taylor one of my recent podcasts, take a listen:

MD: Why in the world would anyone listen if they know what a “proper” MOE process is … let alone if one was in actual operation? Would you listen?

Of all the transactions that tried to participate, the smart contract refunded 111,161 attempts for a total of 347,154 ETH.Status refunded back more ETH than they raised.

I’m not sure you can call that “greedy.”

MD: A “proper” MOE process only has one opportunity for greed by the franchisee (and none by the trader … and there are no investors). He can load interest collections with exorbitant costs. But then he wouldn’t be competitive with the other franchisees. No one would come to his store. With a “proper” MOE process, “all” traders enjoy zero inflation … and responsible traders (those who never default) have zero interest load … unless they go to a greedy franchisee … which of course they never would. You have to be smart to be responsible.

Holla at ya Boi!

I do this because I’m curious, and feel this type of information is lacking. We need to keep an eye on “where the money comes from” as we build this community out.

MD: You “need to come to your senses”. Grasp the concepts of a “proper” MOE process and it should be impossible for you to give this nonsense another thought … period.

As always, come listen to The Bitcoin Podcast and BlockChannel to hear me talk to people in the space about what they’re doing. Our slacks (TBP and BlockChannel) are always welcome to the community as well. I’m always present in them to talk.

MD: You think they would tolerate having their Money Delusion shattered? People this sharp are masters at their own cognitive dissonance. Look how many really smart religious leaders there are. Follow the money in all cases.

If you don’t like slack, hit me up on twitter at @corpetty or email me at petty.btc@gmail.com

Throw me some duckets of you like what I’m doing, and have some to spare. The donations definitely help me stay motivated to do these:

MD: Duckets? Amazing. English has abandoned me in one short lifetime!

R: I have been a bit busy, but finally have a little free time to respond.

Dissecting select statements and then sniping at them with what is often presumptuous and self serving rhetoric (as you did with the Bitcoin shop piece and other readers feedback is a “TACTIC”.

MD: Replying without even referencing the issue of focus is worse. That’s typically what I run into. You are correct. It is a TACTIC. I read an article through the frame of what I know. When I come across something that is in violation of what I know and can prove, even if all I see is a symptom, my TACTIC is appropriate for calling attention to it.

R: Apparently you believe that this type of “dialogue” places you in the critics seat or “instructor” role providing “instructive critique”; it does nothing of the kind, and rest assured you do not enjoy that relationship with me.

MD: “Apparently” is the operative word here. Its root is “appear” … and thus it must appear so … to you. I am in the critics seat. And I am an instructor if I can produce evidence that contradicts what I am reading and prove it. And that is true even if my profession is not “instructor”. The root of the word is “instruct” and it means “teach a subject or skill”. And that’s exactly what my comments do … in as unambiguous fashion as possible.

R: Allow me to demonstrate:

TM – Without even knowing what those theories are, I think it is foolish. You don’t fix an “improper” MOE process by resetting it. You don’t fix an “improper” MOE process by switching to another “improper’ process. And if you have a “proper” MOE process in operation it never requires “re-booting”………”

RD – How can you comment upon the efficacy of any theories if you do not read them. You speak of a “proper” MOE but you repeatedly fail to identify it. Your statement indicates that it is not necessary to learn anything about other theories as only your own are of importance.

MD: When I know what is true and can prove it, I don’t need to know what is theorized if the mention of the theory makes it obvious, it goes against what is provably true. Re. Failing to identify a “proper” MOE process: that takes me about 500 words. I have done it at least 4000 times over the 4+ years it has become obvious to me. I can’t begin every comment with those 500 words. If you want to know the “proper” MOE process, just ask (actually, you can now see it in the right panel). I am now using my MoneyDelusions site to annotate these articles. Contained in the right column is the definition of money and the proof. I do need to add the description of the process … but anyone understanding the definition and proof should be able to easily arrive at the process themselves … and quickly see the defects in other “theories”.

TM – [T] Who is “they”. With a “proper” MOE there are no gains! … period! Usually are reset means the create a new name for their money, you redeem the old money for the new money at 1,000,000 to 1 … and it all starts over again

……”

RD – Who to you think “they” are? It is the authors of the piece at the link. If you read the piece you would know this.

MD: Actually, it is not the authors of the piece … even in this instance. That’s why my method of annotating the actual article is my preferred mechanism. It was actually this article that motivated me to do it create the Money Delusions site. I had done it once before sometime back under a different umbrella … but after a while I was banished for breaking some rule … I was never told what. Money Delusions is now on my own host so I don’t have to deal with such nonsense. It’s not pretty yet … and may not ever be. But the points I make are indisputable.

TM – [T] “All” money is fiat … because all promises are fiat … they are made up by the person making the problem. And that’s not a bad thing … though fiat is “always” used as a slur…..”

RD – Of course the dollar and other currencies are Fiat money. The fact that I called the dollar Fiat currency should make it obvious to you that I am well aware all paper currency is Fiat. Bellicose statements are not required.

MD: What is obvious to me is you haven’t thought very deeply on the issue. Whether money is in the form of coin, currency, or simply ledger references is irrelevant. It “always” stands for an “in-process promise to complete a trade”. It is always … and only … created by traders getting their trading promises certified so they can span time and space. And of course, “all” promises are “fiat” … so “all” money is “fiat”.

As with you, the use of the term “fiat” is to contrast it with “sound” through a slur. “Sound” implicitly means “having intrinsic value” … and the Bitcoin nuts have to extend it … having reference to “work done”. But once money becomes sound … i.e. trades for something of intrinsic value, it ceases to be money. The trade is immediately completed. When you say gold is money, all you’re really saying is that it is an inefficient, expensive, clumsy stand-in for real money. Anyone who takes it as money must somehow exchange it in a future time and space with zero loss of value in the gold itself. And that’s impossible because the supply/demand balance for gold is far from stable. With “real” money it is “perfectly” stable … perpetually … everywhere!

You are correct: Bellicose statements are not required. They just kind of take on that tone after addressing the tone deaf for 4+ years … who, in the final analysis resort to religious arguments when they’re trapped by proof … or run away as soon as they become unhappy with the form.

R: Do you see what I mean? Your style of communication does nothing to advance the discussion let alone your own theories.

MD: My style of communication does more than your style of rebuttal. You haven’t addressed anything of substance which I have asserted. You have only addressed my form. That is “your” TACTIC. It is avoidance. Avoidance is far worse than abrasiveness.

R: I am quite busy and have little time to engage in this level of discourse, let alone time to even read the DB, and I am “done” with this communication thread.

MD: You’re not too busy to make false assertions. You are just too busy to support them and defend them. As usual … the line goes dead … not after rebuttal but after rejection. There are no gloves soft enough for engaging you people.

R: Respond if you must, and if it follows your prior “protocol”, rest assured that it will receive all of the consideration it deserves!

MD: Here’s an article from GoldMoney.com about crypto currency. They don’t get it either … and I prove them wrong. See it at:

Thiel Fellow, Harvard dropout. Working on some fun projects. Hit me up @ yu@benyu.org

Cryptocurrency 101

Ever since Nas Daily’s video came out about how I earned over $400,000 with less than $10,000 investing in Bitcoin and Ethereum, I’ve been getting hundreds of questions from people around the world about how to get started with cryptocurrency investment.

MD: I have an email conversation documenting my conversation with a mover and shaker in Bitcoin … when it was less than $10. I need to dig that out. I recognized it as misguided immediately. Would I have been an “investor” by making probably $40M by buying it back then? Knowing it was a totally bogus concept? It would have made his 40x gain look like a grain of sand. Cryptocurrency cannot be both a currency and an investment … and it is not a currency … and it is not an investment. It is a Ponzi scheme … without a Charles Ponzi. It is pyramid marketing at its finest.

First: I’m super glad there’s so much interest in cryptocurrency right now. I firmly do believe that cryptocurrency and blockchain technology has the potential to fundamentally change much of the way our world currently operates for the better. It reminds me a lot of the internet in the 90s.

MD: Ok. This is the 101 class. If we get through this class without knowing exactly what “blockchain technology” is, well … did we really expect to? Not me … but I do hold out that hope.

Second: Investment in cryptocurrency isn’t something to be taken lightly. It’s extremely risky, extremely speculative, and extremely early stage still at this point in time. Countless speculators and day traders have lost their entire fortunes trading cryptocurrency. I was no different when I first started investing in crypto. The first $5000 I put into crypto fell almost immediately to less than $500 — a net loss of over 90%.

MD: So is the government sponsored lottery. It “guarantees” you a -50% return … unless you win. Then it guarantees a -80% return.

Third: All of the following words are entirely and solely my own opinion, and do not reflect any objective truth in the world or the opinions or perspective of any other individual or entity. I write them here merely so people can know how I personally approach cryptocurrency, and what I have personally found helpful in my foray into this realm.

MD: Man. Is this a clever way of saying “don’t get me wrong … I’m straight out lying to you right now!”

I’m firmly of the opinion that one should never invest in something one doesn’t thoroughly understand, so I’m going to split this article into three parts.

The first part will speak to a broad explanation of what bitcoin and cryptocurrency at large are. The second will discuss my personal investment philosophy as it pertains to crypto. The third will show you step by step how to actually begin investing in crypto, if you so choose. Each section will be clearly delineated, so feel free to skip parts if they’re already familiar to you.

MD: So I shouldn’t have to look beyond the first part. Bet me! I guarantee you I’ll come away asking “where’s the beef?”

Part I: What is Bitcoin? Why is it useful?

Great question. If you want the full story behind the advent of bitcoin, I highly recommend the book Digital Gold. It traces the entire history of bitcoin from its inception all the way up to 2015. It’s an engrossing read, and highly informative.

MD: This is what you get when you talk to religious acolytes. If you begin to ask questions, you get reading assignments and directed to a higher authority. I personally went through this religion … until I finally got so informed they had to say “you’re just not going to get it”.

For now, let’s start with a quick history lesson about bitcoin. Bitcoin was officially unveiled to the public in a white paper published October 31st, 2008. The white paper is actually extremely readable, very short (just 8 pages), and incredibly elegantly written. If you want to understand why bitcoin is so compelling straight from the horse’s mouth, you must read this paper. It will explain everything better than I or anyone else likely ever could.

MD: Or if it was so “elegant” he could tell us the concept with making us go there. Another religious reading assignment from one who claims to be teaching us. My electrical engineering instructors didn’t give me reading assignments to how ohm’s law worked. They just wrote it down on the chalk board.

I won’t delve too much into the technical details of how bitcoin works (which are better elucidated in the white paper), but will instead focus on a broader exploration of its history and implications.

MD: You always get this from those who”can’t” delve into the technical details. They come across as condescending when in reality, they don’t get the details themselves. History and implications? Isn’t that what I get with “all” religions? Believe it or you’re going to hell?

Subpart: The Background Context of Bitcoin

Bitcoin was invented in the aftermath of the 2008 financial crisis, and the crisis was a clear motivating factor for its creation.